Shadab Textile Mills Limited (PSX: SHDT) was established in 1979 as a public limited company. The company’s principal business is manufacturing, selling, buying and generally dealing in all types of yarn.

Shadab Textile Mills set up its first spinning plant in Sheikhupura, Punjab, and has over time added to its capacity with the installation of spindles.

Shareholding pattern

Most of the shareholding of the company is concentrated with the directors, CEO, their spouses and minor children at 39 percent. Of this, Mrs. Fatima Aamir, one of the directors on the board of Shadab Textile Mills, holds almost 14 percent. The CEO, Mr. Aamir Naseem holds a little beyond 9 percent of the shares. About 55 percent of the shares are distributed with the local general public, while NIT& ICP and joint stock companies own 3 percent and 2.5 percent, respectively.

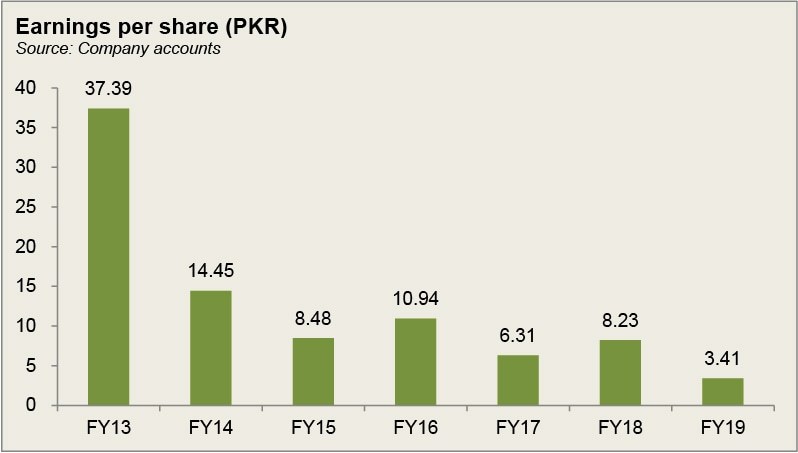

Historical operational performance

Apart from reducing once, the topline of the company has been increasing at varying growth rates. The profit margins, on the other hand, have been fluctuating, as the cost of production varies in the seven years.

During FY15, revenue registered a decline of close to 9 percent. This was attributed to a decline in unit sale price of yarn, both locally as well as in the international market. Note that yarn is one of the major products of the company. On the cost side, it had increased to consume more than 95 percent of the revenue, bringing profit margins down to the lowest seen since FY13. Most of the profitability was adversely affected due to unstable raw material prices and energy expense. Both these two expenses are the main cost drivers for the company.

Revenues grew marginally during FY16, increasing by less than 1 percent. The textile sector of Pakistan had faced intense competition in the international market, owing to a high cost of production, making products uncompetitive. Hence buyers shifted their demand to other regional players which offered lower prices. The company managed to reduce cost of production as a percentage of revenue slightly allowing margins to pick up. The cost of production saw a decline due to uninterrupted supply of energy and reduction in the electricity tariff in the second half of FY16. This is evident from the decrease in fuel and power expense by nearly 15 percent.

Growth in revenue saw some recovery as it increased by almost 10 percent in FY17. The continuous supply of energy helped the company to reduce its production losses and increase production. However, the increased revenue could not be reflected in the bottomline as the former was accompanied by a more than corresponding rise in costs. The availability of energy was through RLNG which is expensive. In addition, there was also rise in wages; thus both fuel and salaries expense saw the most change. As a result, the company saw its lowest profit margins in FY17.

Topline further increased by 11 percent in FY18 as yarn prices increased, while production improved due to better availability of energy. There was an only marginal incline in cost of production as a percentage of revenue; with most other factors remaining unchanged, there was a similar effect on profit margins. Over time, the company had been able to reduce its finance cost due to repayment of long term loans and utilizing internally generated funds for operation.

In FY19, Shadab Textile Mills registered its highest topline growth rate at nearly 24 percent. This was attributed to better selling price, better production and continuous supply of electricity. Cost of production as a percentage of revenue also reduced to 93 percent. This allowed profit margin to pick up, with operating and net margins doubling between FY18 and FY19, while the bottomline, at Rs 78 million, was the highest seen since FY14.

Although the company claims to be a known player in the international yarn manufacturers industry, its financial statements do not show export sales.

Quarterly results and future outlook

Between 9MFY20 and 9MFY19, revenue registered 1.6 percent decline, while the third quarter of FY20 saw a 9 percent decline year on year. This was attributed to the outbreak of Covid-19 and the resultant lock down. However, if one were to look at profitability, the company saw better profits in 9MFY not only year on year but also quarter on quarter. This was due to increase in yarn sale price exceeding the increase in raw material purchase price and other input costs. Some support was also brought in by other income, which was nil in 9MFY19.

Since the lock down was imposed in the last week of March, the full effect may be seen in the last quarter of FY20. However, in spite of the ongoing pandemic, the textile sector players have been unanimously asking for zero rating of the industry and support from the government in the form of continuous supply of energy at lower rates to ensure efficiency. The textile sector makes up a significant part of the country’s total exports; however, it has lost its competitive edge to the regional players, in the international market due to high costs.

Comments

Comments are closed.