Nishat Power Limited (PSX: NPL) announced its FY18 result yesterday which saw the company finally give out a dividend in the last quarter of the year for the company. NPL announced a final cash dividend of Rs1.5 per share (15 percent) for the FY18 period. Recall that NPL has not paid a dividend in any of the previous three quarters.

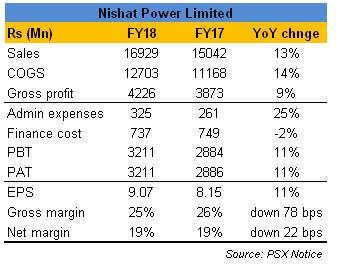

The company registered an increase of 13 percent in its top-line despite a fall in dispatches for the year. NPL’s load factor was 68 percent as compared to XX in FY17. The increase in revenue could be attributed to higher furnace oil prices (FO) which arose by 20 percent on a year-on-year basis.

NPL saw an increase of 9 percent in gross profit whereas gross and net margins remained stable compared to FY17, on the back of devaluation in the rupee. The company’s finance costs also witnessed negligible change in FY18. NPL continues to rely on short term borrowings to finance its working capital needs as the non-payment by NTDC has resulted in a constraint on its liquidity needs.

According to a research note by Arif Habib Limited (AHL), NPL’s overdue receivables amounted to R10.8 billion as of Mar-18, almost 66 percent up on a year-on-year basis. This might also be a factor in the company choosing to reduce its pay-out ratio in FY18.

Going forward, positive triggers for NPL and other IPPs would be settlement of the circular debt by the new government. Although, market expectations this time around are not hopeful of a one-off clearance like the one in 2013, a gradual payment might be on the cards. The company will also benefit from a further increase in interest rates which will boost its penal income on overdue receivables. Further rupee depreciation is also on the cards which will benefit the IPP.

Comments

Comments are closed for this article.