Pakistan’s rice exports appear to be slowing down. Per PBS, volume exported declined by 9 percent during Q1-FY23 compared to the same period last year. Historically, exports usually do slowdown during the first quarter – as inventories start to run out – but the decline in the quarter ended Sep’22 appears to be stronger than usual. (For more, read “Rice exports: are good times over?”, published on November 08, 2022). Are rice exports facing strong headwinds, or will exports pick up with the arrival of the fresh crop?

Earlier this week, USDA made a strong cut to Pakistan’s rice outlook for marketing year 2022-23. The monthly update by the agency lowered rice production forecast to 6.6 million metric tons (MMT), down from 9.1MMT reported last year; and exports to 4MMT, down from record volume of 4.8MMT last year. USDA’s forecast follows the release of GoP’s own estimates during mid-October, which forecast national rice production at 5.5 MMT against the target of 8.5 MMT set in April 2022.

Although there appears to be consensus over significant damage to rice crop following the devastating floods, last month the Rice Exporters Association of Pakistan (REAP) had reportedly claimed that the “damage to the crop is minimal,” and that national production would comfortably reach 8MMT during the ongoing fiscal. It remains to be seen whether REAP’s forecast is on the money, or was an effort to calm the grain market and restrain local prices from rising out of control.

While REAP’s claim may not be without merit, it stands to reason why did rice exports slow down during Q1FY23 (Jul – Sep), if the crop has not performed so poorly? Interestingly, if commercial bank lending data is used as a proxy, rice stocks appear to have been running low long before the floods hit the country.

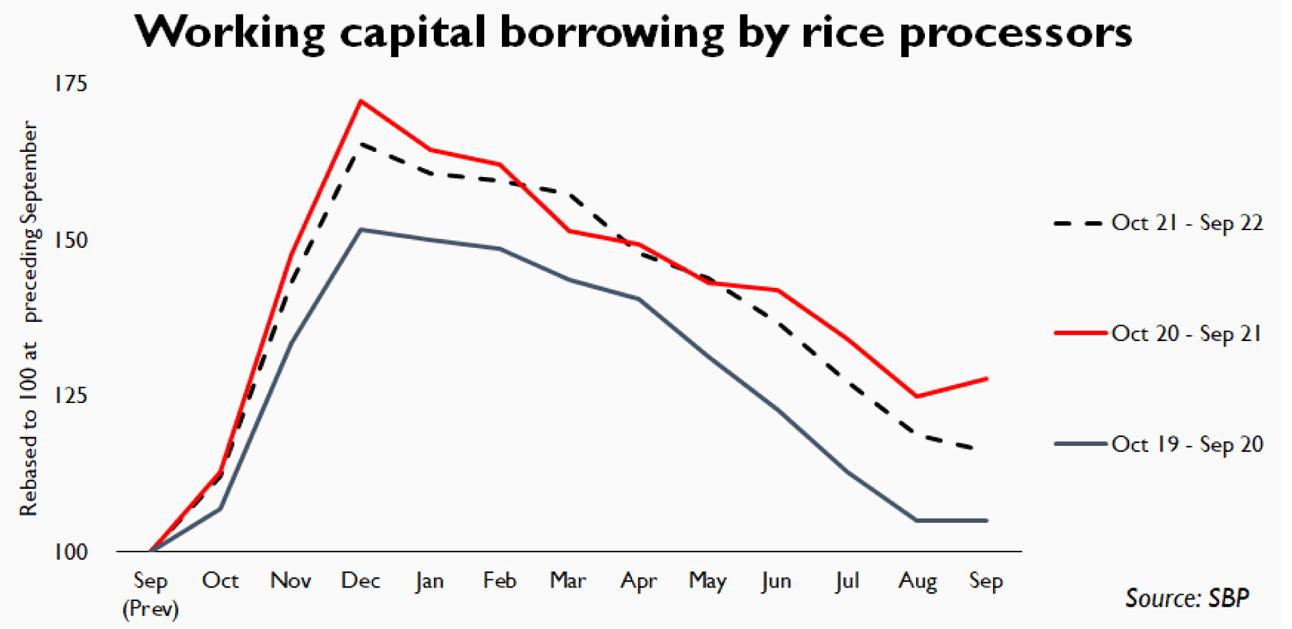

In the accompanied illustration, BR Research has used month-end working capital loans outstanding with rice processors as an indicator of rice stocks with the milling segment. Of course, not all procurement is financed through formal banking credit. However, since no data is available viz. stock positions, and nearly all rice mills are privately held, loans obtained for commodity financing may serve as a valid indicator of the overall market trend.

Note that since loan amount outstanding inflates naturally every year due to rising prices/inflation, 12-month data is re-based to September-end of preceding year. This is done to emphasize the seasonal movement in debt stock. Historically, rice crop harvesting in Pakistan begins in September and is completed by November; therefore, loans outstanding with the milling industry peaks by December and ebbs by September every year.

The credit data from SBP seems to suggest that loans outstanding with the milling segment fell at a far brisker rate between Dec ’21 and Sep’22 than same period last year. In fact, working capital loans to rice mills had already begun to climb up between Aug and Sep last year, while loan outstanding continues to decline during the ongoing season in these months.

But more significantly, borrowing for commodity financing did not peak at the same rate during the last marketing season (Sep – Dec 2021) as it had in the preceding year (Sep – Dec 2020). This is even though Pakistan not only achieved record rice production of 10.6MMT (official GoP estimate for FY22 varies from USDA’s), but also made record exports of 4.8MMT. Did strong demand from exporting destinations allow mills to finance procurement through own sources? Or did higher interest rates restrain formal sector financing?

Either way, both record exports, and bank data suggests that the industry began the current marketing 2022-23 with very low carryover stocks. If USDA and GoP’s forecast of poor crop performance – 5.5MMT to 6MMT - is correct, then rice prices in the local market should go berserk right about now (remember, REAP itself puts national consumption at 4.5MMT). Else, a massive slowdown in exports should be on the cards.

Comments

Comments are closed for this article.