Circular debt continues to be a headache for the IPPs, which exceeds Rs1 trillion now, as their receivables and payables continue to mount leading to higher bank borrowings and hence higher finance cost. The two largest IPPs, HUBC and KAPCO announced their financial result for 1HFY19 last week, and their finance costs continue to grow, showing the adverse effects of the circular debt menace.

Kot Addu Power Company Limited (PSX: KAPCO) touted a more than 100 percent increase in its earnings for 1HFY19 and even a more staggering increase in 2QFY19 profits. While its revenues grew moderately in 1HFY19 (despite a decline in 2QFY19) the increase in profitability came from weaker currency that inflated the ROE component and higher other income, slightly cut short by higher finance cost.

Recall that in 1QFY19, the company saw a significant jump in other income head, which according to the notes to the annual accounts, was due to the “true-up income” along with interest on late payment (penal income) from WAPDA. True-up income in 1QFY19 represented income resulting from change in US Dollar - PKR exchange rate exceeding the threshold defined in PPA, compared to the rates used for indexation calculation of relevant CPP invoices. And along with higher penal income in 2QFY19 as well, the other income depicted a growth of around 250 percent, year-on-year in 1HFY19.

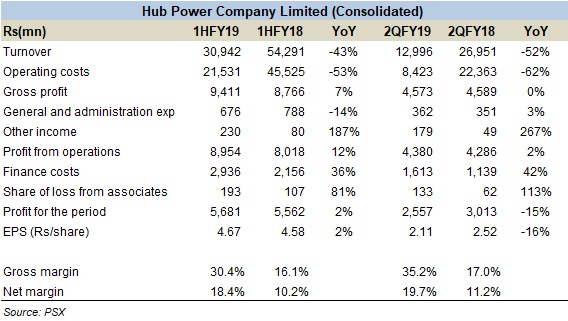

On the other hand, Hub Power Company Limited (PSX: HUBC) announced a decline in earnings for 2QFY19 and almost flat earnings for1HFY19. The IPP’s consolidated revenues dropped by 43 percent, year-on-year largely due to lower power dispatch to the NTDC system. Apart from the squeeze in the top-line, what dragged HUBC’s performance in 1HFY19 was growth in finance costs along with share of loss from associates.

Both IPPs show improvement in net margins. However, contrary to market expectations, none of them announced dividends. Where no dividend from KAPCO came as a surprise as the firm has been regular in paying out dividends, HUBC’s lack of dividend announcement is being pegged to its increase expansion plans and capital expenditure. Apart from the circular debt risk to the IPPs, which if cleared partially as the government mulls to clear Rs200 billion, KAPCO faces the additional risk of PPA renewal.

Comments

Comments are closed for this article.