Reading LSM’s Dec jump

December 2019 was a good month for large scale manufacturing. Or so it seems. Measured by the LSM index released monthly by Pakistan Bureau of Statistics, large scale manufacturing index jumped about nine and a half percent year-on-year in December 2019, raising hopes that the worst is over for the country’s manufacturing sector.

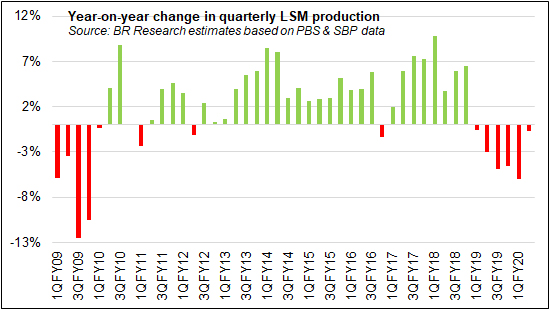

Before being blinded by optimism and hope, however, some stocktaking is warranted. Let there be no doubt that production output of Pakistan’s manufacturing sector has contracted for six quarters in a row, even as growth in December 2019 ended up improving 1HFY20 performance. LSM index had fallen 5.9 percent by 5MFY20. However, 1HFY20 now stands at a negative 3.35 percent.

At some level, optimism may be justified. As the graphs here show, the worst seem to be over for POL products, automobile sector, and cement. But the anatomy of LSM’s December growth reveals that it is essentially the food sector that has posted growth, led by sugar. In terms of point contribution, the nearly 100 percent growth in sugar production alone accounts for about a third of total LSM growth in December 2019. But sugar’s may be a false promise.

Sugar production almost doubled in December 2019 due to thinning carryover stocks that led to early crushing relative to last year. Thanks to lower acreage under sugarcane crop, at best sugar production will remain flat-lined during FY20, assuming average recovery rate remains constant, which is a safe assumption to make at this point.

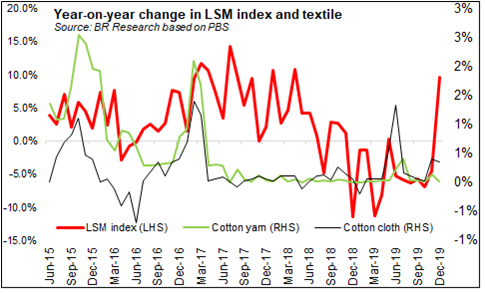

Meanwhile, growth in other LSM index heavy weight items, such as cotton yarn and cloth remains poor – as it has since March 2017 – whereas growth trends in some industries – such as cooking oil – is difficult to project based on LSM trends, since the LSM does not adequately represent total production in these industries.

Sans food, beverages & tobacco, December 2019 growth is almost flat: 0.74 percent. That too offers some hope, at least as much as catching on the straws considering that December’s was the first positive year-on-year tick in LSM since July 2018. But whether these hopes will gain roots or whether these will be dashed depends on January 2020 output, data for which will be reported next month.

It is quite likely that the sugar-high visible in December will not be as much in January 2020, whereas all other sectors will remain weak or show marginal growth on account of low base affect. But given LSM’s broad-based nature of contraction, the absence of growth-drivers and the continuation of high interest rates, government’s LSM growth target of 1.3 percent for FY20 is still not likely to be met. (See also Manufacturing recession: five quarters and counting, Jan 21,2020)

Comments

Comments are closed.