Pakistan State Oil (PSO) threw a positive surprise last week, as it announced higher than expected payout, with its annual financial results for FY18. The final cash dividend of Rs5 per share was accompanied with a 20 percent bonus shares announcement. The dividend for the full year amounted to Rs15/share.

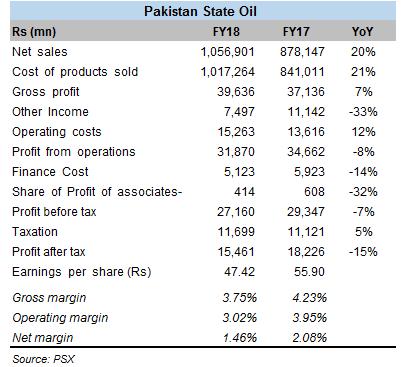

On the profitability end of things, the company’s pre-tax profits slid 7 percent year-on-year, despite stronger top-line growth. PSO’s revenue went up by a healthy rate, despite a 12 percent year-on-year drop in total volume sales. Recall that PSO’s handling of furnace oil has taken a sharp decline, as the country is making a gradual shift in terms of power generation mix from furnace oil to LNG and coal. The FO volume sales in FY18 dropped by a significant 31 percent year-on-year.

On the other hand, the growth in white oil sales, primarily motor gasoline continued healthy growth, showing a 10 percent year-on-year growth. The gross profit margins, however, were not as high as compared to last year. But the good thing is that lesser FO in the sales mix would eventually lead to better and cleaner financial for the company in the longer run.

The real drag on the bottom-line was caused by a sizable drop in other income, which came primarily on the back of reduction in contribution from PIBs in 2017. PSO would do well to curtail its operating expenses, which continued to grow at a brisk rate. Also, a higher tax incidence in excess of 40 percent led to the overall decrease in after-tax profits.

The receivables still remain a blot on the company’s balance sheet. PSO received some amount from the government in the later part of FY18 – but it would be much better if the issues are dealt with once and for all instead of injections every now and then just to keep things afloat. The reduced share of FO may become a blessing in disguise for the company, as the bulk of receivables stuck in the entire power sector chain are contributed on account of FO sales. Should prices remain stable, PSO stands to benefit from its improved sales mix.

Comments

Comments are closed.