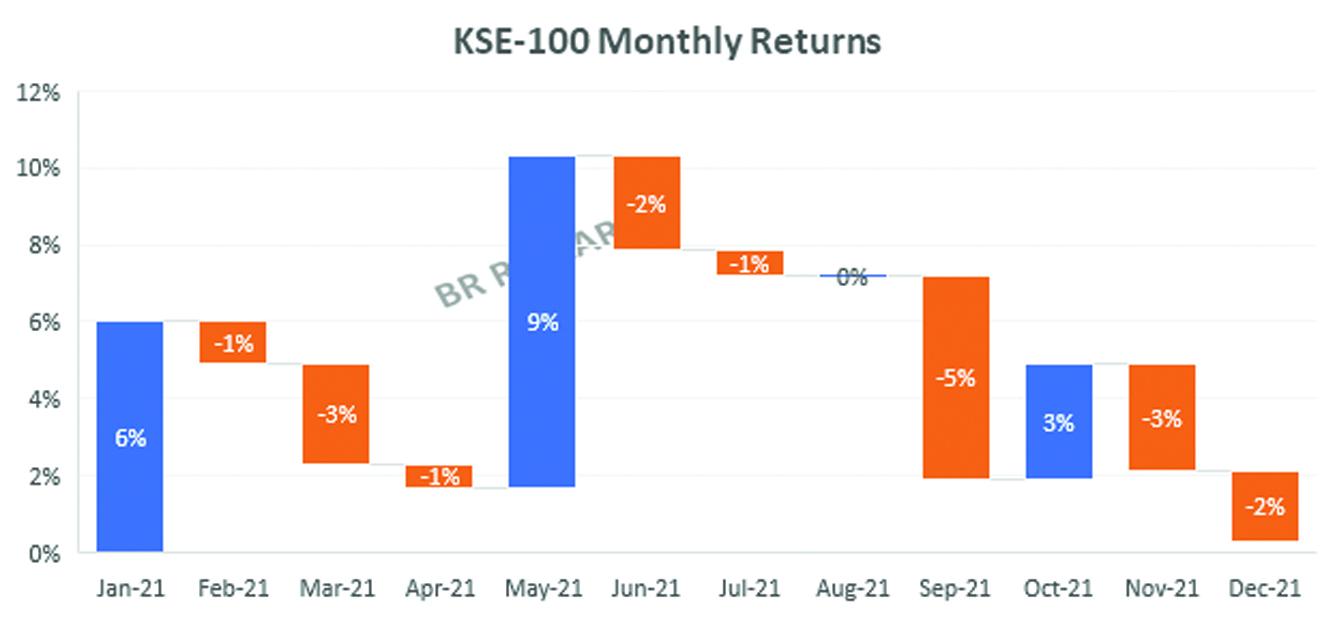

Barring an exceptional spell in the last 12 trading sessions of 2021, the benchmark KSE-100 index at the Pakistan Stock Exchange is all set to end the year, where it started. The strategy reports at the beginning of every calendar year would tell otherwise, but the sell-side bullish bias is well known. Expect another round of strategy reports come 2022, selling the dream of a double-digit return, as the valuations are mouth-watering. Not that they are ever not mouth-watering.

Every single time the KSE-100 index tried to break free, there were months of bearish spells offsetting all the increase, bringing it back to square one. Will 2022 be any different? If one goes by crude numbers, there is every reason for the stock market to wake up from the slumbers. The earnings multiples are the juiciest in a long time, even if there are no takers amongst foreign investors. The big ticket listed companies have raked in quarter after quarter of all-time high earnings. Covid fears are by and large priced in. Regional situation did not pan out as bad as was earlier feared. Local political scene keeps throwing a surprise here or there, without necessarily having the ammunition to topple the system.

All these variables merely become a sidenote, when it comes to the PSX, as the index movement follows one variable that is the 10-year PIB yield, more religiously than any other. Save for the peak Covid days, the trend has stood the test of times, behaving predictably every single time, since time immemorial. The central bank’s monetary policy decisions reversing the accommodative policy stance, is what best explains the bear trend at the PSX.

Just a day after 100 basis points increase in policy rate, the stock market reacted positively. Could this be the beginning of a trend or just a relief rally, is best left to time. There is a perception that the market had overreacted in getting the yield too steep and the signaling by the MPC should cool down the yields. But with the inflation expectations revised upwards, the end goal of “mildly positive” real interest rates may still warrant a rate hike here or there, albeit, not as significant.

Comments

Comments are closed.