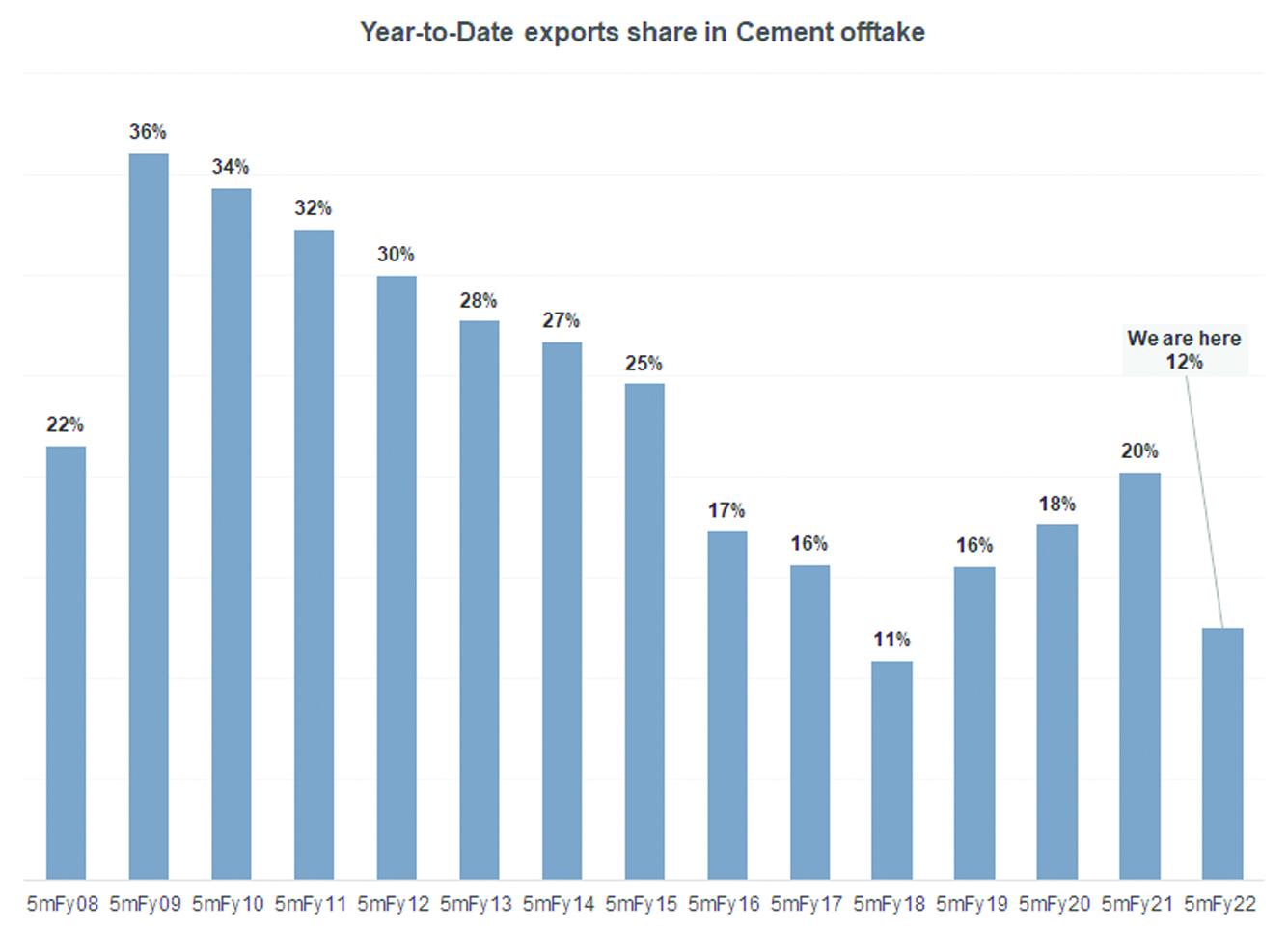

Though cement manufacturers are really counting on domestic demand—on the back of which a whole lot of them are investing large sums of money into capacity expansion—offtake thus far leaves a lot to be desired. Historically, when domestic demand is booming, exports take a backseat and when domestic demand is slowing down, exports contribute a critical share in total offtake. It makes more economic sense to sell domestically where prices are more desirable and less competitive. Naturally, the desire to sell abroad only becomes urgent when domestic demand is not keeping up with expectations. It serves as a buffer, but an important one. The short-term outlook for this year is not great.

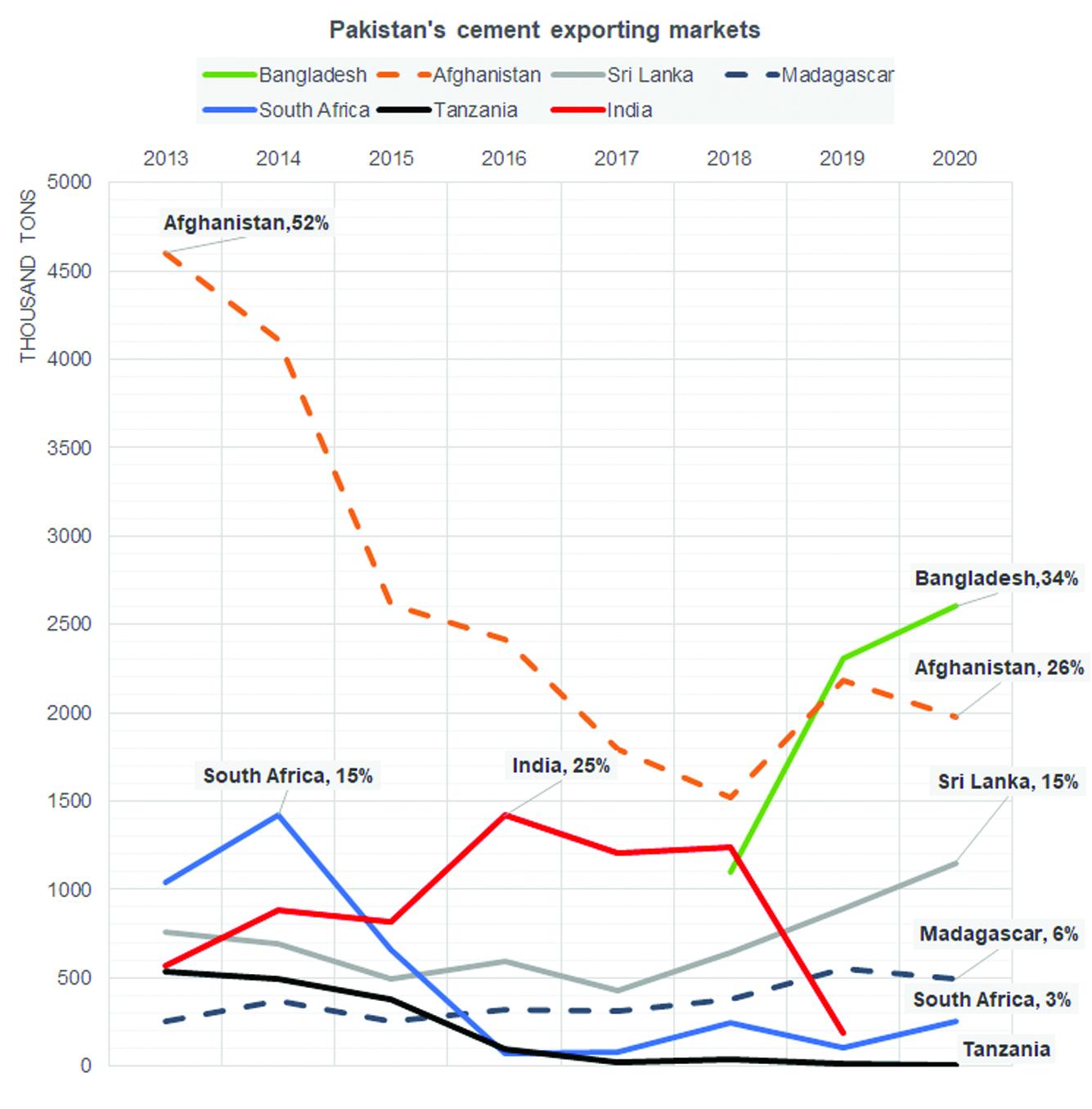

Volumetric and dollar value exported per ton data from Pakistan Bureau of Statistics (PBS) shows that in most months of FY22, exports have fallen year on year. Exports fetched a higher price this year, compared to the previous year (see graph). This is because clinker exports have weakened in key markets which on average fetch $10-12 per ton less than cement exports. Cement buyers are also paying a higher cost of freight since Covid-19 hit where freight rates have grown 4-5x over the past year. For Pakistani exports, there is also a visible shift in markets where once Afghanistan used to dominate but has since become a less receptive market.

Only a few years ago, Pakistan was the biggest supplier of cement to Afghanistan. The share began to drop significantly when Iranian cement found its way into Afghan markets. This necessitated Pakistani cement makers to try selling and increasing outreach to other regional as well as far-off markets. South Africa, India, Sri Lanka and other African markets came to the rescue as exports to Afghanistan dropped.

But until recently, Pakistan was still exporting a large quantity of cement to Afghanistan. Now the situation is direr given the ongoing political turmoil in that country which has caused massive uncertainty in how soon that market may recover. Meanwhile, exports to India were almost banned in 2020 given triple-digit countervailing duties imposed on Pakistani goods. In 2017, cement exports to India constituted 30 percent of total exports; in only three years, that market has all but vanished.

Pakistan was also exporting significant tons of cement to South Africa. By 2014, the share of South Africa in total exports had grown to 16 percent, but in 2016, South Africa slapped anti-dumping duties on Pakistani cement having found its domestic industry under injury due to dumping from Pakistan. Exports to that market fell like a lead ball since then. These duties were supposed to be lifted this year, but exports have not resumed as much due to outcries from South African cement manufacturers. At the same time, one of the biggest cement exporting nations Vietnam grabbed this opportunity to establish its roots in South African markets. Most recently, in a bid to protect domestic manufacturers, South African government has imposed an outright ban on imported cement for state projects i.e., all public-sector projects will procure only local South African cement.

With South Africa and India out, and Afghanistan under conflict situation, cement exports have to be diverted elsewhere. Clinker to Bangladesh and cement to Sri Lanka started to become more feasible options, except right now, the Sri Lankan economy is undergoing an economic crisis of epic proportions. The country has no funds available and is facing significant food inflation. Half a million people have sunk in poverty during the pandemic and current financial crisis could lead the country into bankruptcy.

This means, Pakistani cement exporters to the country can bid farewell to any dollars coming from Sri Lanka at least for now.

That leaves other African countries like Kenya, Madagascar, Mozambique and Tanzania among others, but historically these markets have not contributed more than 5-6 percent in Pakistani cement exports.

They will have to do for now as traditional markets recover. Though, few hopes should be latched onto Sri Lanka, India or even Afghanistan this year.

Last month in November, exports grew not only month on month but year on year but there are very few regional markets left for cement makers to reasonably sell to. The pressure on domestic economy taking off is on, but is it? (Read more: “Construction and Housing: Boom, doom or bust”, Dec 31, 2021).

Comments

Comments are closed.