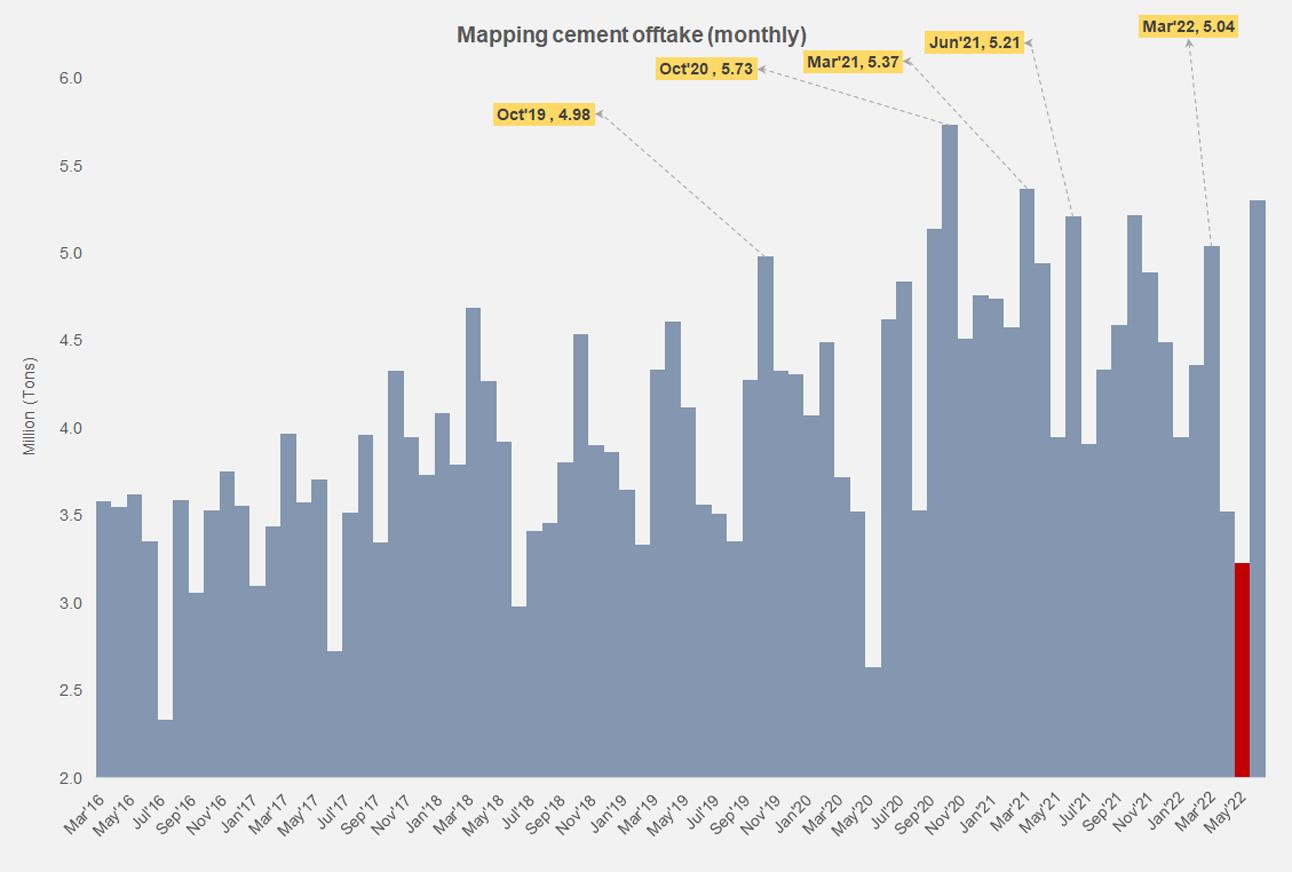

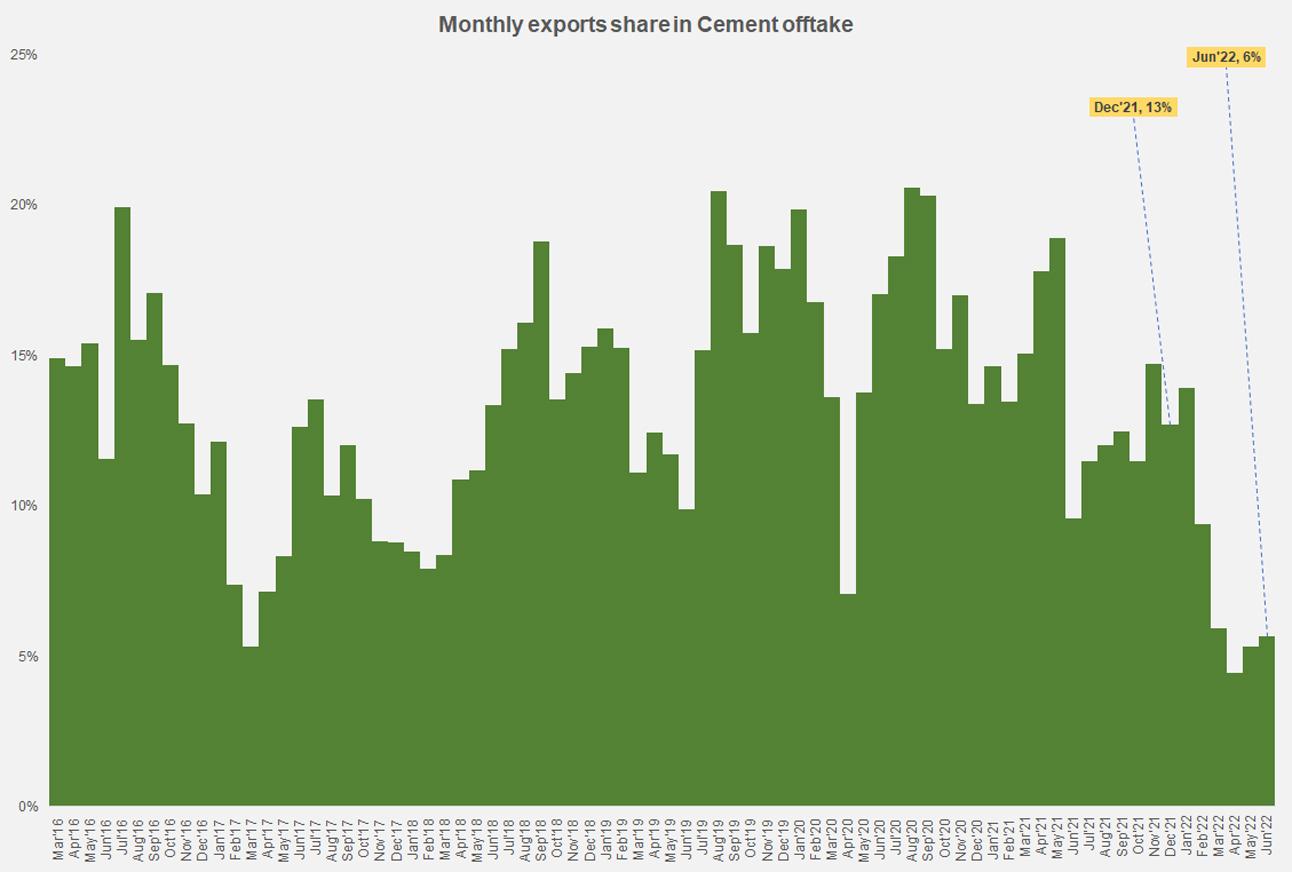

Cement offtake is substantially lower than early year expectations and recorded a negative growth in FY22 (of 8%) first time since FY11, over a decade ago. The primary culprit seems to be exports that have fallen 42 percent, coming down to 10 percent of total dispatches as opposed to 16 percent last year. Reduced demand in exporting countries, high freight rates that made exports uncompetitive all the while traditional markets such as Afghanistan and Sri Lanka drying up having undergone considerable political and economic disruptions. Domestic dispatches meanwhile did not display much excitement, growing only 1 percent in sales during the year compared to FY21.

It is clear now that a major portion of the construction demand that was to be created in Pakistan due to the construction amnesty introduced by the PTI government and housing development under Naya Pakistan Housing Program never reached real fruition. Construction demand fell victim to rising construction material inflation, especially steel, but also cement. Cement prices have risen from roughly Rs640 per bag in Jul-21 to Rs1020 per bag in Jun-22, up 59 percent. Certain markets in the north such as Lahore saw this increase to be trailing 77 percent. These are spot prices and the difference may be erratic one month to another since prices changed on a near-weekly basis over the past year but these numbers can be used to throw light on the level of inflation seen in cement. For a more comparative look, according to the monthly price index published by Pakistan Bureau of Statistics, cement price index moved up 46 percent, as compared to 33 percent for steel and 36 percent for the wholesale price index. Cement prices have evidently increased more than other goods in the basket.

Cement makers have cited their own costs ballooning as coal prices became prohibitively high in the aftermath of covid restrictions lifting, and later due to the Russia-Ukraine war that sent many commodities in a further spiral. Cement manufacturers at home—those particularly located in the north zone—were able to shift toward Afghan coal to wade out the storm that had taken over international coal markets. South plants were not able to do the same. But higher overall inflation, increased fuel costs other than coal alone, and rupee depreciation have not boded well for manufacturers when it came to costs. This necessitated a lot of price hikes that materialized that adversely impacted domestic demand. None of the impetus provided by the ousted government seems to have worked in the favour of creating additional construction demand in the country. The ongoing planned and funded projects such as hydro power projects have gone on as planned but many others’ fates—such as housing under Mera Pakistan Mera Ghar scheme—still hang in the balance. In fact, the SBP has recently restricted banks to stop doling out financing under that scheme bidding premature farewell (temporarily so or otherwise) to the 5-million-home pipe dream.

The cement industry is not going to be coasting anytime soon and the upcoming year will be a struggle in the terms of getting the desired volumes for the kind of earnings cement makers are used to. Amid inflationary pressures and PSDP cuts, cement demand will remain sluggish while there are few hopes of most exporting markets reviving or becoming more viable.

Comments

Comments are closed for this article.