Pakistan rupee averaged the lowest since July 2019 in the first fortnight of April 2021. Much improved currency made matters easier for the government to lower the petroleum prices. Benchmark Arab Gulf crude oil averaged $70/bbl for the reference period, higher by 1.6 percent, which was offset by a similar increase in the rupee value over the greenback – allowing the government to lower the prices further, without having to adjust taxes further downward.

This was one of the very rare occasions where petroleum product prices were lowered despite increase in reference crude oil prices. Previously, the government had maintained the practice of maintaining the prices b adjusting levies or passing it on. These are clear enough signs that inflation concerns are greater today than they ever were and chasing lofty Petroleum Levy target is no more in the scheme of things.

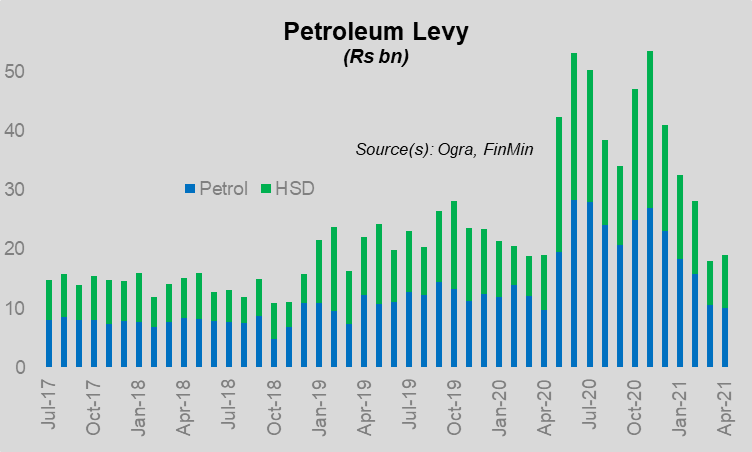

Recall that the PL collection was on song till 1HFY20, as the government had pocketed 60 percent of the rather aggressive annual target of Rs450 billion. Growing inflation concerns have since, slowed down the PL collection, which was the lowest last month, and by the look of things, the pace will remain slow in the remaining four revisions of the fiscal year.

In all likelihood, the annual PL target will be missed by Rs40-50 billion, which is not a huge concern, especially looking at the optimistic nature of the target when it was announced. Much will depend on the consumption pattern, which may face challenges in the short-term given the pandemic situation worsening by the day.

It is therefore, rather surprising that the authorities have committed Rs511 billion in lieu of PL collection for FY20. There is no way the government is even going to get anywhere close to that, which is why doubts have been raised over the seriousness of the government’s commitment to the IMF, in matters other than petroleum.

Every day that passed by is another day closer to the next general elections, and that is where the rather absurd PL collection target of Rs607 billion for FY22, makes even lesser sense. For that to happen, the PL will consistently have to be maxed out at Rs30/ltr for both the key products, also hoping that the demand increases by 10 percent year-on-year. All this while the aim is to curb inflationary pressures. It just does not add up.

Comments

Comments are closed.