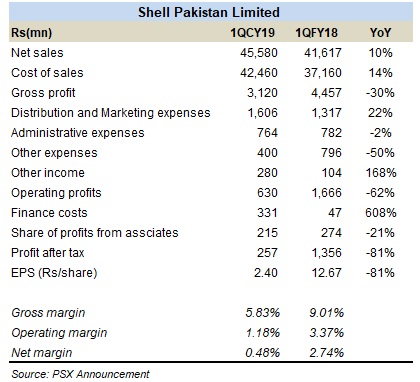

Shell Pakistan Limited (PSX: SHEL) announced its financial performance for the first quarter of 2019 earlier this week with s significant year-on-year plunge in earnings. The oil company’s net revenues were up by 10 percent, but more than proportionate increase in the cost of sales made the gross profits decline by 30 percent. This was because of significant inventory losses that the company faced during the quarter.

Shell’s bottom-line in 1QCY19 has been down by over 80 percent, and apart from the inventory losses, six times increase in finance cost that typically consists of bank charges and mark-up on short term borrowings, also axed the earnings. However, 1QCY19 performance still stood better in front of its CY18 annual performance. Currency depreciation wreaked havoc on the bottom-line in 2018 as earnings were dragged down by staggering increase in exchange losses (part of the other expenses). In 1QCY19, there was a decline in other expenses that kept the earning from going into the negative zone. Back in 2018, Shell Pakistan ended up with a loss of over Rs1 billion versus a profit of Rs3.2 billion in CY17.

The OMC space has become tough not only because of fuel adjustment from furnace oil to RLNG, but also because of increasing competition. Smaller players have been pinching the market share from large players with their aggressive tactics particularly in the retail fuel space. Shell has also seen its market share decline over the last five years amidst rising competition. Though the company continues to be a strong lubricant player, its volumes for petroleum products have also seen a fall in the last 5 years. However, recently, the company has seen some recovery in volumetric growth with improvement in market share as well. However, these large players need to pick up to move ahead of the increasing competition.

Comments

Comments are closed.