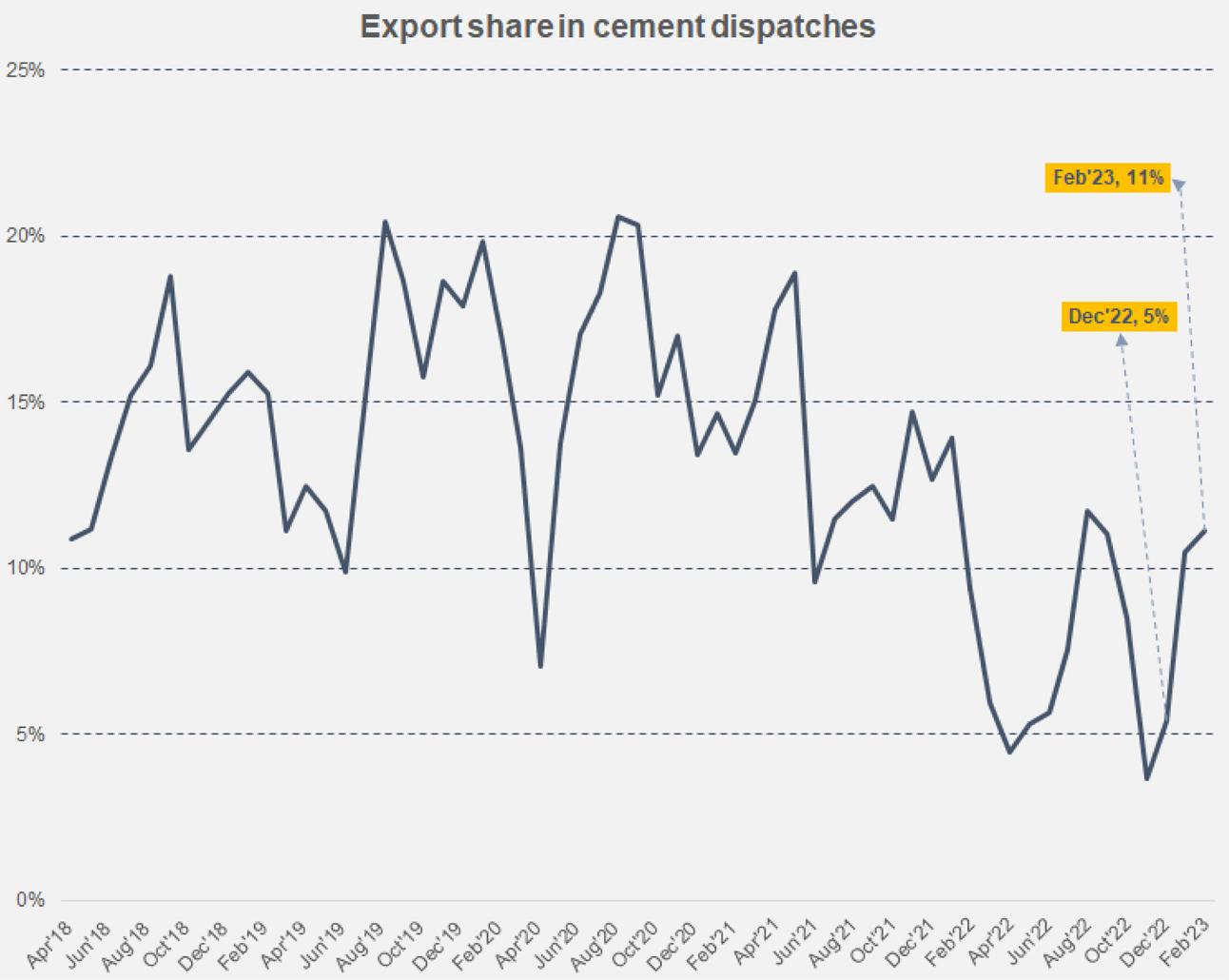

Even as the cement industry turns substantial profits, the threat of dampening demand looms large. In the second quarter of the ongoing fiscal year, high retention prices, cost effeciency in contrast to it, and effective inventory management allowed earnings to promisingly grow across the sector. This was made possible despite considerable demand slowdown, rising cost inflation (specially for other building materials) and high financing costs. But as utilization weakens, it will be ever more difficult for cement makers to sustain their healthy growth rates. In 8MFY23, total dispatches are down 17 percent, contributed by a 13 percent drop in domestic sales of cement and a dramatic 41 percent decline in exportable cement. During the period, cement exports constituted of 9 percent of total dispatches implying that cement makers are trying their best to sell as much cement as they can locally as export markets also dry up.

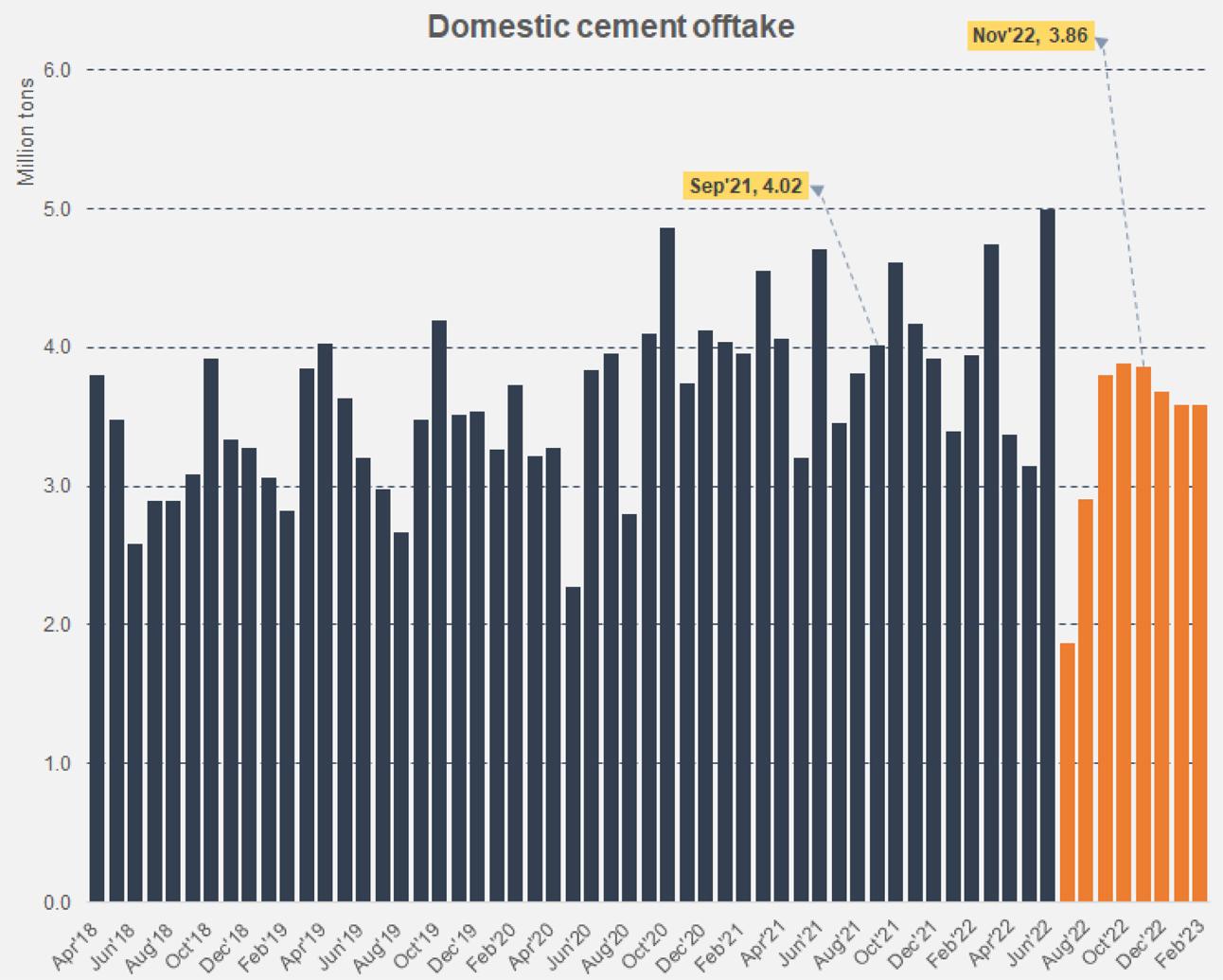

In both Jan-23 and Feb-23, cement offtake stood at roughly 4 million tons and March may register an even lower number. Construction demand is particularly weak as project costs have ballooned over the past year with most construction and building materials experiencing large and persistent price rallies. Cement prices for an instance have risen—on average across various markets—by nearly 47 percent according to data extracted from Pakistan Bureau of Statistics (PBS) for the period July to Feb. Development expenditure has also taken a backseat and only funded projects are trudging forward. In the start of the year, floods caused many projects to stall.

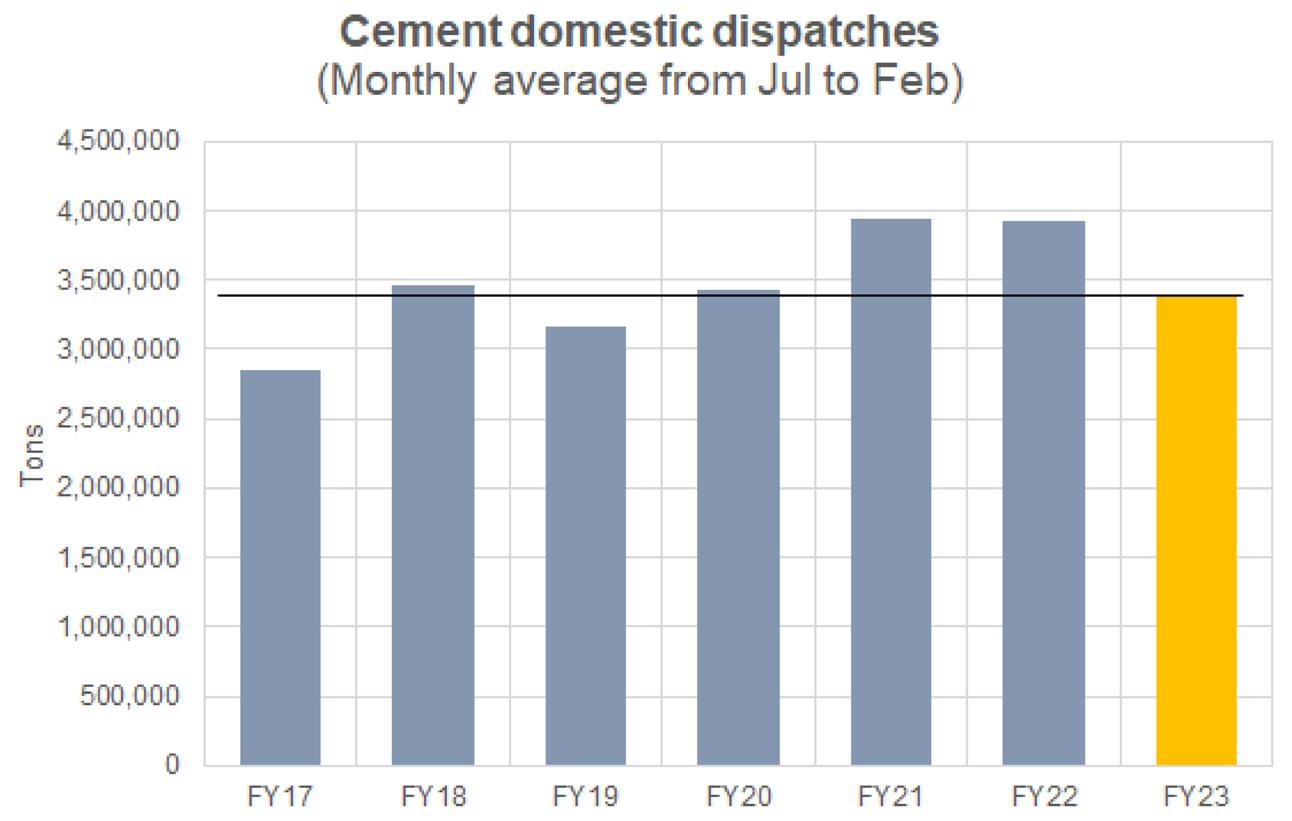

Typically, low utilization causes prices to plummet in cement markets but cement manufacturers have managed to keep prices moving upward and selling as much as they can. The estimated average monthly offtake for FY23 thus far (eight months: July-Feb) is still higher than FY17 and FY19 in the domestic markets which suggests cement demand has not dropped quite as dramatically as one would expect given inflation. But since prices have risen across the board, construction costs have not stood out like a thumb. Builders and developers have only had to absorb the cost and pass it on to end-users.

Unlike other industries that have had to shut down plants for days at end because of the unavailability of inputs—courtesy restriction on imports brought on by a critical shortage of dollars—cement has been fairly fortunate and shielded from the crisis. Cement makers have been using alternative sources of coal such as procuring from Afghanistan or sourcing it locally as opposed to importing it from abroad, long before this particularly crisis set in.At a time when other industries were chasing after the government to allow the clearance of their imported inputs necessary for continued production, cement manufacturers kept their mills running on substitute coal. As coal prices internationally drop, it would benefit them to procure coal from abroad which would help shore up their margins but these plans may not materialize until FX reserves are replenished.

One must admit that there has also been a certain level of preparedness in the industry where prudent investment in renewable energy and waste heat recovery plants have curtailed grid-based energy costs over time. Switching to local and Afghan coal when global coal prices became prohibitively high was also smart management. Demand suppression and coal prices will continue to play major roles in determining the financial performance of cement companies in the coming months. On the upside, (or downside in the case of cement buyers), prices may sustain as other building materials are also inflationary. There is no reason for cement manufacturers to normalize cement prices when steel prices are on the rise as that alone would have affected demand across the board.

Comments

Comments are closed for this article.