Zahidjee Textile Mills Limited (PSX: ZAHID) was set up in 1990 as a public limited company under the Companies Ordinance, 1984. Its primary business is to export value-added fabrics and textile made-ups. It also manufactures and sells yarn.

Its spinning division has two units in Faisalabad and weaving division has one unit, also located in Faisalabad.

Shareholding pattern

As at June 30, 2020, nearly 96 percent shares of the company are owned by the directors, CEO, their spouses and minor children. Within this, over 83 percent shares are held by Mr. Muhammad Zahid, the CEO of the company. The local general public owns 3 percent shares followed by 1 percent held in joint stock companies.

Historical operational performance

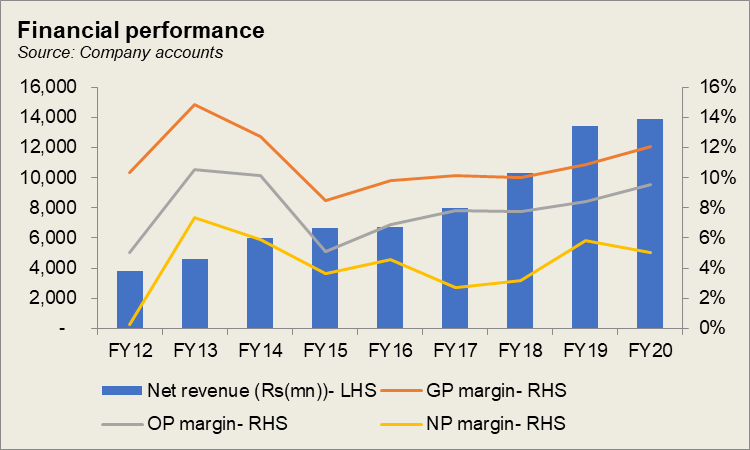

Zahidjee Textile Mills has seen a growing topline consecutively since FY12. Profit margins, on the other hand, dipped in FY15, and slowly increased until FY20.

During FY17, the company witnessed an almost 19 percent growth in its revenue. This mostly came from increase in revenue from local sales that grew by nearly 31 percent, while exports fell by almost 10 percent. The rise in local sales was attributed to a rise in production. This, in turn, was a result of installation of 8,400 additional spindle. Exports of the country have been uncompetitive in the international market, especially with stiff competition from regional peers. There was a very marginal decline in cost of production as a share in revenue, therefore gross margin was also more or less flat at 10 percent. Despite this, net margin decreased year on year to 2.7 percent, due to an escalation in “deferred tax liability due to addition in plant and machinery”.

FY18 saw revenue growing at over 29 percent. Both export and local sales witnessed a rise, by 14.4 percent and 32.7 percent respectively. This was attributed to increased production as a result of capacity expansion; the company installed 17,472 additional spindles during the year. Cost of production, on the other hand, continued to hover around 89 percent of revenue, again keeping gross margin flat at 10 percent. With a slight decrease in finance expense as a share in revenue and an additional Rs 13 million coming in through trading profit, net margin rose marginally to 3 percent.

The company saw one of the highest growth rates in revenue at over 30 percent in FY19. Both export sales and local sales registered an increase by nearly 16 percent and almost 35 percent, respectively. The currency devaluation during the year made exports somewhat competitive as is reflected in the higher export revenue for the year. Cost of production reduced very marginally, allowing gross margin to near 11 percent for the year. The continuous decline in administrative and distribution expenses as a share in revenue also led to some improvement in profitability. Although finance expense inclined due to higher interest rates, to make up almost 3 percent of revenue, net margin increased on the back of lower expenses and a positive tax figure at Rs 37 million, compared to a tax expense of Rs 249 million in the preceding year.

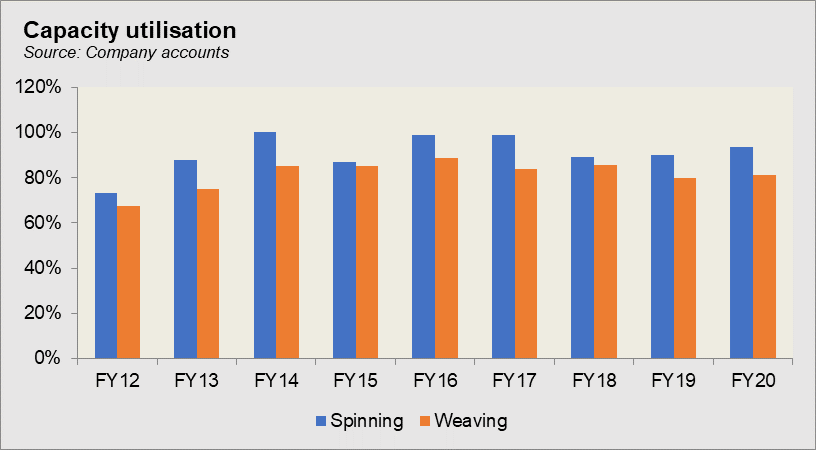

The effect of an economic slowdown at the start of FY20 and the Covid-19 pandemic towards the end of FY20, is reflected in the single-digit growth rate of revenue of the company. At 3.4 percent, it is the lowest growth rate in revenue the company has witnessed since FY17. Most of the rise in revenue was brought in through export sales, while local sales decreased very slightly, by less than 1 percent. The currency devaluation had made the otherwise uncompetitive products, competitive in the international market. In addition, demand for Pakistan’s textile has remained and grown as is reflected in the above 80 percent capacity utilization for the last seven years. Cost of production went down slightly, to 88 percent of revenue, allowing gross margin to reach a high 12 percent. But the higher tax expense kept net margin close to 5 percent for the year.

Quarterly results and future outlook

The first quarter of FY21 saw revenue higher by 4.5 percent year on year. However, cost was significantly higher in the current period; profitability was affected despite the greater contribution by other income due to “execution of customers’ sales contracts which were signed off during the Covid-19 pandemic lock down period, at rates lower than the current market rates”. The second quarter saw lower revenue compared to 1QFY21, but higher year on year by 3 percent. This was attributed to a volumetric gain. With an additional Rs 38 million coming through other income, profit margins were better than the previous quarter, as well as year on year.

The third quarter saw a notable improvement in topline, both compared to previous quarter and year on year. This was attributed to “an opportunity to quote competitive prices”. Along with also offering a good quality product. Cumulatively too, the nine months of FY21 saw a 6 percent higher revenue than 9MFY20. Costs were also lower; therefore, profitability was also higher. With timely raw material procurement, and better prices, the company can end the year profitably.

Comments

Comments are closed.