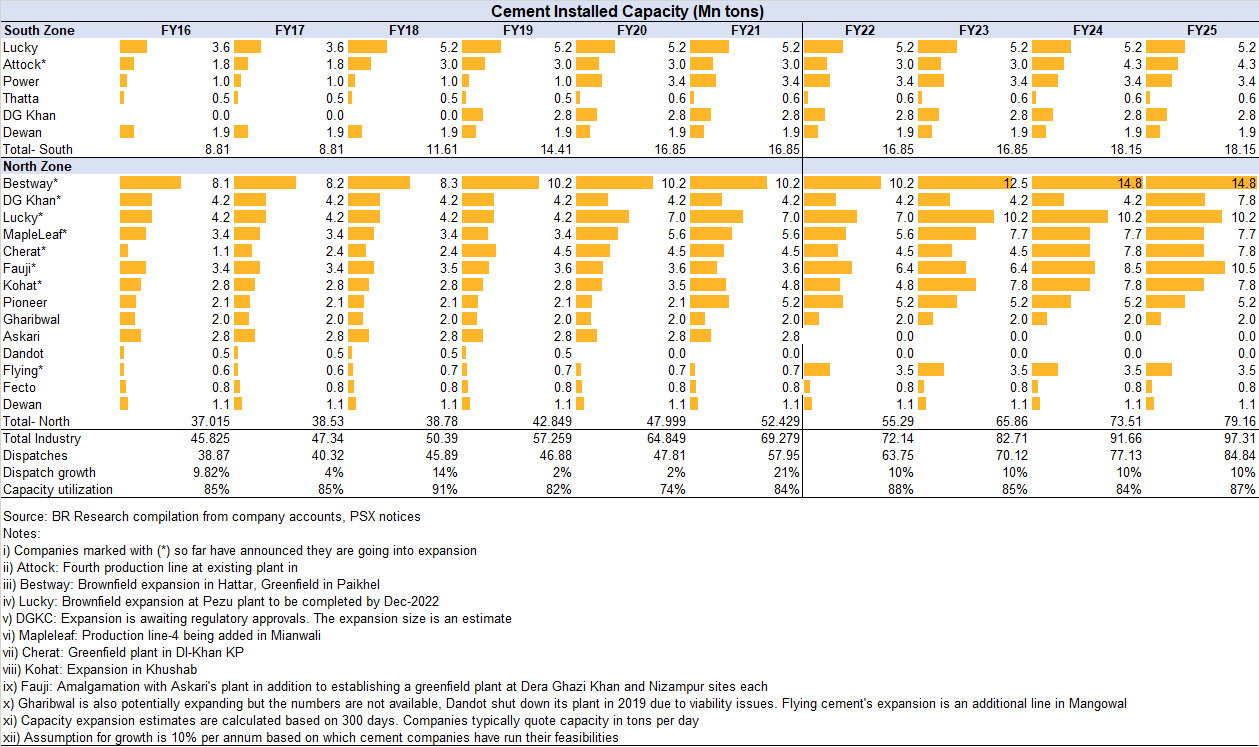

There is no denying it: the cement industry in Pakistan operates like a well-oiled machine. Some might say, even too well-oiled (reference to the assertion that the industry operates in a cartel-like environment). Prices are raised in unison; expansions happen in cycles and almost always together and industry’s financial performance as a whole follows a suspiciously similar pattern, safe perhaps for some troubled players like Dewan, or the now defaulted Dandot that stick out like thumbs. When demand is high and capacity utilization is maximizing, the industry decides to enter into expansion. This operational efficiency within the industry is very evidently a barrier to entry, not just for new players but for imported cement as well.

Last year, PM Imran Khan in the midst of a brewing pandemic announced a massive relief package for the construction industry, along with the promise of building 5 million new homes in the country during his tenure. This promise came with incentives such as mark-up subsidies, tax waivers for builders and other similar incentives to kickstart construction. Cue the next expansion cycle. By FY25, the industry would have raised capacity from its current ~70 million tons to nearly 100 million tons hoping demand to grow at a steady rate, no hitches. The ideal scenario is if both domestic and export demand grow cumulatively at an annualized rate of 10 percent. That’s not entirely unrealistic—since FY16 till FY21, the average 6-year growth stood at 9 percent, though that might be slightly misleading because FY21 was a phenomenal year for cement, raking a growth rate of 21 percent year on year. Of the total dispatches, 16 percent were exported that included a large amount of clinker. Barring that year, the average growth was around 6 percent.

For context, the industry’s CAGR has historically also trailed 6 percent with annualized growth rate around 8 percent. With CPEC on track, hydro power projects under construction, housing potentially taking off like never before (though, it is virtually impossible to ascertain the housing demand and potential offtake under the Naya Pakistan Housing Plan given there is a severe dearth of data on the subject from any government sources, including the FBR and a lot of the projects that have been registered—nearly half—are those that were already under construction); a 10 percent growth is not entirely outside the realm of possibility.

Naturally, a major threat is that domestic demand will not land at or close to 10 percent and given how dramatically macroeconomic conditions can change in this country, that could happen. For reference, in 4M so far, total dispatches declined 6 percent with domestic cement offtake growing by a lazy 1 percent and exports falling 40 percent (read: “Cement prepping!”, Nov 9, 2021). The other threat of course is export markets. Right now, with Afghanistan in political turmoil, India not open to Pakistani cement and freight costs skyrocketing making cement exports unviable anywhere abroad; the exporting outlook is not great. Already in 4M, exports as a share of total dispatches have dropped to 12 percent (4MFY21: 18%). This will continue to slide south. However, the global supply chain issues seem temporary and may normalize by the end of the year which in turn would stabilize freight and container costs (as well as commodity shortages in the global markets). In a longer-term scenario, even if FY22 cannot deliver a 10 percent growth, the next year might. Or the year next.

The industry however is definitely hinging all its hopes and dreams on domestic markets. After all, this is where pricing power exists. In an optimistic scenario where annual growth is 10 percent, the industry can actually stay at a health capacity utilization of roughly 85 percent. But even if demand drops to 5-6 percent, the industry will remain comfortable at 80 percent, and so on. The point is, while trouble may be brewing in FY22 (read: “Cement: Trouble brewing”, Oct 6, 2021), the industry is in it for the long haul with massive capacity and technology expansion plans with most cement manufacturers trying to bring more energy self-sufficiency and efficiency at their factories.

What’s actually intriguing however, is the new pecking order within the industry. There is certainly a shake-up that’s happening with some players about to become a lot more integral to the industry than they were before. Watch this space for more.

Comments

Comments are closed.