Rise in oil prices are a big factor in reisntating the oil and gas exploration and production sector's profitability; the first quarter performance of the sector showed the same as the sector's earnings improved amid rising international oil prices, and the same trend is likely to contnue in the first six-months' performance. When it comes to exploration ad production activities, the firms have been agressively investing during the low oil price times to reap benefits now.

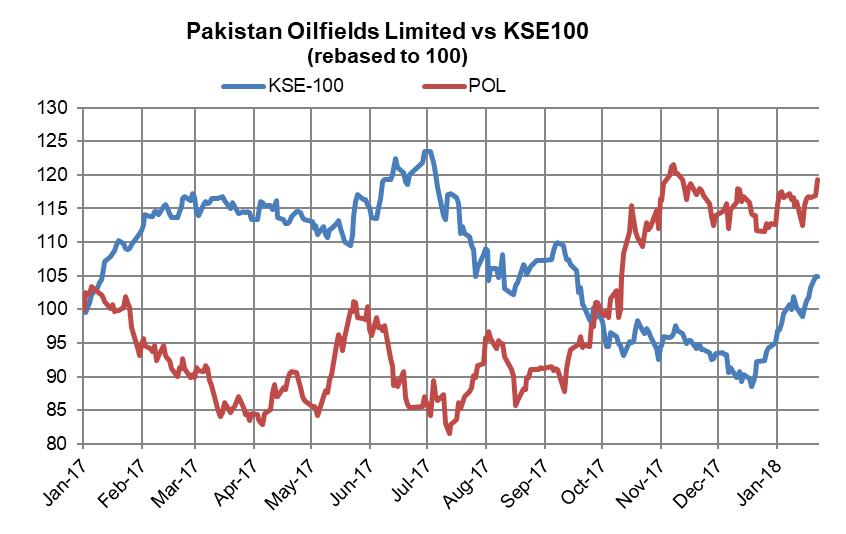

Pakistan Oilfields Limited (PSX: POL) has been the least aggressive lately compared to the other large E&Ps, which was also one reason for its bitter-sweet performance in FY17 (Read: POL - The bitter sweet truth published on September 12, 2017). POL has had heavy reliance on Tal Block. However, with the addition of Jhandial in its production portfolio, the company has good prospects of increasing its asset base.

Increased hydrocarbon production on account of additional flows from Jhandial and higher average hydrocarbon price due to 20 percent increase in oil prices supported POL's topline in 2QFY18. Effects of Jhandial were also seen in higher exploration costs, which had remained tepid in FY17. However, the recently announced revenues of the E&P firm for 2QFY18 were down by 15 percent year-on-year, which carried the squeeze all the way down to the firm's earnings. Despite higher dividend income from portfolio companies (Attock Petroleum and National Refinery) (469% increase in other income), POL's bottomline stood lower by 5 percent year-on-year.

Overall, 1HFY18 revenues for POL were up by a meagre three percent year-on-year, while earnings were flattish with 2.3 percent increase.

The primary reason for lower revenues booked in 1HFY18, and hence lower than expected earnings was the reversal of expected gas revenues worth around Rs3 billion due to enhanced gas prices from the conversion of Tal Block's pricing as well as previously un-booked revenue impact of over Rs3 as the government amended the Petroleum Policy 201 and imposed windfall levy not levied previously, as mentioned in the notes attached to the accounts.

The firm has decided to challenge the imposition of windfall levy in courts and has mentioned in the notes to accounts that the enhanced gas price incentive would be accounted after resolution of the matter.

Comments

Comments are closed for this article.