Bunny’s Limited (PSX: BNL) was incorporated in Pakistan as a private limited company in 1980 and was later converted into a public limited company. The principal activity of the company is the manufacturing and sale of bakery and other food products. BNL has its factory located in Lahore, Pakistan; however, its products are sold across the country as well as internationally. The company co-manufactures with some of the leading national and multinational companies including Pepsi Co., Unilever, and Engro etc.

Pattern of Shareholding

As of June 30, 2022, BNL has a total of 66.805 million shares outstanding which are held by 2894 shareholders. Directors, their spouse and minor children have the majority stake of 42.45 percent in the company. This is followed by general public holding 35.43 percent shares. Joint stock companies have a stake of 13.81 percent in BNL followed by Modarbas and Mutual funds which account for 6.13 percent shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2018-22)

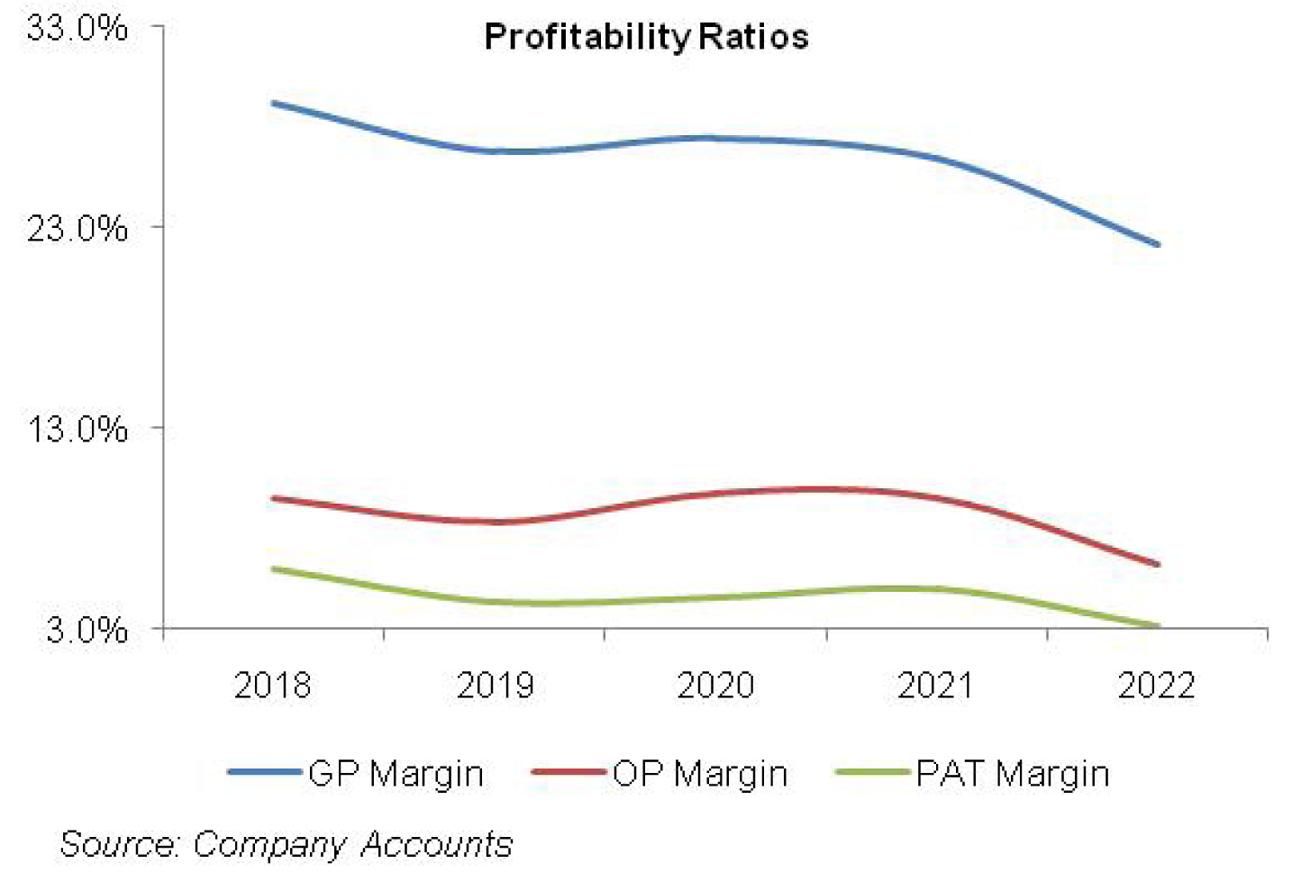

BNL’s topline has been showing steady growth in all the years under consideration. However, the bottomline ascended in 2020 and 2021 with a slump recorded in 2019 and 2022. The gross and operating margins of BNL tumbled in 2018 and 2019 and then recovered in 2020. In the subsequent years, gross and operating margins followed a downward trajectory. Conversely, the net profit margin dwindled in 2019, recovered in 2020 and 2021 and then bottomed out in 2022. The detailed performance review of each of the year under consideration is given below:

In 2019, BNL’s topline grew by 11 percent year-on-year on the back of increased demand combined with upward pricing. As the eating pattern of the people is evolving, people are increasingly focusing towards convenience food which is creating demand for bakery items particularly buns and bread. Buns and bread are the star products of BNL and contribute profoundly to its overall sales mix.BNL has an installed capacity of 13,500 metric tons in bakery division and 1800 in snacks division. In 2019, the company produced 11,150 metric tons of bakery products as against 10,965 metric tons produced in 2018. Snacks division produced 550 metric tons in 2019 up from 455 metric tons in 2018. Capacity utilization in snacks division is less due to low demand. High cost of utility, raw materials which mainly include sugar, flour, eggs, milk, cooking oil/ghee etc as well as costly packaging material culminated into a 15 percent year-on-year rise in the cost of sales. Gross profit marginally grew by 2 percent year-on-year in 2019, however, GP margin slumped to 27 percent in 2019 from 29 percent in 2018. Maybe to counterbalance the effect of rising cost, the company made a significant reduction of 58 percent year-on-year in directors’ remuneration coupled with chopped down entertainment expense, charity and donation as well as legal and professional fee. This trimmed down the administrative expense by 5 percent year-on-year in 2019. Selling and distribution expense mounted by 10 percent year-on-year owing to high salesman commission and discounts as well as vehicle running and maintenance charges due to increased deliveries to meet the demand. Other expense slid by 10 percent year-on-year due to lesser provisioning against WWF and WPPF. Despite a check on expenses, operating profit shrank by 3 percent year-on-year in 2019 with OP margin inching down to 8.3 percent from 9.5 percent in 2018. Finance cost grew by 2 percent year-on-year mainly on account of high discount rate. Net profit contracted by 19 percent year-on-year in 2019 to clock in at Rs.112.38 million with an NP margin of 4.4 percent as against 6 percent in 2018. EPS also slipped to Rs.2.19 in 2019 from Rs.2.69 in 2018.

In 2020, the net revenue of BNL posted a 9 percent year-on-year rise. While the closure of restaurants, educational institutions and offices due to COVID-19 related lockdowns produced a dent in the demand of bakery items particularly buns and bread, increased household consumption came to the rescue. Moreover, higher sales made in the initial quarters offset the effect of tamed demand during the COVID quarter. Overall, BNL produced 11,400 metric tons of bakery items and 565 metric tons of snacks in 2020. High flour cost, energy charges as well as other input cost resulted in cost of sales going up by 8 percent year-on-year in 2020. Yet, gross profit increased by 11 percent year-on-year in 2020 with GP margin clocking in at 27.5 percent. BNL hired additional employees during the year to meet the demand. This took the total employee count to 682 employees in 2020 from 669 in 2019. This pushed the salaries expense up which combined with an uptick in directors’ remuneration pushed the administrative expense up by 3 percent year-on-year in 2020. Selling expense also surged by 6 percent year-on-year primarily due to vehicle running and maintenance charges coupled with commission and other sales incentives. High provisioning against WWF and WPPF also resulted in a 22 percent hike in other expense. BNL also made Rs.6.6 million worth of other income in 2020 which is around 15 times higher than that of 2019. This was on account of gain on the sale of fixed assets as well as amortization of deferred income during the year. Operating profit boasted a considerable 28 percent year-on-year growth in 2020 with an OP margin of 9.8 percent – the highest among all the years under consideration. Finance cost rose by a huge 44 percent year-on-year in 2020 due to higher discount rate for most of the year except for the COVID quarter. Moreover, the long-term borrowings of BNL also rose during the year as it availed the SBP Refinance scheme for the payment of salaries and wages. Moreover, the company also installed a gas-based power plant during the year to cut back on its power cost. Besides, the company also started working on a fully automated production line for buns and bread for which the basic infrastructure was installed in 2020. Higher finance cost diluted the bottomline growth which posted a 14 percent year-on-year rise to clock in at Rs.127.80 million in 2020 with an NP margin of 4.6 percent. EPS also climbed up to Rs.2.49 in 2020.

Among all the years under consideration, BNL posted the highest topline growth of 28 percent year-on-year in 2021. The gradual resumption of economic activity led to an upsurge in demand. BNL produced 12000 metric tons of bakery items and 765 metric tons of snacks in 2021 to meet the demand. During the year, the company completed the installation of its dully automated bun line and started working on fully automated cake line and continuous fryers for its snack division. The cost of sales grew by 30 percent year-on-year in 2021. While gross profit climbed up by 23 percent year-on-year in 2021, GP margin inched down to 26.4 percent. Administrative and selling expenses grew immensely by 22 percent and 32 percent respectively in 2021. As of December 2021, the company had a total of 751 employees which greatly drove the salaries expense up. BNL also upped its advertising and sales promotion during the year to achieve higher market penetration besides providing commission and other sales incentives to pitch sales of BNL products. Other expense grew by 32 percent year-on-year due to higher provisioning for WWF and WPPF on account on increased profitability. Other income posted a massive 269 percent year-on-year growth on the back of gain on sale of fixed assets coupled with amortization of deferred grant. Operating profit magnified by 25 percent year-on-year in 2021, however, OP margin slightly reduced to 9.6 percent. Finance cost provided some breather as it slid by 10 percent year-on-year in 2021 due to monetary easing. This is despite the fact that BNL’s short-term and long-term borrowings have considerably increased during the year to meet its working capital requirements and support its expansion plans respectively. Net profit registered a stunning 39 percent year-on-year growth in 2021 to clock in at Rs.177.95 million with an NP margin of 5 percent. EPS clocked in at Rs.2.66 in 2021 which signifies a growth of 7 percent as the company issued 30 percent bonus shares during the year which increased its share capital. The company didn’t pay cash dividend in 2021 keeping in view its investment plans and the associated funds requirements.

2022 brought in another 25 percent year-on-year growth in BNL’s topline. However, during 2022, the topline growth has a great effect of upward revision in prices to counterbalance the effect of rising input cost due to domestic floods as well as Russia-Ukraine crisis. The production slightly inched up to 12400 metric tons in bakery division and 925 metric tons in snacks division in 2022. The cost of sales went up by 32 percent year-on-year. Gross profit grew by 5 percent year-on-year in 2022, however, GP margin drastically fell to 22 percent – the lowest among all the years under consideration. The company kept a check on its administrative expenses which grew by a mere 5 percent year-on-year in 2022 despite unprecedented inflation. While salaries expense grew substantially, the company contained directors’ remuneration during 2022. Distribution expense grew up by 24 percent year-on-year in 2022 due to sharp increase in fuel prices while other expense slumped by 34 percent year-on-year in 2022 due to lesser WWF and WPPF. Other income also declined by 55 percent year-on-year in 2022. Gain on sale of fixed assets was the main component of BNL’s other income in the past years; however, the company didn’t sell any of its fixed assets during 2022. Operating profit contracted by 19 percent year-on-year in 2022 and OP margin also stood at its five-year low of 6.2 percent. Finance cost grew by 32 percent year-on-year in 2022 due to multiple rounds of monetary tightening during 2022. The bottomline plunged by 22 percent year-on-year in 2022 to clock in at Rs.138.96 million with an NP margin of 3.1 percent. EPS also plummeted to Rs.2.08 in 2022.

Recent Performance (9MFY23)

During 9MFY23, BNL’s topline grew by 26 percent year-on-year in 9MFY23 due to increase in demand as well as prices. Cost of sales grew by 25 percent year-on-year in 9MFY23 due to rising food inflation. Upward revision in prices of BNL’s products helped in achieving a GP margin of 23 percent during 9MFY23 versus 22 percent during 9MFY22. Gross profit also rose by 29 percent year-on-year during 9MFY23. BNL cut down on its administrative expenses by 2 percent year-on-year in 9MFY23; however, distribution expense posted a steep 37 percent year-on-year rise during the period due to high fuel charges which profoundly increased vehicle running and maintenance charges. Other expense rose by 114 percent year-on-year in 9MFY23. The detailed financial statements are not yet available to comment on the underlying reasons for the rise in other expense. BNL didn’t make any other income during 9MFY23. Operating profit grew by 33 percent year-on-year in 9MFY23 and OP margin also slightly ticked up to 6.7 percent versus 6.3 percent during the same period last year. Finance cost severely rose by 66 percent year-on-year in 9MFY23 due to record high discount rate. While BNL put brakes on its long-term borrowings, short-term borrowings show no breather owing to increased working capital requirements. Due to high finance cost, bottomline slid by 7 percent year-on-year in 9MFY23 to clock in at Rs.96.99 million with an NP margin of 2.3 percent versus 3.1 percent in 9MFY22. EPS also plunged to Rs.1.45 in 9MFY23 versus Rs. 1.56 during the same period last year.

Future Outlook

With food inflation showing no breather, the cost of BNL is sure to hike. Furthermore, high distribution cost and finance cost owing to unabated fuel prices and discount rates respectively will put further pressure on its bottomline and margins. With steady demand growth and periodic price revisions, the company can, to some extent, pass on the onus to the final consumers and keep its bottomline in the profit-zone, yet, its margins are very much expected to take the hit in the coming quarter.

Comments

Comments are closed for this article.