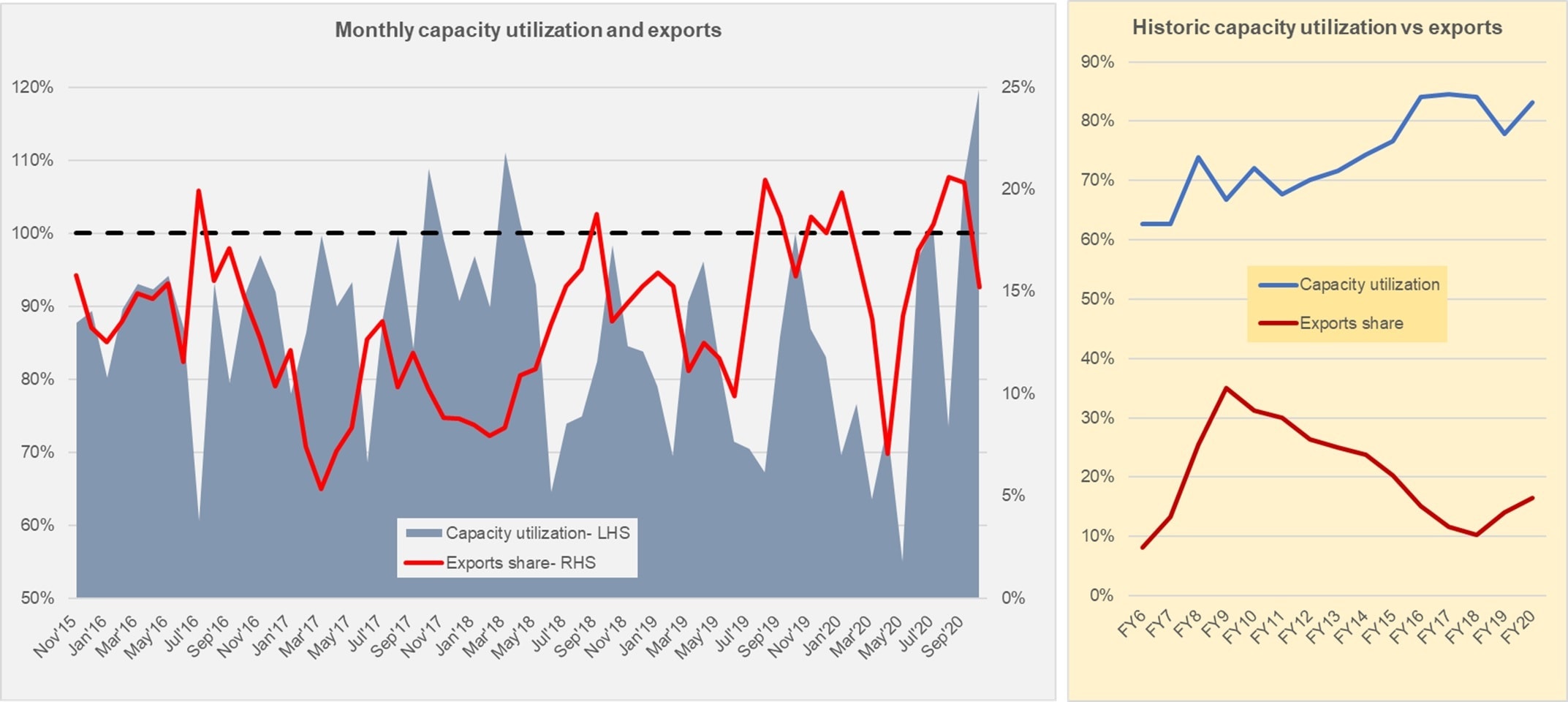

That the cement industry is returning to its former glory days is very apparent—in Oct-20, the industry dispatched nearly 6 million tons of cement—the highest ever in history--selling 120 percent of its existing capacity. Demand is bolstered by strong domestic factors (read more: “Cement’s second coming”, Dec 2, 2020) that will keep pushing the limits over the next few years. At this point, two things are clear: the industry has to go into another expansion phase and exports’ share in total dispatches is scheduled to wane.

The latter is probably despite the South African market opening up to Pakistani cement once again over the next ten days after the lifting of the five-year anti-dumping duty on Pakistani cement manufacturers. Though, exports share has grown since last year, the pace of domestic demand is outstripping and reducing the need to sell cement abroad. Exports may very well become an added bonus for cement makers, rather than a reliable and hefty source of revenue. After all, cement manufacturers get substantially better pricing locally than abroad and will likely incur lower distribution expenditures if the path back to domestic market is cleared out.

Notice, historically, as capacity utilization for the industry grew—which meant demand in the country was booming—exports share began to fall. This is because cement makers are naturally tuned to cater to local demand, using exports as a way to diversify markets and access when domestic demand is not meeting expectations.

That is not to say, exports won’t grow. All signs indicate exports will continue to grow in terms of volume—companies in the south that are at the moment exporting clinker to some markets will shift back their focus onto exporting better-priced cement to South Africa while Afghanistan and other neighboring countries will keep providing constant avenues. But the share will likely drop as local markets dominate the sales mix. Already, data shows, exports share fell to 15 percent—from 20 percent the previous month—when capacity utilization reached 120 percent in the month of October.

The second important development in the industry would be more expansions. Demand patterns suggest, or rather necessitate, capacity growth which can come in the form of new greenfield or brownfield plants or simply by improving existing plant efficiencies. This is a good time for companies to go into expansion from the perspective of cost of debt—interest rates are pretty low which would make cost of financing new facilities and machinery fairly cheaper.

So far, Kohat cement has already announced expansion plans that would include a new production line, a cement mill and a coal-fired boiler that would generate electricity and reduce power costs. DG Khan cement is also contemplating an addition to existing capacity and may add a new production line after evaluation. Maple Leaf has a waste-heat recovery project in the works. But other companies are only a step or two away from similar announcements—probably being more vigilant than the last wave of expansion and spending more time assessing the situation. Demand did not jump as much as it was expected post the 2016 expansion era which led to companies going into losses with debt piling up.

But any risk assessment should take into consideration the possibility of higher imports to meet mounting demand which would tilt favors away from domestic manufacturers in terms of market share. With the way the government has latched onto the construction sector though, the industry does not really have to be a real daredevil to enter expansions—it simply makes more economic sense.

Comments

Comments are closed for this article.