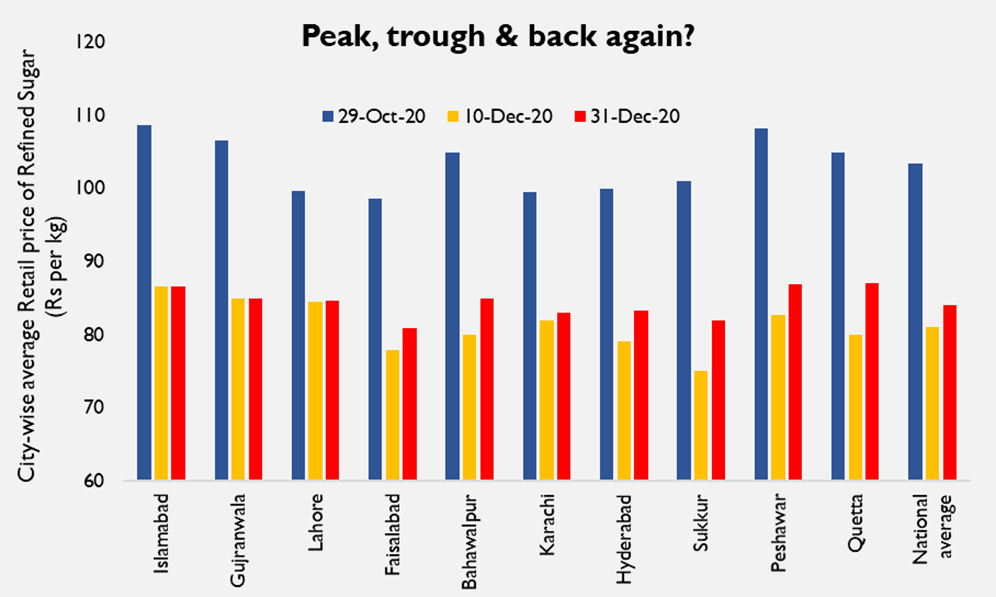

For the past four weeks – beginning mid-December – retail sugar prices are on the rise again, inching forward slowly by 3.6 percent on nationwide basis. According to news reports, commodity price in domestic wholesale markets of Lahore and Karachi has risen to Rs 87 – 88 per kg, after witnessing a short-lived bottom of Rs 71 per kg. Is another price spiral in the works?

To regular readers, this may sound like a déjà vu from 12 months ago, when sugar prices declined precipitously at the beginning of crushing season, then suddenly shifted gears around turn of the calendar year. But unlike last season, no (unofficial) strike of sugar mills has been declared so far, nor have there been reports of shortage of raw material, sugarcane.

So, what is going on? Recall that the country is slated to witness a bumper crop this season, highest since at least 2017-18. The last time sugarcane production had crossed 75 million tons, sugar production had touched 6.5 – 7 million tons for two consecutive seasons, resulting in a healthy exportable surplus of 20 percent that led to calls for freight support subsidy by the industry.

But surplus crop need not mean that the commodity price reverts to its pre-crisis (depressed) levels of below Rs 55per kg. In the 24 months since, cost of raw material has increased by 12 percent, whereas cost of production such as labour rates and imported chemicals & spares have also escalated.

Moreover, the name of the game remains the crop utilization level by the crushing industry, which reduces every time the industry foresees a surplus and a less-than-friendly Commerce ministry, disinclined to offer subsidy on export of surplus. Meanwhile, the industry’s narrative of enforced crushing under archaic regulations are well, just stories.

Already, murmurs are being raised that growers are demanding exorbitant rate against a minimum support price fixed at Rs 200 per 40 kg, which in effect absolves mills from procurement. That farmers would be tempted to demand a premium over base rate in a year of substantial crop surplus sounds disingenuous, as sooner or later they must be forced to sell off their produce to the only willing buyer, the mills.

Which brings us back to the primary argument: that the market players shall stay on short on sugar, which means the price volatility being witnessed currently is - in all likelihood - ephemeral. Why? Consider the following.

Earlier this week, SBP in its first quarterly report on State of the Economy has corroborated earlier estimates of bumper sugarcane crop with acreage, yield, and output all exceeding targets by handsome margin. Thus, even if the ‘reported’ utilization level meets the worst in two decades. i.e. 70 percent along with a below par recovery level at 9 percent, the country will still manage output no lower than last year levels. (For more, read “Time to go short on sugar, published by BR Research on 24 November, 2020)

This means that the market already has an upper ceiling for how high retail prices can go. And mind you, price escalation last year came on the back of mills bleeding due to high inventory carrying costs, which have declined substantially in the aftermath of discount rate reduction over past 9 months.

Thus, prices reverting to Rs 100 per kg is a near-impossibility, especially considering that the crop output witnessed this year is not an anomaly, but a trend reversion which may see another peak due to ratoon crop, fertilizer subsidy, and improved support price levels for growers.

About how low the prices may go, consider that mills can delay crushing to score raw material at best prices, but not refuse to crush cane altogether. And information asymmetry about production levels achieved during November and December can only be exploited for a limited time, as output data is periodically released through Large Scale Manufacturing index.

The only possibility then, is mills holding on to stocks to take advantage of prevalent low inventory carrying costs. But why should wholesaler/dealers give in to mills demand for higher ex-factory price, knowing that come March – marking the end of crushing – a commodity surplus is right around the corner.

For those in the government worried about recent price surge, dangling the stick of duty-free import quota – import volume has begun to wane since November 2020 – may just do the trick.

Comments

Comments are closed.