Shams Textile Mills Limited (PSX: STML) was established in 1968. It is a public limited company incorporated under the Companies Act, 1913, (now Companies Act, 2017).

The company manufactures, sells and trades yarn and cloth. It produces various kinds of yarn that finds its utility in denim, woven fabric and knit wear.

It established its first plant in Chiniot for spinning, weaving, dyeing and finishing. It added to its capacity by setting up another plant- spinning unit at Sheikhupura Road. Its last addition to capacity was establishing a third specialized unit which started commercial production in 2006.

Shareholding pattern

As of June 30, 2019, close to 34 percent of the shareholding is with the associated companies, undertaking and related parties. Of this around 20 percent is with Crescent Powertec Limited. While 27 percent is distributed with the local general public, directors, CEO, their spouses and minor children own about 24 percent of the shares. Mr. Khalid Bashir, the CEO of the company has a little more than 10 percent of the shares. NIT & ICP has just over 12 percent which solely includes CDC- Trustee National Investment (Unit) Trust. The rest of the 3 percent is distributed with the remaining of the categories.

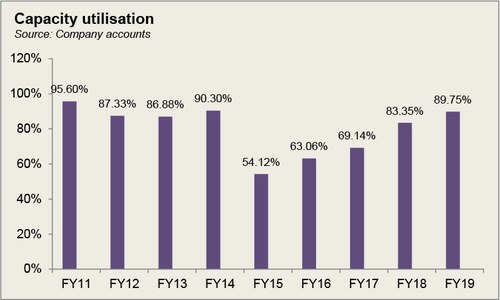

Historical operational performance

Shams Textiles’ revenue and profit margins have been rather inconsistent, as the former grows and decreases at varying rates while the latter reached its lowest in FY16, before improving again, only to decrease again three years later, in FY19.

During FY15, the company experienced a negative growth in its topline- close to 4 percent; although it was lower than last year’s double digit negative growth of 13 percent. The reason for decline of sales is attributed to lower demand from one of their major export markets. The breakdown of sales shows that export sales have increased while local sales have seen a decline. Costs on the other side only a saw a slight decline, although it made a considerable 96 percent of the revenue; this left little room for other costs to be absorbed. Cost of manufacturing was largely dominated by cost of raw materials, making up 67 percent of the total cost of manufacturing. So while the company did incur a loss, it was lower than that in FY14.

Topline further decreased in FY16, this time a notable slump by 29 percent. This was again attributed to a slowdown in demand from one of its major export market. In addition, cost went up exorbitantly to consume 98 percent of the revenue. The burden of energy prices is to be blamed here. Fuel and power are the next biggest cost element of cost of manufacturing, raw material cost being the first. According to an excerpt from the Pakistan Textile Journal, 2016, “apart from the woven apparel sector, all sectors showed a decline or at best, stagnating textile exports in 2015-16”. It further goes on to state that Pakistan had been increasingly reliant on China for more than 85 percent of its exports. With a decline in demand from China, the country did not have much to rely on. In this scenario, an increase in loss for textile companies was inevitable as was the case with Shams Textile.

Some recovery was seen in FY17 as topline registered a positive double digit growth of 18 percent. However, this was mostly brought in by local sales, while export sales contracted to Rs671 million from the previous year’s Rs 1 billion. Despite having one of the best technologies and machineries in the region, Pakistan was unable to reap the benefit as energy cost crippled its ability to manufacture at a cost that allows for a competitive price in the international market. Moreover, since the cotton crop of the country could also not fulfill its industry demand, it had to be imported which further added to costs; the latter consumed 96 percent of the revenue. Although lower from last year, it was still high. The higher topline trickled down its effect as the loss incurred halved from that in FY16.

In FY18 the company saw a further incline in their revenue as it grew by 41 percent. Both, exports and local sales saw an increase; local sales in FY18 were the highest seen thus far. During FY17, with the consistent BMR activities, the company was expecting better figures in the future, as is evident from the improvement in FY18. There was a further reduction in costs, as a percentage of revenue, which helped margins grow, and the company managed to post a positive bottomline after four consecutive periods of losses.

The company entered a third year of positively growing revenues- nearly 13 percent in FY19. Exports reduced notably by 28 percent while local sales, owing to a growing middle class continued to grow for the fourth year in a row. The devalued currency, which by economic principles could have made exports competitive, did not fetch higher export sales since high cost of production still kept price uncompetitive as compared to regional peers such as India. With costs consuming more than 95 percent of the revenue, bottomline declined to Rs 43 million.

Quarterly results and future outlook

While revenue improved year on year during 9MFY20, there was no change in costs as percentage of revenue with the former still consuming 96 percent of the topline. Although gross margins improved, the same effect could not be reflected in the bottomline as operating costs increased by 50 percent while some support was also brought in by other income during 9MFY19, which was absent in 9MFY20. Eventually the company posted a loss for the period. With the current scenario of Covid-19 and a halt in business activities at home and abroad alike, it is likely that FY20 will end with negative figures for Shams Textiles.

Comments

Comments are closed.