Power generation in March 2019 went down by 12 percent year-on-year to 7.4 billion units – the biggest year-on-year decline in recallable memory. The demand slowdown has been ever so evident as, as the net power generation has decreased for the fourth straight month, in comparison to the previous year. The power generation in March 2019 stood at levels seen in March of two years ago. The economic slowdown is real – and is not going anywhere, anytime soon.

The power generation dependable capacity has increased by 22 percent year-on-year from same period last year to 30,590 MW. The generation is down in double digits – which essentially means more capacity payments been made regardless of power generation, in most cases where plant have shown availability.

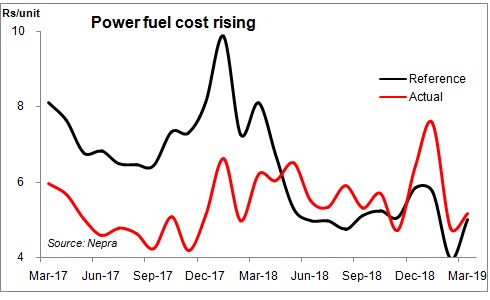

The average fuel cost has also gone dearer, which thankfully, is a pass through item, but can still be a drag on recoveries and contributes to the mounting circular debt.

The fuel cost component for March 2019 was Re0.16/unit higher than the reference cost of Rs5/unit – making an impact of just over a billion rupees for the month. This, in comparison to the same period last over is a big relief, as the fuel cost per unit has come down from Rs6.21 to Rs5.16. The fuel bill from the same period last year has also gone down from rs60 billion to Rs38 billion – part of which is due to lower actual generation.

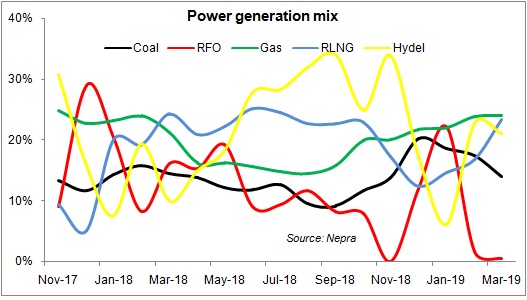

What has changed is the power generation mix. Barring a few blips in the recent months, where FO based generation kicked in – the overall situation has been on the improved side. Hydel was back in the fold, as March 2019 saw 21 percent share of hydel generation, up from just 10 percent in March of last year. Better and extended rains have surely played their part in filling up the dams.

More hydel means less or no FO. This pattern has been consistently observed ever since the reliance on FO has been decreasing. Earlier in the year, when hydel went down for extended periods, the government invariably had to fall back on FO. This is not to say that FO based generation will completely go away anytime soon, as the refineries continue to produce FO, and the government, as yet, has not found a mechanism other than continue procuring the same.

The implementation of merit order continues to be the exact opposite of its name. For many months in a row, a few more efficient RLNG based plants ended up not producing a single megawatt, despite availability and higher merit order than a few others. For March 2019, the excuse of FO based generation was not there either, which makes the whole exercise questionable.

The demand will surely pick from here on as the temperatures rise. That said, it will not be anywhere close to yesteryear’s demand. More emphasis needs to be put on following the merit order strictly and continue improving the generation mix – so as to reduce the impact of high capacity payments that may arise due to high availability but low demand

Comments

Comments are closed for this article.