Poultry prices are once again on a rebound, as predicted by BR Research, one month ago. And what a rebound; national broiler chicken prices have crossed the barrier of Rs 200 per kg for the second time within six months. Yet, there is little clarity which way they may settle for the remainder of the year.

Poultry prices have historically been volatile, but what is special about 2020 is the extent to which they have varied. Poultry and poultry related products bottomed out twice this year during April and August, when broiler prices fell to an average of Rs 120 per kg across the country.

And in that, the two bottoms and peaks witnessed between Q2 and Q4 of CY20 mirror the rollercoaster ride that Covid-19 has taken. The first time prices crashed in Apr-20 heralded the beginning of first nation wide lockdown.

Except, when poultry retail prices crash, so do prices of Day Old Chicks. By mid-May (Ramzan), it became obvious that demand for poultry had not fallen as drastically as had been anticipated. Thus, came the first peak.

It wasn’t long before that the bonhomie of poultry growers was over. Come July, Pakistan's Covid-19 cases peaked. This time, the anticipated bottom coincided with peak red meat season (read Eid ul Azha), which is also traditionally the time of the year when poultry demand ebbs.

Since then, the unexplained decline in Covid-19 cases in the country, stepwise easing of lockdown and pickup in commercial activity, followed by eventual lifting of lockdown meant poultry demand had no where to point except upwards. And if weekly SPI prices since October are any guide, they have.

But where to from here? The end to ban on social gatherings and opening of schools in September meant that poultry prices were expected to lift in tandem. And they did, but fears of second wave, and NCOC's recommendation to ban crowded gatherings as well as re-imposition of lockdown in various forms mean the future looks uncertain once again.

The biggest directly correlated indicator of future poultry prices – day old chick prices – have shown no sign abatement so far. This means that so far, poultry growers have remained unnerved by fears of second wave, and continue to invest in fresh crop of DOC.

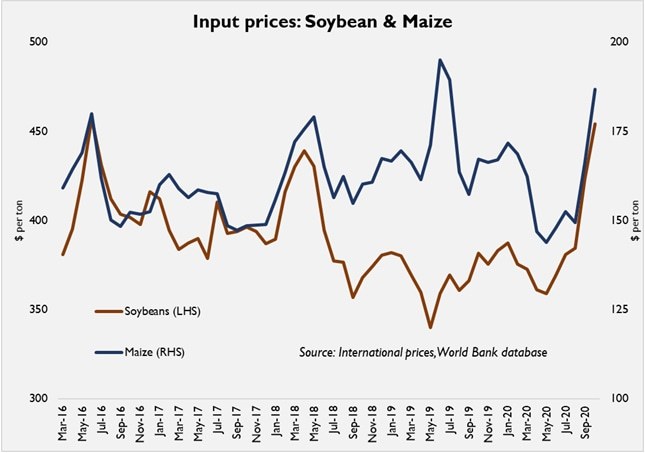

Meanwhile, other indirect indicators like prices of inputs such as maize and soybean are also on the higher side, meaning poultry prices have little reason to ease in the short term. Recall, that historically, poultry prices are on a rise during winters, as demand improves due to wedding season, and supply becomes constricted due to change in weather.

It is tough to predict which direction demand will take now. However, the price trajectory in 2020 stands out for it’s extreme volatility, created by lack of cold chain infrastructure that leaves both suppliers and consumers at a loss.

Comments

Comments are closed for this article.