The Federal Government presented Finance Bill, 2023(‘FB’) in the National Assembly on June 9, 2023. After the debate in the Senate and National Assembly, the Government has passed Finance Act, 2023(‘FA’) with certain modifications/amendments made in the FB.

The amendments made in the fiscal laws by the FA are made effective from July 1, 2023 unless otherwise specified.

This Memorandum summarises major amendments made in the FB whilst passing the FA.

==========================================================

S. Engine Existing Revised Tax/

No. Capacity Tax Rate of Tax

==========================================================

1 Upto 850cc Rs 10,000 Rs 10,000

2 851cc to 1000cc Rs 20,000 Rs 20,000

3 1001cc to 1300cc Rs 25,000 Rs 25,000

4 1301cc to 1600cc Rs 50,000 Rs 50,000

5 1601cc to 1800cc Rs 150,000 Rs 150,000

6 1801cc to 2000cc Rs 200,000 Rs 200,000

7 2001cc to 2500cc Rs 300,000 6% of the Value

8 2501ccto 3000cc Rs 400,000 8% of the Value

9 Above 300occ Rs 500,000 10% of the Value

==========================================================

INCOME TAX

ADDITIONAL TAX ON WINDFALL INCOME

Through the FB, a new provision was proposed to empower the Federal Government to impose additional tax on persons or classes of persons who have any income, profits or gains arisen due to any economic factors that resulted in windfall income, profits or gains.

The proposal has been retained by FA with following amendments:

=======================================================================

Description Current Amended

=======================================================================

-number of days-

=======================================================================

Constitution of committee 45 days of receipt days of receipt

of applica15 of application

Decision in dispute 120 days 45 days, extended

by 15 days

=======================================================================

i) The applicability of the said tax has now been restricted to companies only operating in specified sectors;

ii) The retrospective application of the said tax has been reduced from five (5) years to three (3) years preceding the tax year from tax year 2023 and onwards; and

iii) Federal Government notification for determination of windfall income and the economic factors resulting in an income subject to tax under this section is now required to be placed before the Parliament within ninety (90) days of notification or June 30 of the financial year, whichever is earlier.

The legal challenges to the implementation of these provisions are still not addressed which may arise on certain constitutional grounds and principles laid down by the Superior Courts particularly with regard to past and closed transactions.

TAX ON DEEMED INCOME UNDER SECTION 7E

Through the Finance Act, 2022, a resident individual owning immovable properties in Pakistan is subjected to tax on deemed income from such properties for tax year 2022 and onwards. Such deemed income is effectively taxed at 1% of the FBR values of immovable properties. The said tax is not applicable on certain immovable properties which inter alia include the following:

==========================================================================================================

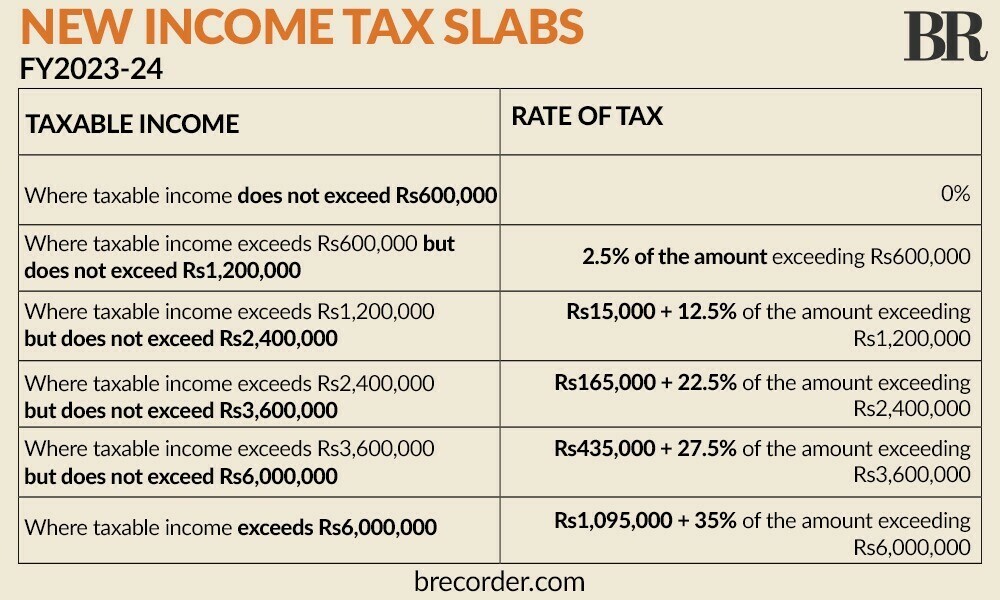

Sr No. Taxable income Existing Rates New Rates

==========================================================================================================

1. Where the taxable income does not Rs. 0 Rs. 0

exceed Rs 600,000

2. Where the taxable income exceeds Rs 2.5% of the amount 2.5% of the amount

600,000 but does not exceed Rs exceeding Rs 600,000 exceeding Rs 600,000

1,200,000

3. Where the taxable income exceeds Rs Rs 15,000 + 12.5% of the Rs 15,000 + 12.5% of the

1,200,000 but does not exceed Rs amount amount

2,400,000 exceeding Rs 1,200,000 exceeding Rs 1,200,000

4. Where the taxable income exceeds Rs Rs 165,000 + 20% of the Rs 165,000 + 22.5% of the

2,400,000 but does not exceed Rs amount amount

3,600,000 exceeding Rs 2,400,000 exceeding Rs 2,400,000

5. Where the taxable income exceeds Rs Rs 405,000 + 25% of Rs 435,000 + 27.5% of the

3,600,000 but does not exceed Rs the amount amount

6,000,000 exceeding Rs 3,600,000 exceeding Rs 3,600,000

6. Where the taxable income exceeds Rs Rs 1,005,000 + 32.5% of

6,000,000 but does not exceed Rs the amount

12,000,000 exceeding Rs 6,000,000

Rs 1,095,000 + 35% of the

7. Where the taxable income exceeds Rs Rs 2,955,000 + 35% of the amount

12,000,000 amount exceeding Rs exceeding Rs 6,000,000

12,000,000

==========================================================================================================

a) one immovable property owned by the resident person;

b) any property from which income is chargeable to tax under the Ordinance and tax leviable is paid thereon;

c) immovable property in the first tax year of acquisition where tax under section 236K has been paid;

d) where the fair market value of the properties in aggregate excluding certain specified properties does not exceed Rupees twenty-five million

By way of an amendment through the FA, the abovementioned assets will only be excluded from the purview of tax on deemed income if the name of the person holding such properties is appearing on the Active Taxpayers’ List (ATL). However, if any person is not required to file a return of income and obtain certificate to that effect as provided under the Tenth Schedule then such person would not be liable to pay tax on deemed income under section 7E despite not appearing on the ATL.

If the tax liability under section 7E is not discharged, then the registrar or the person registering the transfer is required not to register the transfer of the subject property.

ADVANCE TAX ON PURCHASE/SALE/ TRANSFER OF IMMOVABLE PROPERTY

The rate of advance tax to be collected from buyer or seller on purchase/sale/transfer of property has also been increased from 2% to 3%. As a result, rate of tax on those not appearing on the ATL will also be increased as under:

=======================================================================

Annual taxable Tax Year 2023 Tax Year 2024 Excess tax

Income

=======================================================================

600,000 - - -

1,200,000 15,000 15,000 -

2,400,000 165,000 165,000 -

3,600,000 405,000 435,000 30,000

6,000,000 1,005,000 1,095,000 90,000

12,000,000 2,955,000 3,195,000 240,000

=======================================================================

(i) On purchase of property - from 7% to 10.5%

(ii) On sale of property - from 4% to 6%

CAPITAL MARKET

a) Public Offering

Through the Finance (Supplementary) Act, 2023, capital gains arising on disposal of shares of listed company which is made otherwise than through stock exchange and which are not settled through NCCPL, is taxed under section 37 of the Ordinance. The said amendment had resulted in unwarranted tax implications on public offerings of listed securities.

Through an amendment made by the FA, disposal of shares through initial public offer during the listing process will remain subject to tax under section 37A of the Ordinance provided the details of such disposalare furnished to NCCPL for the computation of Capital Gains and tax thereon.

b) Securities acquired prior to July 1, 2013

At present, capital gains arising on disposal of securities that are acquired before July 1, 2013are subject to tax at the rate of 12.5%.

Through FA, capital gains arising on disposal of such securities will be subject to tax at 0%. The said amendment has resolved the unwarranted anomaly arisen due to an amendment made through the Finance Act, 2022.

PERMANENT ESTABLISHMENT (PE)

The FB proposed certain changes in the definition of PE which has been further amended by the FA to include virtual business presence in Pakistan including any business where transactions are conducted through internet or any other electronic medium, with or without having any physical presence.

Non-residents covered by Double Tax Treaties (DTT) will not be affected by the changes made through FA and consequently their PE status will continue to be determined under the DTT provisions.

ADVANCE TAX ON CONSTRUCTION / DISPOSAL OF BUILDINGS AND PLOTS

An amendment has been made in section 147 through FA, which requires payment of advance tax on project-by-project basis in four equal instalments by persons deriving income from business from the following:

i) construction and disposal of residential, commercial and other buildings

ii) development and sale of residential, commercial and other plots

The said advance tax is required to be discharged by the dates prescribed for corporate and non-corporate persons, as the case may be. The rates prescribed for advance tax are aligned with the tax rates applicable on builders and developers who opted to be taxed under section 100D read with Eleventh Schedule.

Builders or developers in respect of projects registered / covered under the Eleventh Schedule will continue to discharge their tax liability (including advance tax) under the said Schedule. However, for projects which are not registered / covered under the Eleventh Schedule, the advance tax liability under section 147 will be discharged as stated above whilst their taxability will be governed under normal provisions of the law.

ADVANCE TAX ON MOTOR VEHICLES

Through the FA, the rate of advance tax collected on registration of motor vehicle by motor registration authority or by the manufacturer on sale of motor vehicle has been amended as under:

For the purpose of advance tax, the value of motor vehicle above 2000cc will be as follows:

i) Imported vehicle – value assessed by the customs authorities as increased by the customs duty, federal excise duty and sales tax payable at import stage

ii) Locally manufacture/assembled vehicles – invoice value inclusive of all duties and taxes

iii) Auctioned vehicle – the auction value inclusive of all duties and taxes

There is no change in rate of advance tax collected on transfer of registration of motor vehicle.

ADVANCE TAX ON CASH WITHDRAWAL FROM NON-FILERS

Adjustable advance tax on cash withdrawals of non-filers was reintroduced through the FB at the rate of 0.6% where the sum of the payments for cash withdrawal in a day exceeds Rs 50,000. Since the said tax is applicable on non-filers only, therefore, corrective amendment has been made in the Tenth Schedule to avoid duplicate implications.

THRESHOLD FOR SALARY PAYMENT OTHERWISE THROUGH BANKING CHANNEL

Presently, salary payments exceeding Rs 25,000 per month are not allowed as admissible deduction while computing income from business.

The said limit is now enhanced to Rs 32,000 per month.

ALTERNATIVE DISPUTE RESOLUTION (ADR)

The concept of ADR was introduced in the law to avoid protracted litigation and delay in settlement of cases. This mechanism was introduced in parallel with taxpayer’s right to appeal before appellate forums.

Despite of various amendments made over the years; this forum has not achieved the desired results.

To make this forum effective, following amendments have been made through the FA:

Under the revised mechanism, the committee shall include a retired judge, not below the rank of a judge of a High Court, who shall also be the Chairperson of the Committee. The retired judge would be nominated by FBR from the panel notified by the Law and Justice Division. The other two members of the Committee shall be the concerned Chief Commissioner Inland Revenue and a person to be nominated by the taxpayer from the panel notified by FBR.

Presently, the taxpayer needs to withdraw his appeal for seeking relief under the ADR. Under the revamped procedure, the taxpayer, if satisfied with the ADRC decision, is required to withdraw appealand communicate the withdrawal to the Commissioner within 60 days of the ADRC decision.

Presently, the offer of tax payment made by taxpayer in initial proposal for resolution of dispute, accompanied with the application for ADR, is irrevocable. Through amended provisions, such offer would not be binding.

Under the amended mechanism, the decision of the Committee shall only be binding upon the Commissioner if the taxpayer has withdrawn the appeal and has communicated the same to the Commissioner within 60 days of service of decision of the Committee. In such circumstances, Commissioner is also required to withdraw his appeal within 30 days of appeal withdrawal notice from the taxpayer.

Time period for the appointment of Committee as well as time period prescribed for the decision of the dispute has also been reduced in the following manner:

Similar amendments have been made in the Sales Tax Act, 1990 and the Federal Excise Act, 2005. In the Customs Act, 1969, amendments on above lines were made through the Finance Act, 2020 except for appointment of a retired judge as member of the ADRC which has now been made through the FA.

AMENDMENTS PROPOSED THROUGH THE FB BUT NOT ADOPTED IN THE FA:

Following amendments proposed in the FB have not been adopted in the FA:

=============================================================================================================

Sr No. Taxable income Existing Rate New Rate

=============================================================================================================

1. Where the taxable income does not exceed Rs 0% 0%

600,000

2. Where the taxable income exceeds Rs 600,000 5% of the amount 7.5% of the amount

but does not exceed Rs 800,000 exceeding Rs exceeding Rs

600,000 600,000

exceeding Rs 600,000

3. Where the taxable income exceeds Rs 800,000 Rs 10,000 + 12.5% Rs 15,000 + 15% of

but does not exceed Rs 1,200,000 of the amount the amount

exceeding Rs exceeding Rs

800,000 800,000

4. Where the taxable income exceeds Rs 1,200,000 Rs 60,000 + 17.5% Rs 75,000 + 20% of

but does not exceed Rs 2,400,000 of the amount the amount

exceeding Rs exceeding Rs

1,200,000 1,200,000

5. Where the taxable income exceeds Rs 2,400,000 Rs 270,000 + 22.5% Rs 315,000 + 25% of

but does not exceed Rs 3,000,000 of the amount the amount

exceeding Rs exceeding Rs

2,400,000 2,400,000

6. Where the taxable income exceeds Rs 3,000,000 Rs 405,000 + 27.5% Rs 465,000 + 30% of

but does not exceed Rs 4,000,000 of the amount the amount

exceeding Rs exceeding Rs

3,000,000 3,000,000

7. Where the taxable income exceeds Rs 4,000,000 Rs 680,000 + 32.5%

but does not exceed Rs 6,000,000 of the amount

exceeding Rs

4,000,000

8. Where the taxable income exceeds Rs 6,000,000 Rs 1,330,000 + 35% Rs 765,000 + 35% of

of the amount the amount

exceeding Rs exceeding Rs

6,000,000 4,000,000

=============================================================================================================

1) Enhancement of monetary limit for immunity on foreign remittances received from abroad through permissible channels from Rs 5 Million to an amount equivalent to USD 100,000 per annum.

2) Reduction of minimum turnover tax from 1.25% to 1% for listed companies.

3) Tax credit for tax years 2024 to 2026 for an individual on construction of a new residential house.

4) Extension in period of exemption on profits and gains on the sale of immoveable property or shares of Special Purpose Vehicle to any REIT scheme from June 30, 2023 to June 30, 2024.

5) Reduction in tax liability on income from new construction projects to a ‘builder’.

6) Reduction in tax liability on income from business of a youth enterprise.

7) Increase in the threshold of Special Tax Regime for SME having turnover up to Rs 800 Million (from Rs 250 Million) and inclusion of persons engaged in the provisions of IT services and IT enabled services under the said Special Tax regime. Conditional tax holiday for SMEs setup exclusively as Agro based industry in a rural area.

8) Reduction in tax liability of a banking company on income arising from additional advances to certain specified sectors.

9) Non-applicability of advance tax on purchase of immovable property by overseas Pakistanis through Roshan Digital Account.

INCOME TAX SCHEDULES

INCREASE IN TAX RATES FOR NON-CORPORATE TAXPAYERS

There was no proposal for increase in the rate of tax for individual and Association of Persons in the FB. Through the FA, the rate of tax for tax year 2024 and onwards has been increased as under:

===================================================

Annual Tax Year Tax Year Excess

Taxable 2023 2024 tax

income

===================================================

600,000 - - -

800,000 10,000 15,000 5000

1,200,000 60,000 75,000 15,000

2,400,000 270,000 315,000 45,000

3,000,000 405,000 465,000 60,000

4,000,000 680,000 765000 85,000

6,000,000 1,330,000 1,465,000 135,000

===================================================

Flat increase of 2.5% in the tax rates applicable on salaried individuals earning more than Rs 2.4 Million per annum with highest slab rate of 35% starting from Rs 6 Million per annum (previously Rs 12 Million).

Flat increase of 2.5% in the tax rates applicable on non-salaried individuals and AOPs earning more than Rs 600,000 per annum with highest slab rate of 35% starting from Rs 4 Million (previously Rs 6 Million).

SALARIED INDIVIDUALS (COMPARISON OF EXISTING AND NEW RATES)

The impact of the above-mentioned changes is illustrated as under:

NON-SALARIED INDIVIDUALS / AOPs (COMPARISON OF EXISTING AND NEW RATES)

The impact of the above-mentioned changes is illustrated as under:

(To be Continue)

Copyright Business Recorder, 2023