There are plans in the making to shift the transport sector’s gas usage from domestic natural gas to privately imported LNG. The relevant associations have lauded the government’s idea. The idea is to free up more volume for high priority areas. Top on the priority list sits the domestic sector. Now, you can debate whether domestic sector should continue to be prioritized over other users, especially when it continues to be heavily cross subsidized. But that is not changing anytime soon.

So CNG will have to go in winters for starters. And then likely forever be shifted to privately imported LNG for the foreseeable future. You can’t argue with the plan. Experts have long advocated freeing the pipeline gas from transportation use, citing it as the most inefficient use. Inefficient it may well be, but before the leap is taken to a CNG-free natural gas consumption pie – measures will have to be taken to ensure the distribution companies sail smooth in terms of financials.

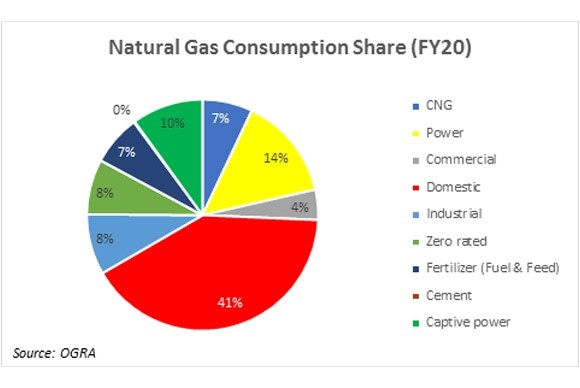

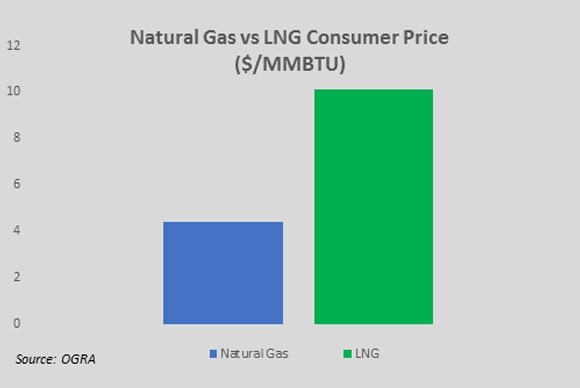

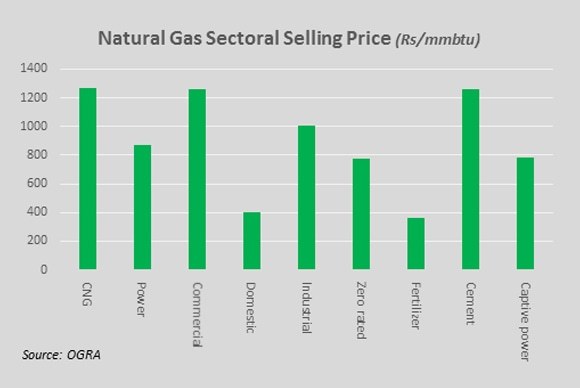

CNG makes just 7 percent of the total domestically produced gas consumption pie. So, letting go of that should not be a big problem, one would assume. But it has a higher share in revenues than even non zero-rated industrial sector. Recall that natural gas in Pakistan is priced using cross subsidies. CNG at Rs1260 per MMBTU is priced 83 percent higher than the average selling price of Rs692/MMBTU. It is nearly three times pricier than domestic gas – which averaged Rs387/MMBTU for FY20.

Assuming the freed gas would then be diverted to domestic consumption, you are staring at a Rs40 billion-dollar gap, in the estimated revenues of the two gas distribution companies. One could argue that the domestic prices could be increased to cover up for the potential CNG volume loss. Bear in mind that domestic average prices have already been jacked up by 100 percent in two years. While domestic average price continues to be significantly cheaper than the weighted average price – it would be unwise to put the domestic consumers in front of another massive hike.

Had gas prices continued to be gradually rationalized over time, things would be much different today. A gradual 15-20 percent annual increase spread over time is less painful than two rounds of 50 and 60 percent back to back. This has now limited the ability to tinker with domestic gas prices for at least another year if not more.

What else could go up? At a time when the government is providing incentives on incremental electricity consumption to industries, it is hard to believe gas tariffs for industries could be increased to cover up CNG. There are talks of reducing gas supply to captive power plants and instead encourage national grid consumption. And rightly so too. Only that this would also free up another 10 percent volume that contributes 12 percent to revenues.

What are the options left? Could there be a case of penalizing incremental domestic consumption? This could well make a case to discourage wastage of the scarce precious resource which goes to the most inefficient usage for domestic heating purposes. The argument that the demand for natural gas may not be there beyond current rates, still needs to be put to test. The delta between domestically produced and imported gas is a massive one, and the sooner Pakistan adopts a weighted average pricing mechanism, the better it will be. There is also the need of fair demand assessment by the authorities.

Gas shortage numbers in excess of 2 billion cubic feet per day keep making the rounds – but given how little the needle has moved in terms of consumption after LNG was made widely available shows the demand may be overestimated. Demand assessment, creating more use cases, and weighted average price should now be subjects of debate. Boring as they may sound, that is where the meat is. Or else, keep going circles about LNG spot and how many million dollars were “lost” because bookings were delayed.

Comments

Comments are closed.