FY22 has been benefitting the oil and gas exploration and production sector in Pakistan because of spiking international oil prices amid rising demand as well as geopolitics, and depreciation of local currency significantly. Oil and Gas Development Company Limited (PSX: OGDCL) in 1HFY22 has seen its profits rise due to the same factors.

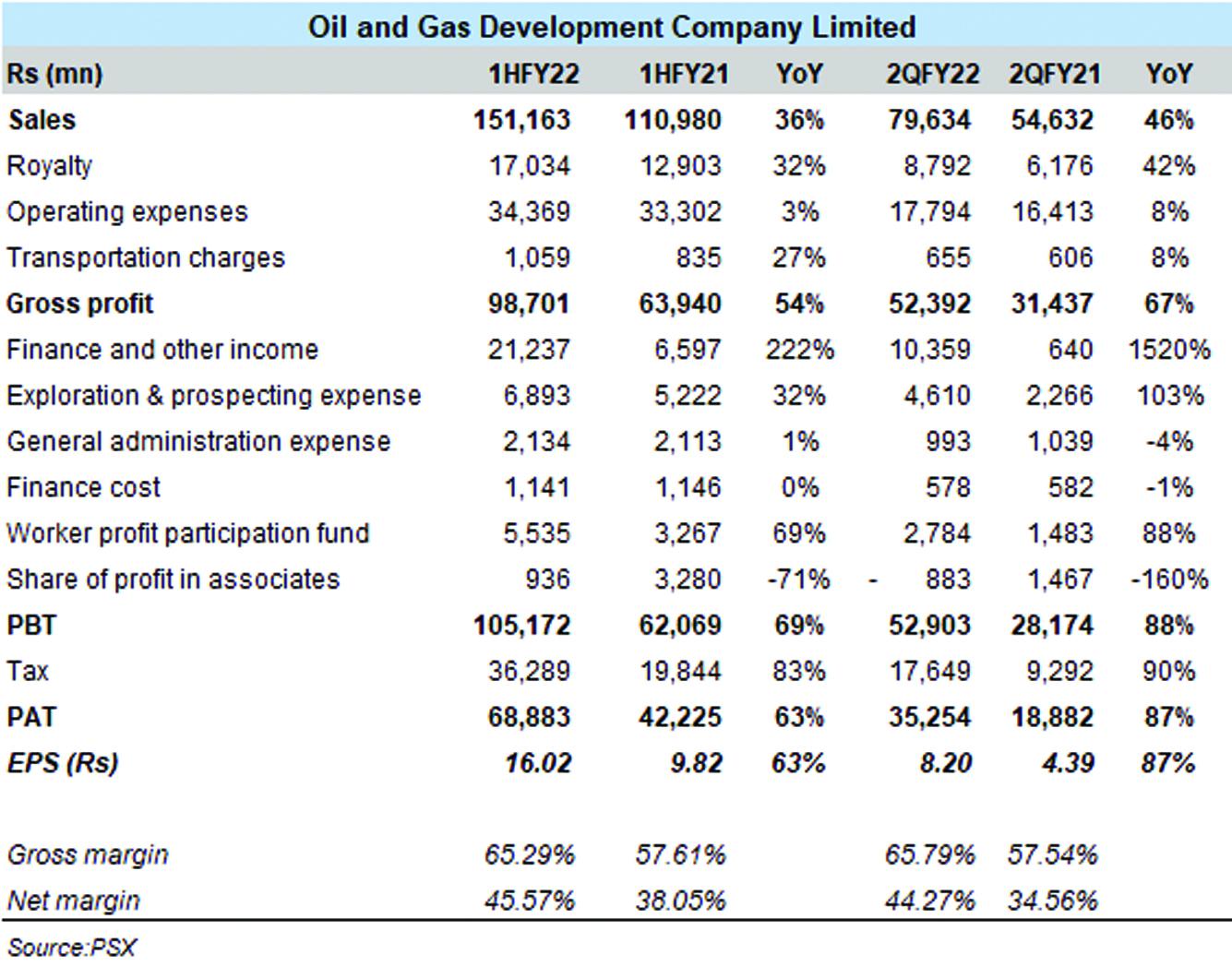

Starting with the topline growth, OGDCL’s revenues for 2QFY22 was grew by 46 percent year-on-year, while the bottomline growth stood at 87 percent year-on-year. Overall, first six month’s revenues climbed by 36 percent, while the earnings growth for 1HFY22 was recorded at 63 percent year-on-year.

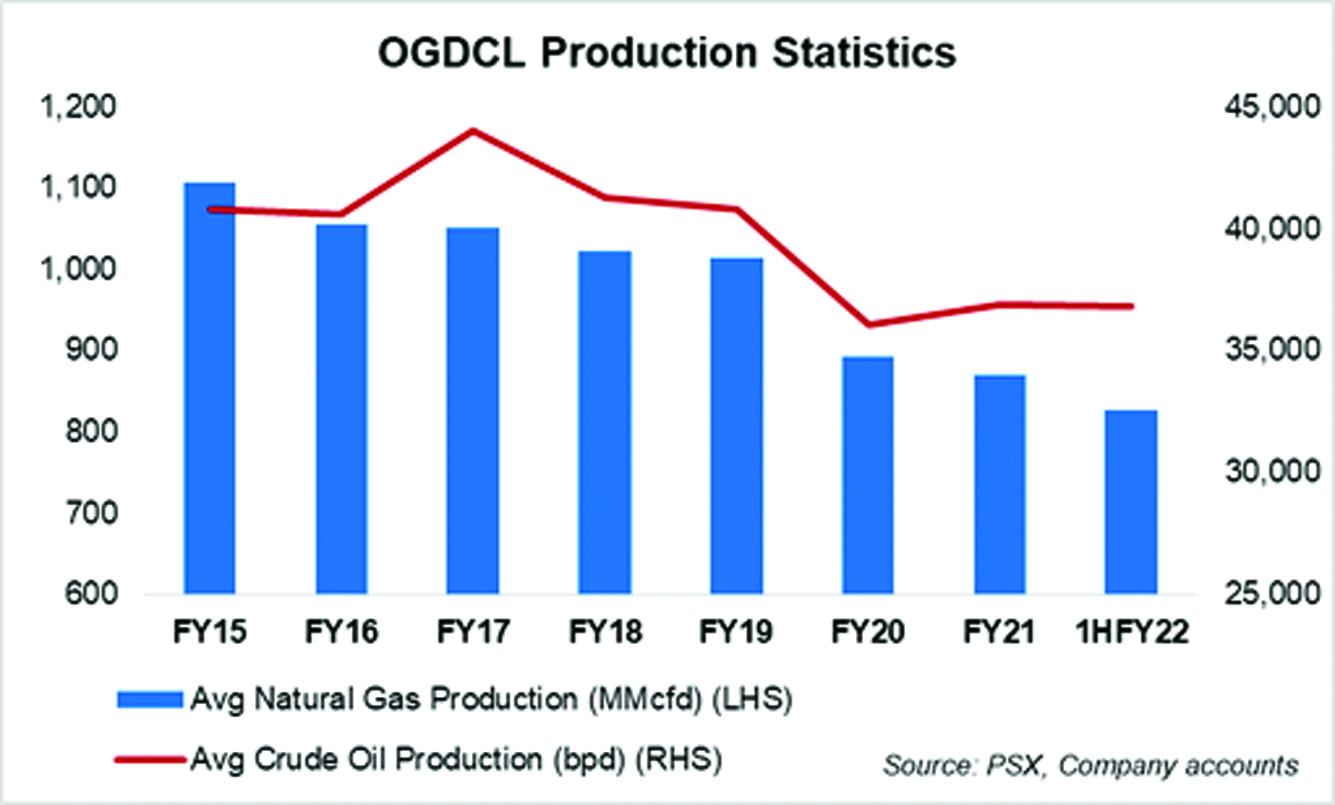

Topline growth was driven by a whopping 77 percent year-on-year rise in international crude oil prices along with three percent currency depreciation and slight uptick in crude oil production for OGDCL during 1HFY22. Average net realized price of crude oil increased by 63 percent year-on-year in 1HFY22, while that of natural gas sold was up by around 7 percent year-on-year. Crude oil production was up by one percent year-on-year; however, the natural gas production was down by 3 percent year-on-year in 1HFY22.

Growth in OGDCL’s bottomline was also lent significantly by the mammoth increase in other income due to hefty exchange gains from currency depreciation. On the expenditure side, two times increase prospection and exploration expenditure in 2QFY22 offset the decline of 23 percent year-on-year in 1QFY22- taking the 1HFY22 expense up by 32 percent. OGDCL spud six wells including four exploratory wells and two development well. It also made four discoveries.

Oil prices have continued to drive earnings for the E&P sector and the prices are not coming down anytime soon. Currency depreciation has been a companion in driving the E&P sector’s earnings. WACOG could bring a breather to the receivables of the EP companies, which could unlock production prospects as more room (cash) will be available to undertake drilling and prospecting activities.

Comments

Comments are closed.