Archroma Pakistan Limited (PSX: ARPL) is a limited liability company and a subsidiary of Archroma Textiles GmbH. The latter is headquartered in Switzerland. The company manufactures, imports, and sells chemicals, dyestuffs and coating, adhesive and sealants.

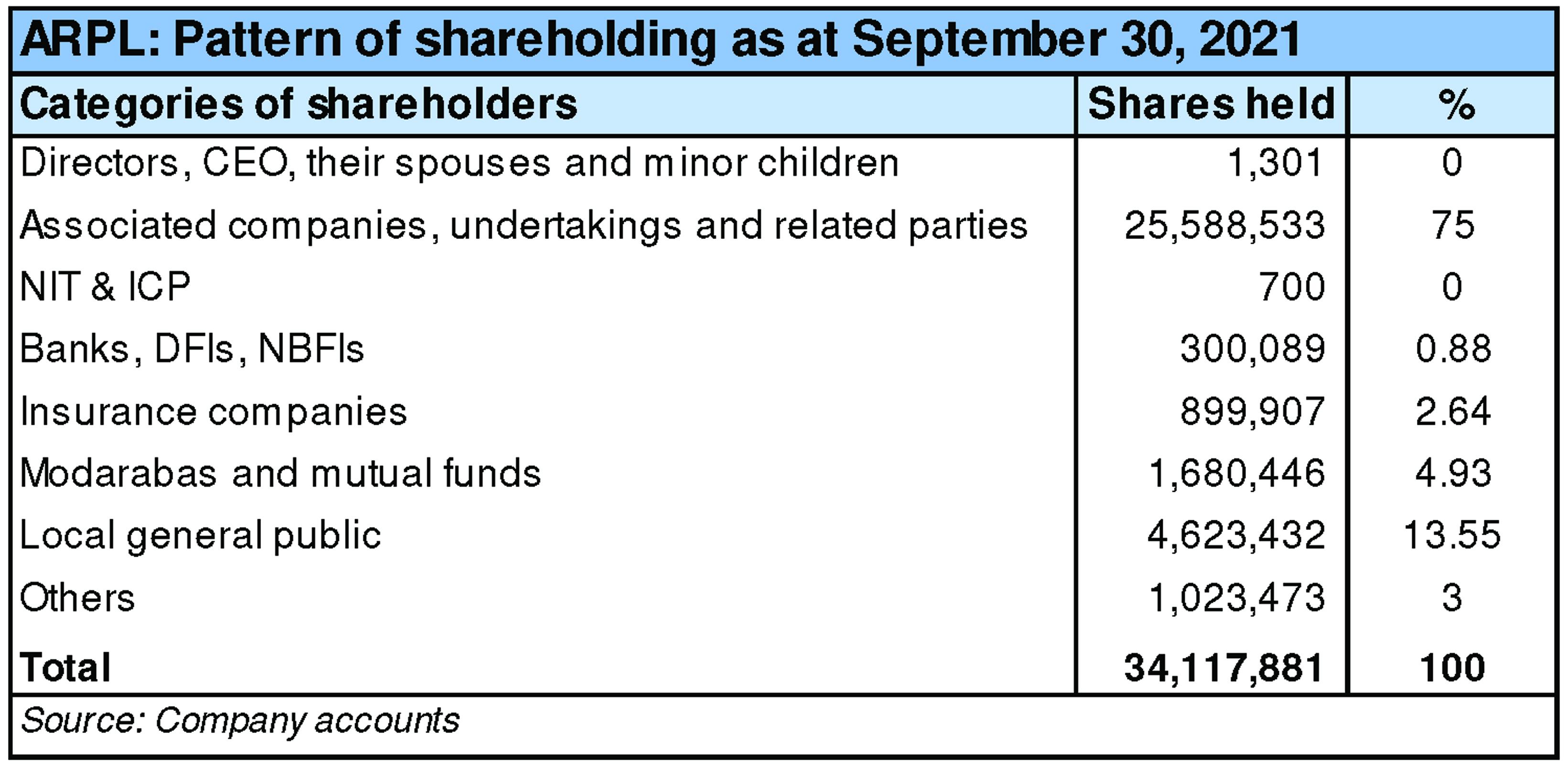

Shareholding pattern

As at September 30, 2021, 75 percent shares were held by the associated companies, undertakings and related parties. This solely includes Archroma Textiles GmbH. The local general public holds over 13 percent shares, followed by almost 5 percent shares in modarabas and mutual funds. The directors, CEO, their spouses and minor children hold a negligible share whereas the remaining about 6 percent shares is with the rest of the shareholder categories.

Historical operational performance

Archroma Pakistan has mostly seen a growing topline, while profit margins in the last six years have followed a gradual decline before improving slightly in MY21.

In MY17, revenue grew by nearly 8 percent, unlike the double-digit growths seen in the last two years. Topline crossed Rs 12 billion in value terms. Export sales posted a growth of 49 percent while the textile division remained the major contributor to the total revenue. Cost of production, on the other hand, increased marginally to 68.4 percent, compared to over 67 percent in MY16. However, the decrease in operating margin, and hence net margin was relatively more pronounced as administrative expense consumed a larger share in revenue. This was due to salaries expense and outside service charges. Thus, net margin was recorded at a lower 13.2 percent.

The company was back to its double-digit revenue growth in MY18 as it was higher by 16.7 percent. Export sales continued to post exorbitant growth rates as it grew by more than 50 percent, while brand performance and textile division remained the major contributors to revenue. Cost of production remained stable at around 68 percent, keeping gross margin also flat at 31.6 percent. However, due to royalty charges, distribution expense inclined as a percentage of revenue. Coupled with a rise in finance expense due to exchange loss and high short-term running finances, net margin fell to 10.7 percent.

The company maintained its growth momentum in MY19 as revenue posted a growth of 21.4 percent. Export sales alone reached Rs 4 billion, whereas brand and performance textile specialties dominated the total revenue. Cost of production increased to 69 percent, reducing gross margin marginally to 30.8 percent. This also trickled down to the operating margin as operating expenses remained more or less similar as a share in revenue. However, net margin reduced to 9.9 percent due to a rise in finance expense as well as impairment loss on trade debts that stood at Rs 143 million for the year compared to Rs 60 million in the previous year.

After witnessing a rising revenue for five consecutive years, revenue in MY20 contracted by over 13 percent. This was due to a decrease in local sales of “others” category that is not the core business activities of the company. Moreover, export sales of the brand and performance textile specialties division also reduced significantly which could not be offset by the increase in local sales of the same. On the other hand, cost of production increased to a nine-year high of 72 percent that reduced gross margin to nearly 28 percent. Moreover, the administrative expense increased due to salaries expense, legal and professional charges, that reduced profitability further. Net margin was recorded at 7.8 percent for the year.

Recent results and future outlook

The company witnessed the biggest increase in revenue in MY21 as it grew by over 32 percent, nearing Rs 20 billion in value terms. This was attributed to the growth in the business of brand and performance textile specialties and coating adhesive and sealants by 33 percent and 41 percent respectively. This resulted in an improvement in the gross margin for the year that was recorded at 31 percent. With better cash generation and hence lower finance expense along with a decrease in operating expenses as a share in revenue, the improvement in profitability trickled down to the bottomline. It was recorded at an all-time high of Rs 2.31 billion, and a net margin of 11.6 percent.

While demand has recovered considerably nearly two years into the Covid-19 pandemic, there are other challenges that continue to persist. There are issues with supply chains that have resulted in delays in raw material supplies. This in turn, has resulted in an increase in costs and lead times. There is also a shortage of containers and vessels.

The country’s textile industry has seen an improvement in its exports, particularly in the value-added sector. News suggests that this has been on the back of easing of lockdowns in North America and European countries that are prime export destinations. The demand is expected to continue, not only for home textiles but also for denim and casual wear.

Comments

Comments are closed.