Sunrays Textile Mills Limited

Sunrays Textile Mills Limited (PSX: SUTM) is part of the Indus Group of Companies. The formerwas established in 1987 as a public limited company under the Companies Ordinance, 1984. The company trades, manufactures and sells yarn. Its spinning mill is located in Dera Ghazi Khan, Punjab. In the previous year, the company purchased a piece of land in Kasur District.

Shareholding pattern

As at June 30, 2021, nearly 72 percent shares are with the directors, CEO, their spouses and minor children. Within this category, a major shareholder is Mr. Kashif Riaz, the CEO of the company. Over 21 percent shares are held under the category of “individuals” while the remaining roughly 7 percent shares are with the rest of the shareholder categories.

Historical operational performance

The company has largely seen a growing topline with the exception of FY15 and FY16, while profit margins have been following an upward trajectory.

In FY18, revenue increased by over 16 percent to reach close to Rs 5 billion in value terms. This was the biggest incline in revenue seen thus far. There was a significant growth in export sales that registered an increase of 57 percent. Local sales, on the other hand, reduced by more than half. The increase in exports was attributed to currency devaluation that made exports favourable. Additionally, an improvement in yarn prices also helped to raise profit margins as is reflected in a higher gross margin of nearly 13 percent, from last year’s 8.7 percent. Despite the escalation in finance expense owing to short term borrowings, net margin also increased year on year to reach 5.7 percent compared to last year’s 3.4 percent.

Revenue growth reached another high in FY19 as the company posted a growth of almost 23 percent. Topline reached Rs 6 billion in value terms. Again, this growth was largely contributed by export sales that grew by 25 percent while local sales registered a growth of 11.5 percent. With cost of production reducing to a little over 84 percent, gross margin further improved to 15.7 percent. This also trickled down to the bottomline that was recorded at the highest thus far of Rs 471 million with a net margin of 7.7 percent.

Most likely owing to the slowdown in business activity brought about by the Covid-19 pandemic, growth in the company’s topline was recorded at a relatively lower 6.4 percent in FY20.Local sales posted a growth of 81 percent, while export sales, although made the major contribution to revenue, increased by a marginal 2.3 percent. With cost of production increasing to almost 86 percent, gross margin declined to 14 percent. However, net margin continued to improve, to reach 8.6 percent and a net profit of Rs 560 million, on the back of unusually high other income coupled with a substantial reduction in finance expense. The latter was due to lower short-term borrowing.

In FY21, revenue increased by an all-time high of over 33 percent, with topline reaching Rs 8.6 billion in value terms. Export sales grew by 38 percent, while local sales registered a growth of 43 percent. This was attributed to a resumption in trade and business activities as lockdowns eased. Additionally, the US-China trade war and dire Covid-19 situation in neighbouring countries redirected global yarn demand to Pakistan.With cost of production falling to near 82 percent, gross margin reached an eight-year high of over 18 percent. With little changes in other factors as a share in revenue, this also trickled to the bottomline that was posted at an all-time high of over Rs 1 billion while net margin also reached a peak of 13.3 percent.

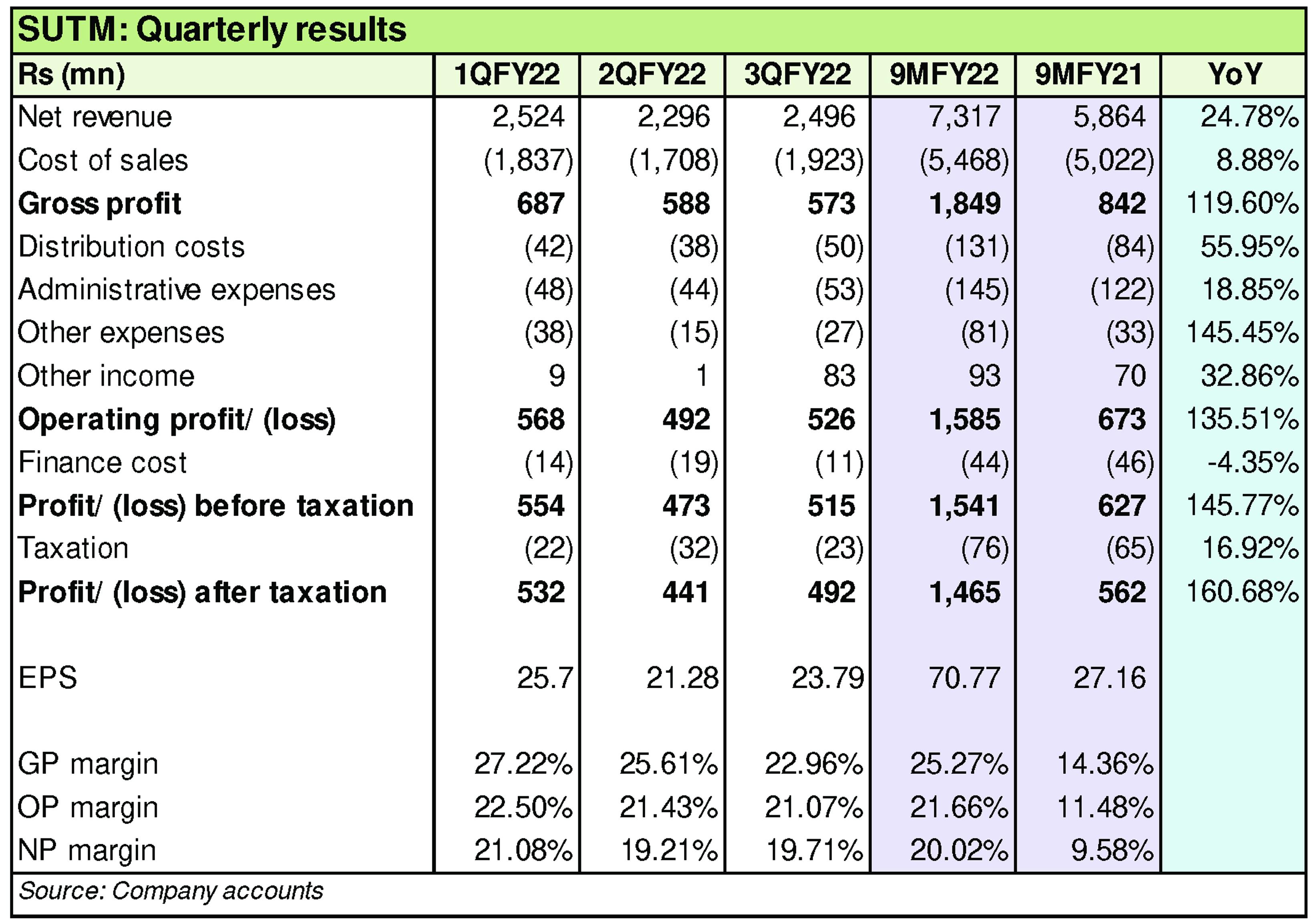

Quarterly results and outlook

Revenue in the first quarter of FY22 was higher by over 55 percent year on year. This was attributed to an increase in demand, followed by an increase in yarn prices. In addition, the company also procured raw material that helped improve profit margins as gross margin in 1QFY22 was higher at 27 percent compared to 6.5 percent in the same period last year. This also trickled to the bottomline. Net margin was also notably better at 21 percent versus 3.4 percent in 1QFY21.

The second quarter also saw higher revenue year on year, by nearly 17 percent. This was again attributed to an improvement in prices. Additionally, demand has also been strong since business activities normalized a year after the pandemic. Cost of production has also been significantly better at 74 percent of revenue, compared to nearly 87 percent in 2QFY21. As a result, profit margins were better year on year at 19.2 percent versus 9.8 percent in 2QFY21.

In the third quarter too, topline was higher, albeit by 9.7 percent year on year. Cost of production was only marginally better at 77 percent compared to 79 percent of revenue. Therefore, net margin was also only marginally better, relative to improvement seen in the previous two quarters, at 19.7 percent compared to 14.5 percent in 3QFY21. While the grave Covid-19 situation in neighbouring countries have worked in the benefit of Pakistan’s textile industry, the fluctuations in exchange rate and increases in price of inputs keep future profitability uncertain for the company.

Comments

Comments are closed.