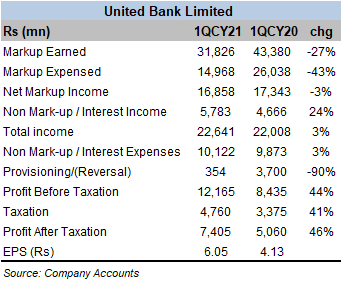

2021 has started on a smooth note for banks. UBL was the latest to rake up good profit numbers for 1QCY21 – registering a massive 46 percent year-on-year increase in after-tax profits. The earning asset base averaged 10 percent higher year-on-year at Rs1.7 trillion. The net markup income slid only marginally, as the decline in net interest margins was largely in proportion with the reduction in cost of deposits.

On the advances front, domestic loan book contracted to Rs438 billion, down by 9 percent over 1QCY20. UBL puts it down to restricted credit demand due to Covid. Earning investment portfolio continued to form the major chunk of the asset base, expanding by 26 percent over 1QCY20, averaging Rs1.2 trillion for 1QCY21.

Bulk of the investment portfolio goes to government securities, with PIBs and treasury bills lining up. The securities portfolio also continues to offer decent and reliable return, having yielded a very healthy yield of 8 percent during the period. Risk-free sovereign returns at 8 percent in times of low interest rates is all banks could ask for. No wonder that the markup on advances only makes up for 29 percent of the total markup earned.

The ADR down in the early 30s is at a multiyear low, whereas the investment to deposit ratio exceeded 80 percent. On the liabilities front, the year-on-year growth remained strong, with domestic deposits rising by 19 percent, averaging Rs1.4 trillion. The focus on low-cost deposits yielded the desired results, with CASA ratio further improving to 85.6 percent.

Current deposits growth at 25 percent, along with reduction in the policy rate ensured significant reduction in average cost of deposits – which went down from 6.4 percent in the same period last year to 3.4 percent in 1QCY21.

Non-core income was once again a major supporting act, where the biggest difference was made by capital gains realized on the sale of UBL’s international foreign bonds. Double-digit growth was also recorded in bancassurance and remittance business lines. Operating expenses were kept largely in check, keeping the cost to income ratio in line with last year.

The largest difference was made by the sharp reduction in provisioning charges – which went down by nearly ten times year-on-year. Recall that UBL - in line with its de risking strategy of international loan portfolio - had opted to book aggressively last year.

Economy seems to be gradually picking up, and there is more certainty this time around the interest rates as well. Whether or not this translated into higher incidence of private sector borrowing will be interesting to see. It is not as if UBL and others are not doing pretty well without having to lend, anyways.

Comments

Comments are closed for this article.