The monetary policy meeting is scheduled for Tuesday. A mere look at the yield curve implies that the policy rate should be 11 percent, 225 bps higher than prevailing rate. But that does not necessarily mean that SBP will meet the market expectations. Markets always overreact – both in bullish and bearish seasons. Market participants currently seem to be showing greed. SBP needs to anchor the direction. It has limited options. One is to inject liquidity in the market and other is to be clearer and firm in the forward guidance. And the increase should be measured.

Arguably the best play SBP has is to outrightly purchase Rs100-200 billion of government papers and bonds held by the market. The section 18 of the SBP Act, which deals with open market operations (OMOs), states that “the Bank (SBP) may operate in the financial markets buying and selling outright (spot or forward) or under repurchase agreement of Government securities purchased in the secondary market or such other means as may be deemed expedient.”

There is case of permanent liquidity shortage. SBP is consistently (since May21) injecting around Rs2 trillion liquidity on seven day rolling basis thorough reverse OMOs. The secondary market purchases do not constitute government borrowing from SBP but are reported as part of monetary assets (which also includes reverse REPO purchases). MPC should bring this into the meeting agenda on Tuesday. This might give market the right signal.

This is a unique situation. Unlike previous crises, government cannot borrow from the central bank. Market is manipulating this constraint. Its motive is to maximize profits for shareholders. Treasurer’s job is to take advantage, and they seem to be fulfilling their roles well.

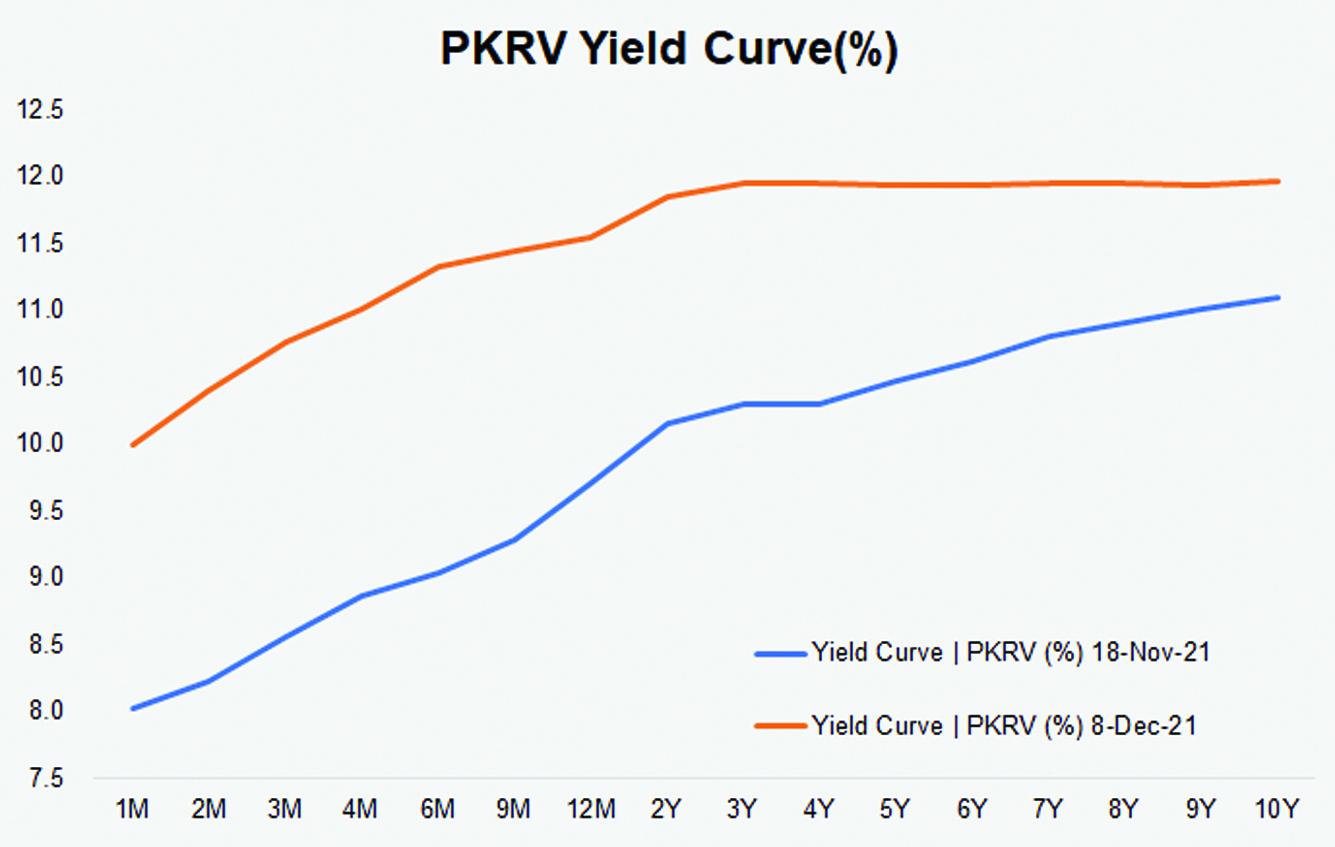

After policy rate increase by 150 bps to 8.75 percent on 19th Nov, in the very next T-Bill auction (on 1st December), the 6M paper moved up to 11.5 percent – up by 3 percent from the previous cutoff. The 3M paper is 200 bps over the policy rate. Market is sensing blood. Rs2.6 trillion worth of T-Bills are maturing in December. These are to be rerolled. If one goes with the Finance Minister’s televised wish of halting OMOs (as a threat to banks to lower T-bill rates), the government may not be able to find buyers and rates may shoot further up.

That is why right signaling by SBP in MPS is imperative. Prior to the last policy, market rates were 100 bps above the policy rate. SBP hawks increased it by 150 bps; but couldn’t beat market aggression. Its uncertainty on the forecast and current numbers in red that is causing jitters.

SBP should revise up and give a fresh range of inflation forecast. Market is expecting double-digit inflation in the next twelve months. Some are even talking about 13 percent. They are foreseeing déjà vu of 2019. If SBP thinks that market is overplaying the fear, it should be explicit about its forecast and have a decision based on fresh forecast. A measured and prudent call might be to raise policy rate by 75-100 bps.

Comments

Comments are closed.