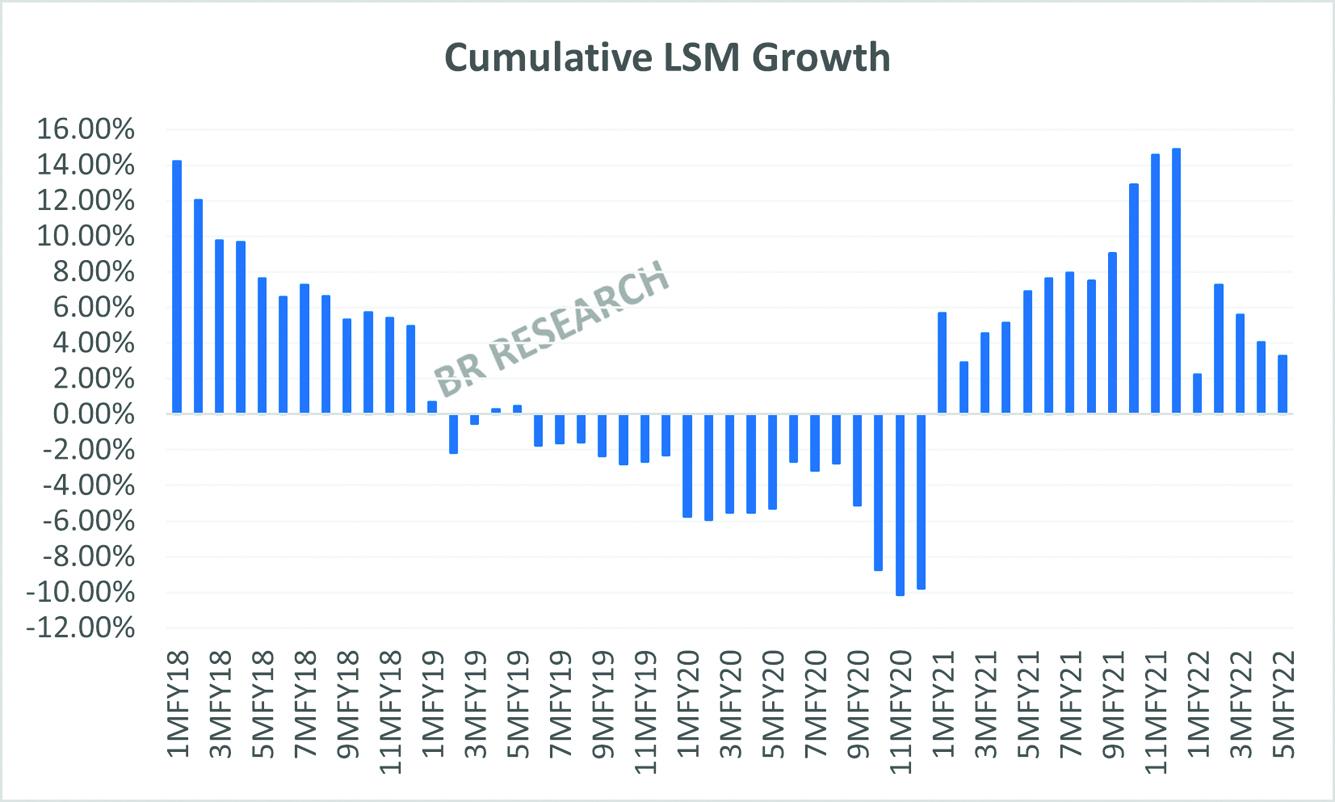

The LSM growth in November 2021 came down to 0.29 percent – lowest year-on-year number since August 2020. Having hit the double-digit highs in FY21, it was always going to be a matter of time before LSM lost the steam, as higher based kicks in. The central bank governor sees the bright side of near zero LSM growth, terming it “good news as it tells the growth is sustainable”.

Now, one is not too sure how these middling numbers show a sign of sustainable growth, especially when the previous round of increase was mostly rooted in the low base arising out of Covid. Before reading too much in the November LSM and calling it “moderation of economic activities”, it would be wise to keep in mind that early sugar crushing in 2020 had led to a higher than usual sugar production in November. The return to normalcy for the ongoing crushing season has led to a 27 percent year-on-year decline in sugar production. Sugar has the single highest weight in the LSM food category.

Even with the marginal year-on-year growth, November 2021 index has returned the highest-ever monthly value, keeping with the 2021 trend, where eight of the 11 months have recorded all-time monthly highs. In terms of sectoral contribution, automobiles continue to headline the growth, with the biggest contribution, despite less than 5 percent weight in the index. Jury is out on what the future holds for automobile demand, but there are early signs that price increase, and increased cost of auto financing will put a lid on the double-digit automobile demand, going into 2H FY22.

Iron and steel products, with 5 percent weight, are second in line in term of contribution, as the low base remained in play for much longer. The euphoria around construction industry seems to be cooling off, as evident from cement production numbers, which have plateau during 5MFY22. The other significant contributor to the LSM growth is the wood product category, with a negligible share of 0.6 percent in weight. The 200 percent growth will count for much less once the PBS starts publishing LSM numbers with the new and improvised base – where share of wood has been reduced to a third.

It remains to be seen how the LSM growth for 5MFY22 transpires with the new base, but if FY21 numbers are any guide, the revision could well be on the downside. Elements such as wearing apparel have made an entry into the LSM index, and that has worryingly shown a negative growth, which is likely to further dent the period growth in the new base. Let us not forget, large scale industrial activity, even after the double-digit FY21 growth is nowhere close to the highs of FY17-18. With energy prices slated to stay higher, the “moderation” in growth could kick in quicker.

Comments

Comments are closed for this article.