As the sugar inquiry report makes sensational headlines for its not-so-shocking revelations, the performance of the lesser half of the industry has gone unnoticed. These are the 28 listed units, which together account for at least half of the sector’s total output. A pre-ponderance of these firms are located in Sindh, whose beneficial ownership is usually not attributed to politically exposed persons.

Although semi-annual financials (ending 31-March) for the sector are now long overdue, dominant players from Punjab and KP have filed for an extension in deadline. That could be for variety of reasons; from operational delays stemming from lockdown, to the launch of forensic inquiry by FIA at the premises of these units which may have delayed their reporting. Whatever the explanation, all listed units from Sindh operational during the ongoing season have now announced their six-month accounts (barring one), thus making a detailed commentary on their performance possible.

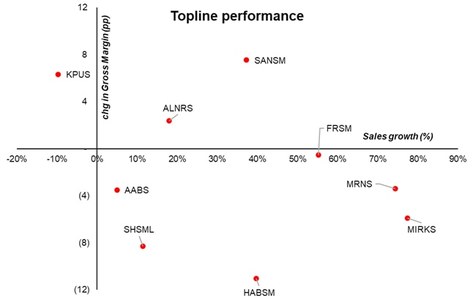

And quite a surprise do they offer. Although an uptick in industry’s performance was anticipated given the substantial increase in average retail price of sugar compared to the previous year, it was expected to be partially offset by plummeting exports from the province. Instead, mills managed to pull off a monumental rebound in revenue, with at least two units recording a topline jump of over 75 percent.

This is why the performance scorecard is so revealing. A turnaround in profitability did not accompany the jump in topline performance, as gross margin saw industrywide erosion. Average gross margin, albeit a crude measure, declined by seven percentage points from 13 percent to six percent. For two units that recorded a positive movement in GPM compared to last year, it was only a climb out of negative territory.

The reasoning requires some explanation. Mills in the province claim that due to shortage of raw material sugarcane during the ongoing season, mills had to procure cane at exorbitant rates from growers, with gross profit margin taking the brunt. That is understandable, except that the industry association claimed to have carryover inventory for at least three months at the beginning of marketing year in October. It should be clarified whether sales made from carryover inventory have been recorded at last year’s production cost or at current season’s cane procurement rate.

Add to this the compounding effect of inflationary pressures, and it is little surprise then that the operating performance took a depressive turn for most firms. Out of 11 units from Sindh whose 6M financials are now available, four reported an operating loss whereas four others saw profitability take a dip by average 40 percent year-on-year.

Beyond this, bottomline for most firms had nowhere else to go but south. Because discount rate was still at its peak of over 13 percent during the reported period (Oct-Mar), finance cost for almost all units saw an upward spiral. Before-tax position thus received substantial battering, with loss for six out of 11 companies, while only two reported what could be termed notable improvement in profitability.

Barring the doubts raised by the inquiry commission on the integrity of sugar industry’s financial reporting, the sector appears to have witnessed a tough year so far due to increased inflationary pressure (upto Mar-20), rebound in raw material prices, and expense under working capital financing head. If that’s industry’s predicament in a year when commodity prices surged ahead by over one-third, the picture may turn far uglier in upcoming period if demand declines due to Covid-19 related pressure on discretionary spending.

Comments

Comments are closed.