There is a tariff petition filed by Tapal Energy to NEPRA to extend Power purchase agreement [PPA] of its Furnace Oil [FO] based 120 MW plant, under 1994 power policy, to KE network, by five years. The PPA is expiring in June 2019 and the petition is to extend it till June 2024. Someone should ask the company that in 22 years of operation they have earned on all the equity invested, why are they asking for 15 percent return on equity for another five years.

There is a supply glut coming in south and there is no rationale to extend the PPA by five years for a plant that is producing expensive energy. This space has repeatedly highlighted that there is case of excess capacity and the need is to novate some of the upcoming plants in NTDC system to KE to dilute the capacity charge per unit. For details read "Power[ful] scenarios", and "A case for higher power consumption".

This is the first PPA expiring, which is to be followed by Gul Ahmed plant in Nov 2019 and a few others including KAPCO in years to come. The case in hand is important as it is to set the precedence. Hence, it has to be kept straight for future referencing.

There is no way to extend the PPA on 'take or pay'; and even 'take and pay' does not make sense. It is beneficial for KE to buy from Tapal Energy even in case of 'take and pay', as the distribution company can use its existing network to keep on buying electricity. The fuel cost is a pass through item and the cost has to be borne by the consumers.

In case of transferring upcoming plants to KE, the company has to invest in network expansion, which would be good for the country- and consumers, but may not suit the distribution company. There are a number of new plants coming online in the south and the capacity charge of all these would be either paid by consumers, or become part of the growing circular debt.

One plant of 330 MW is under test run in Thar, and by this year end 660 MW will be added by two plants in Thar. Already a 1320 MW plant on imported coal is online at Port Qasim. Time is not far for first phase of China Hub power plant [660MW] to become operational. Apart from these, two nuclear plants of 2,200 MW will be online by 2021, and around same time, three plants each of 330MW will be functioning in Thar. Also, Lucky 660MW Port Qasim plant is in the process too. Not to mention that there is huge renewable potential in the South as well.

Phew, with all these capacities coming online amid the power consumption not increasing in proportionality, it is highly advisable to let go of the old expensive plants. The government is going to increase tariffs and that might result in dip in demand - the slowdown is already visible for Feb’19 consumption numbers - down by 4.2 percent. A few may economise consumption while others may move to solar.

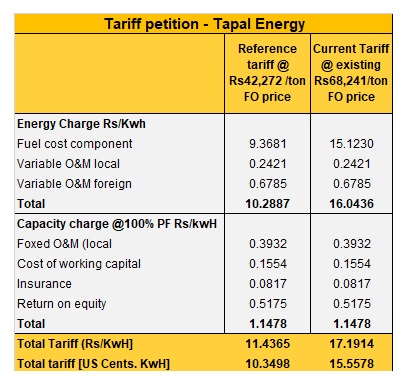

Hence, a big no to extending any PPA. And even the proposed tariff of the plant is wrongly computed in the tariff petition. Its misleading; they have used RFO base price at Rs42,282.71/Ton while the current price is Rs68,241/Ton. So the current fuel cost works out to be Rs15.2/KWh as against reference of Rs9.37. Total tariff likewise increases to Rs17.2/ KWh as against reference tariff of Rs11.44/KWh.

Comments

Comments are closed for this article.