Pak Elektron Limited (PSX: PAEL) was incorporated in Pakistan as a public limited company in 1956. The company is engaged in the manufacturing and sale of domestic appliances and electrical capital goods. The company organizes itself in two divisions – power and appliances. The company was acquired by Saigol Group of Companies in 1978. The company has formed several alliances over the years with renowned international companies including Hitachi, Fujitsu and General Electric.

Pattern of Shareholding

As of June 30, 2022, PAEL has a total of 856.012 million shares outstanding which are held by 11,702 shareholders. General public has the major stake of 48.36 percent in the company followed by its directors, CEO, their spouse and minor children holding 30.55 percent shares. Insurance companies hold 8.6 percent of PAEL’s shares while Banks, DFIs and NBFIs account for 5 percent shares. Around 3.15 percent of the company’s shares are held by joint stock companies and 2.46 percent by Modarabas & Mutual Funds. The remaining ownership is distributed among other categories of shareholders.

Financial Performance (2019-22)

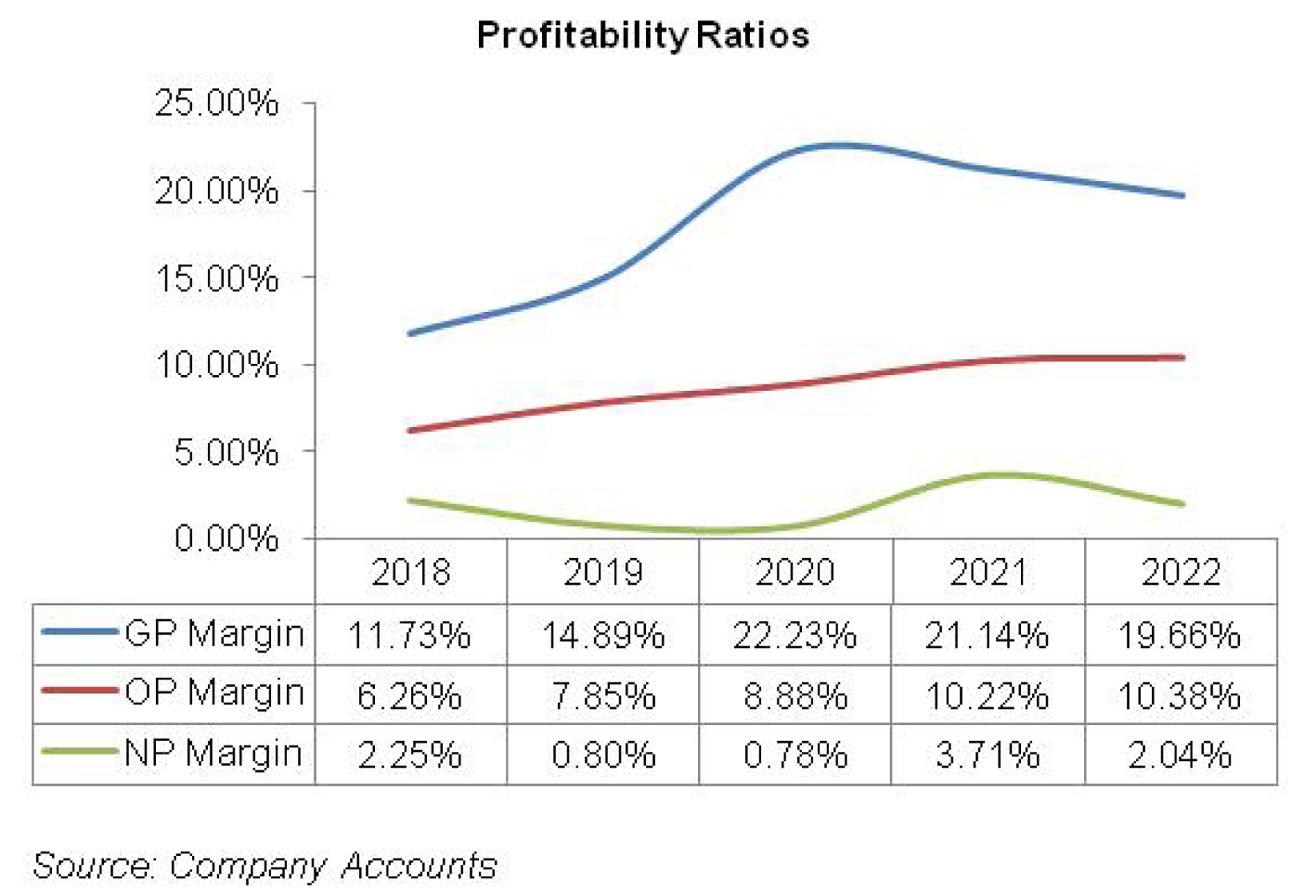

Barring 5 percent year-on-year dip in 2019, PAEL’s topline has been riding an upward trajectory until 2022. Conversely, its bottomline took a plunge twice i.e. in 2019 and 2022. PAEL operating margins posted a steady inclining trend in all the years under consideration. Its gross margin also followed the suite until 2020, however, plummeted thereafter. PAEL’s net margin inched up only in 2021 since 2018 only to slip back in 2022. The detailed performance review of each of the years under consideration is given below.

In 2019, PAEL’s topline slid by 5 percent year-on-year. Home appliances division registered a mild growth of 1.87 percent in its revenue 2019 as the company started the commercial operations of its washing machine production line during the year. Power division revenues slumped by 16 percent year-on-year which was the consequence of slow orders from WAPDA and DISCOS. Cost of sales also tumbled by 8 percent year-on-year in 2019, resulting in 21 percent year-on-year improvement in its gross profit during the year. GP margin also climbed up from 11.73 percent in 2018 to 14.89 percent in 2019. Distribution expense registered 30 percent year-on-year spike in 2019 primarily due to warranty period services as well as freight & forwarding charges. Administrative expense also surged by 13 percent year-on-year in 2019 due to higher payroll expense despite 10.68 percent shrinkage in its workforce which stood at 4321 employees. Other income also posted a noticeable 95 percent year-on-year rise in 2019 particularly due to gain on sale and lease back activities undertaken during the year. Operating profit rose by 19 percent year-on-year in 2019 with OP margin improving from 6.26 percent in 2018 to 7.85 percent in 2019. Finance cost grew by a massive 58 percent year-on-year in 2019 due to discount rate hike. This culminated into 66 percent year-on-year plunge in PAEL’s net profit in 2019 which stood at Rs.177.84 million. EPS also plummeted from Rs.0.98 in 2018 to Rs.0.27 in 2019. NP margin dropped from 2.25 percent in 2018 to 0.8 percent in 2019.

In 2020, PAEL’s topline posted a vigorous 29 percent year-on-year rise. During the year, the company witnessed three important milestones. Firstly, its wholly owned subsidiary, PEL Marketing Private Limited (PMPL) was amalgamated into PAEL. Secondly, the company’s power transformer manufacturing facility started its commercial operations. Finally, the company entered into collaboration with Panasonic Marketing Middle East & Africa (PMMAF). All these developments produced a profound impact on its sales and profitability. The outbreak of COVID-19 during 2020 had a devastating impact on the disposable income of company’s consumers. This was evident in a considerable decline in refrigerator, deep freezer and LED TV sales during the year. Power infrastructure related projects also remained lackluster during 2020 due to operational lockdown imposed on account of COVID-19. The topline growth came on the heels of a tremendous growth in the sale of water dispensers, energy meters, switch gears, power and distribution transformers, washing machine, AC and microwave oven. Cost of sales grew by 18 percent year-on-year due to high inflation, Pak Rupee depreciation and hike in the prices of POL products. However, higher sales on the power division front and the company’s ability to pass on the impact of cost hike to its consumers yielded 92 percent growth in gross profit in 2020 with GP margin moving up to 22.23 percent. Distribution expense registered a massive 146 percent spike in 2020 on account of higher salaries & benefits, advertising & sales promotion, freight & forwarding as well as warranty period services. 2020 marked 30 percent year-on-year increase in the number of employees which clocked in at 5616 during the year, resulting in a considerable rise in payroll expense which provided impetus to 148 percent year-on-year escalation in administrative expense during the year. Nevertheless, operating profit improved by 46 percent year-on-year in 2020 with OP margin climbing up to 8.88 percent. Finance cost surged by 43 percent year-on-year in 2020 despite monetary easing backdrop for the most part of the year. This was due to increased long-term borrowings obtained during the year which is also evident in a significant growth in PAEL’s gearing ratio in 2020 (see the graph of gearing ratio). This greatly diluted the bottomline growth which was recorded at 26 percent in 2020. PAEL’s net profit stood at Rs.223.85 million in 2020 with EPS of Rs.0.36. NP margin inched down to 0.78 percent in 2020.

The promising recovery post COVID is evident in 49 percent year-on-year increase in PAEL’s net sales in 2021. With robust economic recovery, industrial sector revival and rapid urbanization, PAEL’s power division posted 62 percent year-on-year growth in its revenues. Home appliances division’s revenues also magnified by 37.39 percent in 2021 particularly on the heels of tremendous rise in disposable income principally, agricultural income and foreign remittances. Cost of sales mounted by 51 percent year-on-year in 2021 which was the consequence of hiking inflation, supply chain disruptions, high global commodity prices, gas shortages and electricity tariff hike. While gross profit progressed by 42 percent year-on-year in 2021, GP margin ticked down to 21.14 percent. Distribution expense surged by 18 percent year-on-year in 2021 on account of increased freight & forwarding charges, advertising & sales promotion as well as salaries & benefits. Administrative expense also grew by 18 percent year-on-year in 2021, primarily on the back of higher payroll expense, as the number of employees grew by 2.9 percent year-on-year to clock in at 5745 in 2021. High profit related provisioning undertaken during the year resulted in 302 percent spike in other expense. Operating profit registered 71 percent year-on-year enhancement in 2021 with OP margin rising up to 10.22 percent. Finance cost slid by 1 percent in 2021 due to discount rate cuts and reduced borrowings, which is also evident in a slump in its gearing ratio. Net profit enlarged by 611 percent in 2021 to clock in at Rs.1591.076 million with EPS of Rs.2.89 and NP margin of 3.71 percent – the highest among all the years under consideration,

PAEL’s topline grew reasonably by 22 percent year-on-year in 2022. This was on the heels of 52.24 percent rise in power division revenues. Home appliances division posted a marginal decline of 0.74 percent in 2022 which signifies reduction in disposable income, product cost hike and sluggish economic backdrop which squeezed the purchasing power of consumers. Cost of sales spiraled by 24 percent year-on-year in 2022 on account of high inflation, global commodity super cycle, Pak Rupee depreciation and hike in energy tariff. Gross profit inched up by 14 percent year-on-year in 2022, however, GP margin slipped down to 19.66 percent. A mild 7 percent year-on-year growth in distribution expense in 2022 was the result of sky-rocketed freight & forwarding charges on account of high petroleum prices. While the workforce shrank by 14 percent to clock in at 4921 employees, payroll expense continued to mount in line with inflation, resulting in 15 percent year-on-year spike in administrative expense in 2022. During the year, PAEL’s export sales immensely boosted, yielding significant foreign exchange gain. This pushed up the company’s other income by 103 percent in 2022. As against the previous year, PAEL also booked impairment reversal on ECL worth Rs.241.88 million. As a consequence, operating profit built up by 24 percent year-on-year in 2022 with OP margin reaching its highest value of 10.38 percent. Finance cost soared by 42 percent year-on-year in 2022 due to excessive monetary tightening as well as enormous rise in working capital related borrowings. The company also issued 358.33 million ordinary shares during the year which compressed its gearing ratio. Higher finance cost coupled with the imposition of additional taxes during the year constricted PAEL’s bottomline by 33 percent year-on-year in 2022. Net profit stood at Rs.1067.47 million in 2022 with EPS of Rs.1.33 and NP margin of 2.04 percent.

Recent Performance (9MCY23)

During 9MCY23, PAEL net sales dwindled by 29 percent year-on-year. Drastic drop in the purchasing power of consumers due to hiking inflation took its toll on the sales of home appliances division. Furthermore, sluggish industrial activity also kept the power division sales under stress. Geographical breakup of sales shows decline in both local and export sales during the period. On supply front, import restrictions also contributed to lower production and sales during the year. Cost of sales plunged by 36 percent year-on-year in 9MCY23, translating into 3 percent lower gross profit when compared to the same period last year. However, as the company passed on the onus of high raw material cost and Pak Rupee depreciation to its consumers, it was able to attain GP margin of 26.55 percent in 9MCY23 versus 19.42 percent during the same period last year. Due to lower sales volume, distribution expense shrank by 18 percent year-on-year in 9MCY23. Conversely, administrative expense increased by 6 percent year-on-year during the period under review. PAEL was able to improve its operating profit by 3 percent year-on-year in 9MCY23 by keeping a check on its operating expense during the period. OP margin also improved from 10.27 percent in 9MCY22 to 14.98 percent in 9MCY23. Finance cost mounted by 27 percent year-on-year on account of unprecedented level of discount rate. This was despite the fact that the company significantly reduced its borrowings during the period by efficient working capital management. This resulted in 37 percent year-on-year decline in PAEL net profit in 9MCY23 to clock in at Rs.946.339 million. EPS also slid from Rs.1.98 in 9MCY22 to Rs.1.07 in 9MCY23. While PAEL was able to enhance its gross and operating margins during the period, hefty finance cost resulted in a net margin of 3.09 percent in 9MCY23 versus 3.46 percent in 9MCY22.

Future Outlook

With import restrictions largely eased and Pak Rupee riding a gradual recovery path, the company might not face supply side issues. However, as the inflation monster is rising its head up yet again due to massive rise in gas prices, the discount rate is expected to show no respite in the near-term. This will continue to take its toll on the economic activity, hence affecting PAEL’s power division sales. Moreover, radical decline in the disposable income of consumers gives no hope for improvement in home appliance division sales.

Comments

Comments are closed for this article.