Ahmad Hasan Textile Mills Limited (PSX: AHTM) was established in 1989, and was listed on the Pakistan Stock Exchange a year later. It manufactures and sells yarn and fabric. The company has its own in-house production capacity from ginning to weaving. It started its cotton ginning business by acquiring a ginning factory on lease from its associated undertaking.

Shareholding pattern

More than 50 percent of the shareholding is with the directors, CEO, their spouses and minor children of which Mr. Muhammad Haris, an executive director, holds nearly 18 percent. Another major chunk of shareholding of 40 percent is distributed with the local general public while the rest are scattered between the remainder of the categories.

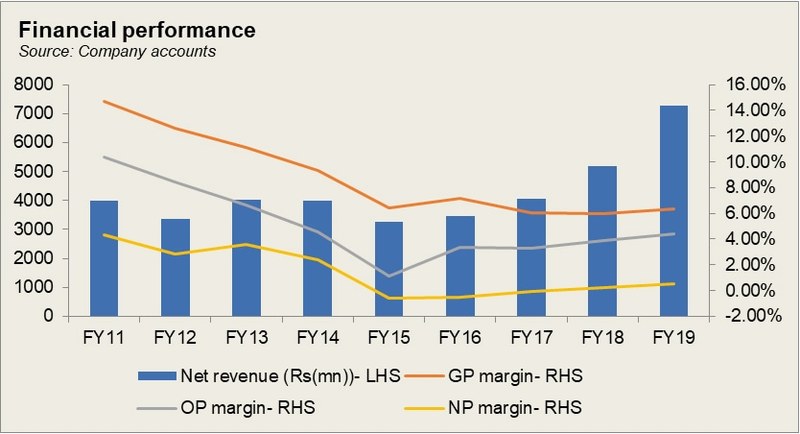

Historical operational performance

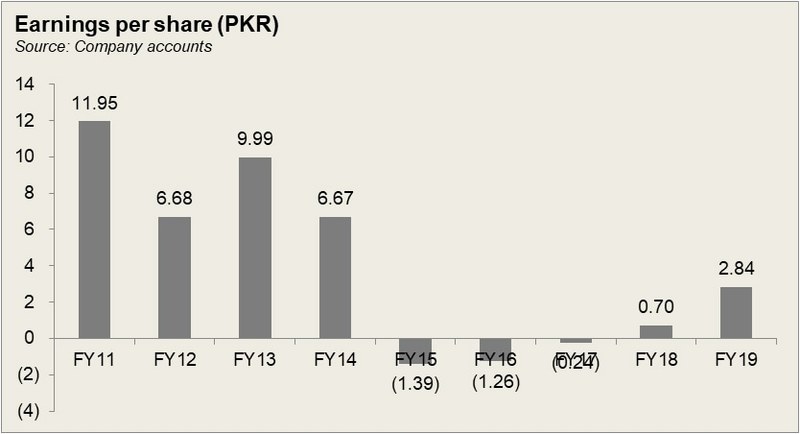

The company’s topline has, for the most part, been witnessing positive growth while profits have also largely been in the green with the exception of FY15 to FY17 when the sector experienced mediocre growth due to low demand globally.

In FY15, the company saw the highest drop in sales revenue- at 18 percent. Ahmad Hasan’s Textile Mills’ revenue is primarily sourced through export sales. Thus, with a drop in global demand for textile sector, exports saw a 20 percent decline. With a fall in revenue, the company saw the cost of production rising as a percentage of revenue, making up nearly 94 percent. This left little room for absorption of any other costs, particularly finance cost, which stood at more than 3 percent of the topline. Thus, the year concluded with a loss of Rs 20 million.

Where a lot of the companies continued to see poor sales revenue during FY16 owing to the recession that hit the sector, Ahmad Hasan Textiles managed to recover quickly; the company saw a 6 percent growth in its revenue. It seems that it was quick to shift its target market which previously was primarily exports, to the domestic market. While export sales nearly halved, local sales picked up to almost double year on year. This also allowed a marginal decline in cost of production as a share in revenue. Distribution cost also reduced due to lower expense with regards to commission paid for exports. While the company still incurred a loss, there was slight improvement in margins.

Ahmad Hasan Textile Mills saw a more than 17 percent increase in revenue in FY17. Export sales recovered to nearly double year on year. However, the increase in revenue brought with it a more than corresponding rise in costs, which made up about 94 percent of revenue. Raw material cost, which constitutes more than 70 percent of the total cost of production, saw a rise owing to costly cotton. The high price of cotton was unmatched by demand. With a consistent control on costs, and a rise in other income, that arose due to duty drawback of taxes on export sales, the company managed to lower its losses for the year to Rs 3 million.

Revenue saw its highest growth in FY18 at almost 28 percent. Both export sales as well as domestic sales saw a rise; export sales increased by a larger extent due to the effect of currency devaluation which made exports competitive. However, the higher revenue brought with it higher costs, primarily raw material. Over the years, domestic cotton production has failed to meet the market demand, due to which the shortfall has to meet through import. With the given situation of currency devaluation, imports have been costlier. However, some support to the bottomline was brought in by other income, again arising from duty drawback of taxes on export sales. Thus, the company managed to post a positive profit figure after three consecutive years of losses.

Topline in FY19 surpassed the growth of the previous year, to increase exorbitantly by more than 40 percent. Both export sales and domestic sales saw a double-digit growth; the latter nearly doubled year on year. Facing tough competition in the global market, the company found better pricing in the local market thus directing its sales here. This allowed the said growth in revenue. Cost of production persisted at 94 percent of the revenue, keeping gross margins consistent at close to 6 percent. The company steadily curtailed its costs which allowed an improvement in margins, albeit marginal. However, the rise in revenue could not be translated into a similar rise in net margins as finance cost maintained to consume near 3 percent of the revenue, thus keeping net margins below 1 percent.

Quarterly results and future outlook

Ahmad Hasan Textile Mills saw close to a 10 percent incline in topline during 9MFY20 year on year. While the breakdown of sales is not yet available, currency devaluation could serve as a rationale for better sales. Cost of production as a percentage of revenue also improved to come down to 90 percent; it had remained near 94 percent consistently in the last five years. The company’s cost controls are commendable as they managed to consistently reduce from previous years’ Rs 100 million to Rs 38 million for 9MFY20. This was reflected in the net margin which increased to near 3 percent.

While the ongoing pandemic has wreaked havoc for the economic activity the company lauds the government’s efforts to provide relief measures. The company foresees recovery in the next financial year. However, one factor that the textile players have unanimously asked for is timely payment of tax refunds, the absence of which affects their working capital needs to a great extent.

Comments

Comments are closed for this article.