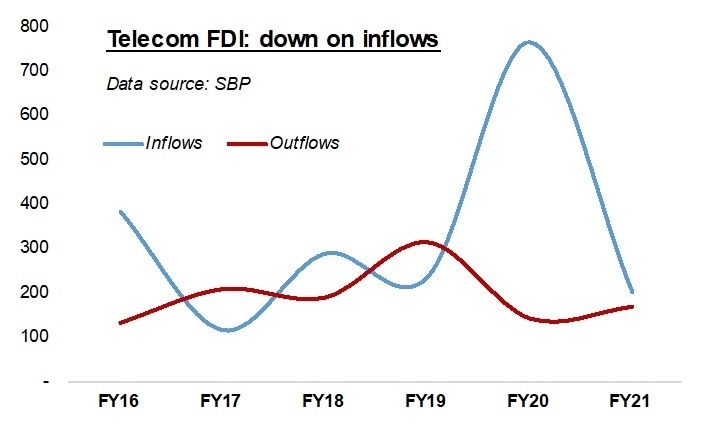

The telecom sector’s contribution to the country’s foreign direct investment (FDI) scorecard has plummeted sharply. The latest central bank data show that the net FDI for the telecom sector came in at $35 million for the entire FY21, down by a whopping 94 percent compared to the previous year. Much-reduced inflows and rising outflows have delivered a double blow to the sector’s investment profile.

Lower inflows were expected as the government couldn’t hold the spectrum auction on time, but the final tally is rather abysmal. As a result, the telecom sector FDI accounted for mere 2 percent of the country’s overall FDI in FY21, significantly lower than its 24 percent share in the pie in the previous fiscal. The FY20 telecom FDI had benefitted from the windfall due to partial payments from cellular license renewals.

Data from the SBP show that the sector’s gross inflows at $202 million – down by nearly three-quarters compared to FY20 – were at a multi-year low. Other economic sectors actually did better overall, as non-telecom-related gross FDI inflows had increased by 10 percent year-on-year. To make it worse, telecom sector’s FDI outflows increased by nearly a fifth to reach $168 million during the just-concluded fiscal. However, this exodus is lower than the 70 percent jump in outflows for non-telecom sectors as a whole.

For FY22 to be any different, the onus is on the government to hold the stalled spectrum auction in the coming months. Background discussions indicate that while the PTA had done its homework to conclude the auction within the confines of FY21, it was the ministerial changes at the finance ministry that contributed to the delay in spectrum auction that was to bring in revenues valued at $900 million+.

Partial, 50 percent proceeds from the said auction can land somewhere close to half a billion dollars in spectrum fees, a part of which is expected to come in the form of FDI from operators’ foreign principals. The FY22 budgetary documents show that the federal treasury is expecting Rs45 billion as “income from PTA”, which is a 32 percent increase over the Rs34 billion under revised estimate for FY21. Most of this money is to be collected under the head of license-renewal payments from Telenor, Zong and Jazz.

Be that as it may, simply counting on operators’ acquisition (and renewal) of spectrum to boost investment numbers is not an ideal tactic. For one, such an exercise is occasional in nature, hence the crests and troughs in telecom FDI numbers. Besides, operators complain about government fixation on raising high amount of revenues from spectrum auctions instead of following a predictable auction calendar that is sensitive to the needs of market development.

As highlighted in this space before, the opportunity to mobilize additional, perhaps much higher, foreign investment can materialize if the government and operators paid serious, sustained attention to the need to expand affordable broadband access to un-served and under-served regions of Pakistan. This would include rolling out fiber-optic networks on a massive scale, along with associated physical infrastructure. For that, the government needs to incentivize the market and the operators need to play the long game.

Comments

Comments are closed.