Pakistan Bureau of Statistics’ monthly CPI bulletin for September-2020 published last weekend had a curious illustration. The PBS especially highlighted the rise in prices of broiler chicken and tomatoes, illustrating the contribution of these perishables to higher month-on-month increase in inflation.

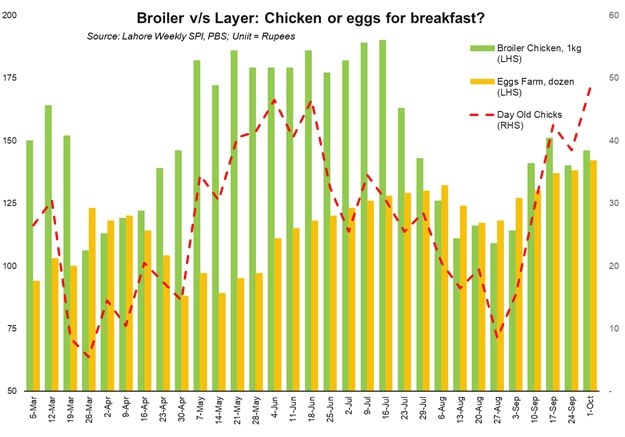

Periodic increases in perishable prices do not pose a serious challenge to the administration, as the volatility in prices goes both ways. Afterall, fluctuations caused by disruptions in supply chain of perishables have a way of eking themselves out over time. Consider that since the beginning of calendar year, Pakistan has seen national average broiler prices as low as Rs 125 per kg and as high as Rs 225 per kilo; September CPI average of Rs 150 is in fact still lower than YTD average of Rs 170.

But what really fuels the maddening rollercoaster that is broiler chicken prices? Are poultry farmers so disconnected from the demand side that they can rarely tell which way the prices might swing over the next 4 weeks? Or is the seasonality effect in poultry supply chain so critical that little - if nothing - can be done to even out prices throughout the year?

Various industry sources claim that the feed cost constitutes between 70 – 90 percent of cost of raising poultry. If those estimates are to be believed, then the multiple peaks and troughs witnessed in bird prices in less than 12 weeks appears counterintuitive.

Why? Because feed consists of mostly non-perishable grains such as maize, meals made of imported oilseeds such as soybean, rice/corn gluten, cotton seedcakes, with a small component of vitamins, vaccines, and antibiotics. As most inputs are storable and harvested seasonally, most poultry businesses – whether organized or otherwise - must follow principles of cost minimization by buying low during harvest season or in times of surplus supply.

Does that mean the final price of bird meat represents market-based price discovery mechanism working at its best, fluctuating on day-to-day basis in the throes of supply and demand palpitations? Of course, the seasonality effect looms large on broiler prices, as demand peaks around religious festivities of Ramzan and Eid ul Fitr, and bottoms out after Eid ul Azha – the red meat bonanza. But what explains the wild fluctuations outside those three months?

Then, there is the summer vacations, and winters wedding season – compounded this year by the lifting of lockdown and restrictions on social gatherings beginning September. That poultry prices were set to rebound as a result - after kissing bottom in August - was predicted in this space exactly a month ago (For more, read “Broiler: time for a rebound, by BR Research, published on August 09, 2020). But that raises an obvious question: if the seasonality effect is so predictable and cost of inputs also (relatively) stable, why has the market not worked out a mechanism to offer a steady price throughout the year?

It appears that the missing link is the price of Day-Old Chicks (DOC). A lull period means the meat would sell at a lower price point, even though cost of production is relatively stable through all the peaks and troughs of demand. Because all ‘living’ chicks must grow into fully fed birds, farmers have no choice but to cull the surplus chicks whenever they foresee a looming slowdown in meat demand, instead of bearing the 90 percent variable cost component – the feed cost.

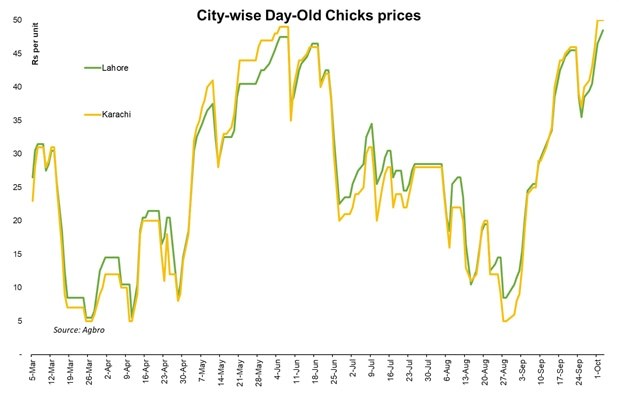

DOC prices thus have become the pass-through component in bird meat prices. In the past 6 months, DOC price in Lahore has fallen to as low as Rs 5 per unit, only to climb back 10 times to Rs 50! Meanwhile, the difference between maximum and minimum retail price of broiler chicken in the provincial capital during the period is Rs 90! And that cycle has taken place at least twice since March 2020 (and not for the first time in recent years).

Because poultry prices are cyclical, a near hundred rupee variation in bird meat prices in less than 4 months does not raise the same hue and cry as does a permanent increase of Rs25 in price of a kilo wheat or sugar, stretched out over a year.

But consider this: the wild ride of bird meat is only a distraction. In the past two years, price of dozen eggs have increased by over one-third. And unlike bird meat, price of eggs has a tendency of inching forward permanently.

Turns out, in the eternal question of egg or chicken, chickens do come first. At least in the measurement of inflation.

Comments

Comments are closed for this article.