After posting a strong performance in FY21, the banking sector’s prominent alternate delivery channels (ADCs) – the ATMs, point-of-sale (POS) machines, Internet banking and Mobile banking – have carried the growth momentum into the ongoing fiscal as well. As per the latest SBP data released earlier this week for the quarter ended September 30, 2021, there is strong double-digit growth on annualized basis in both the volume and value of transactions made by customers under each of these four ADCs.

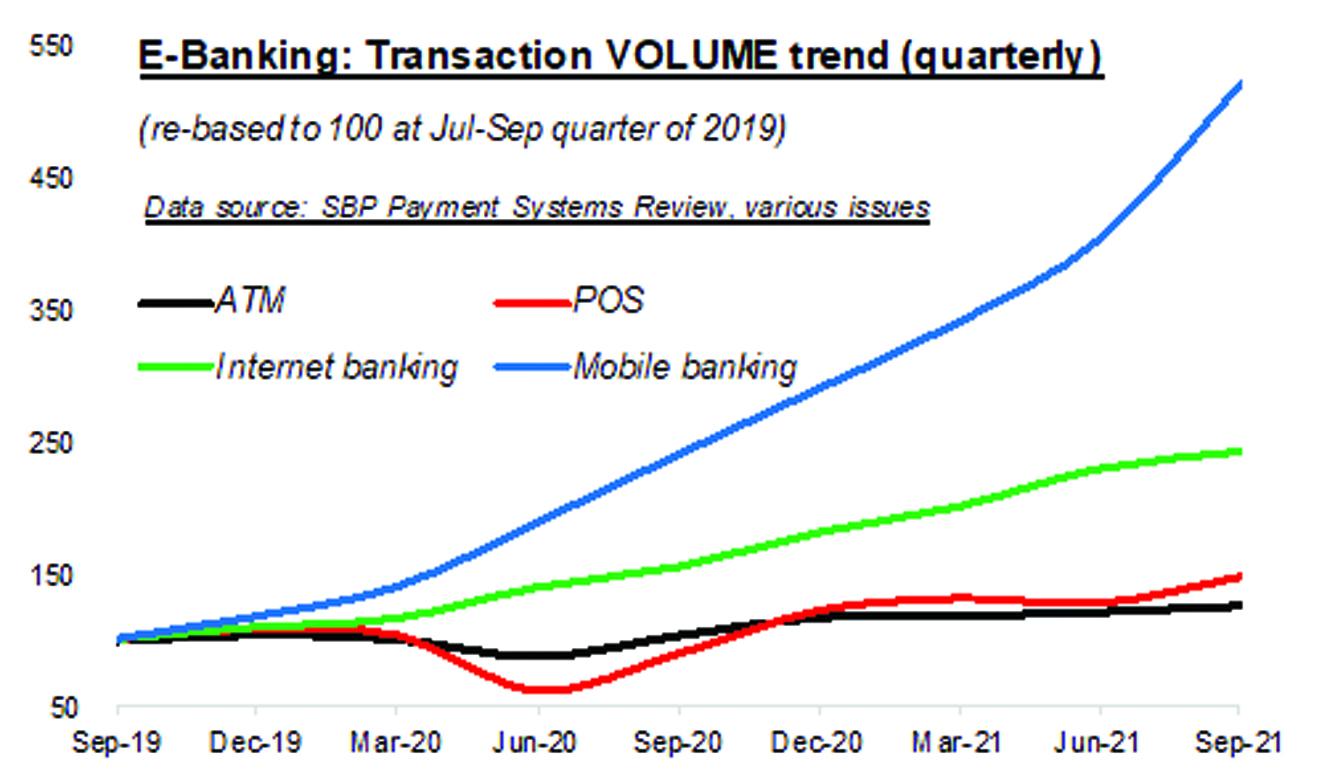

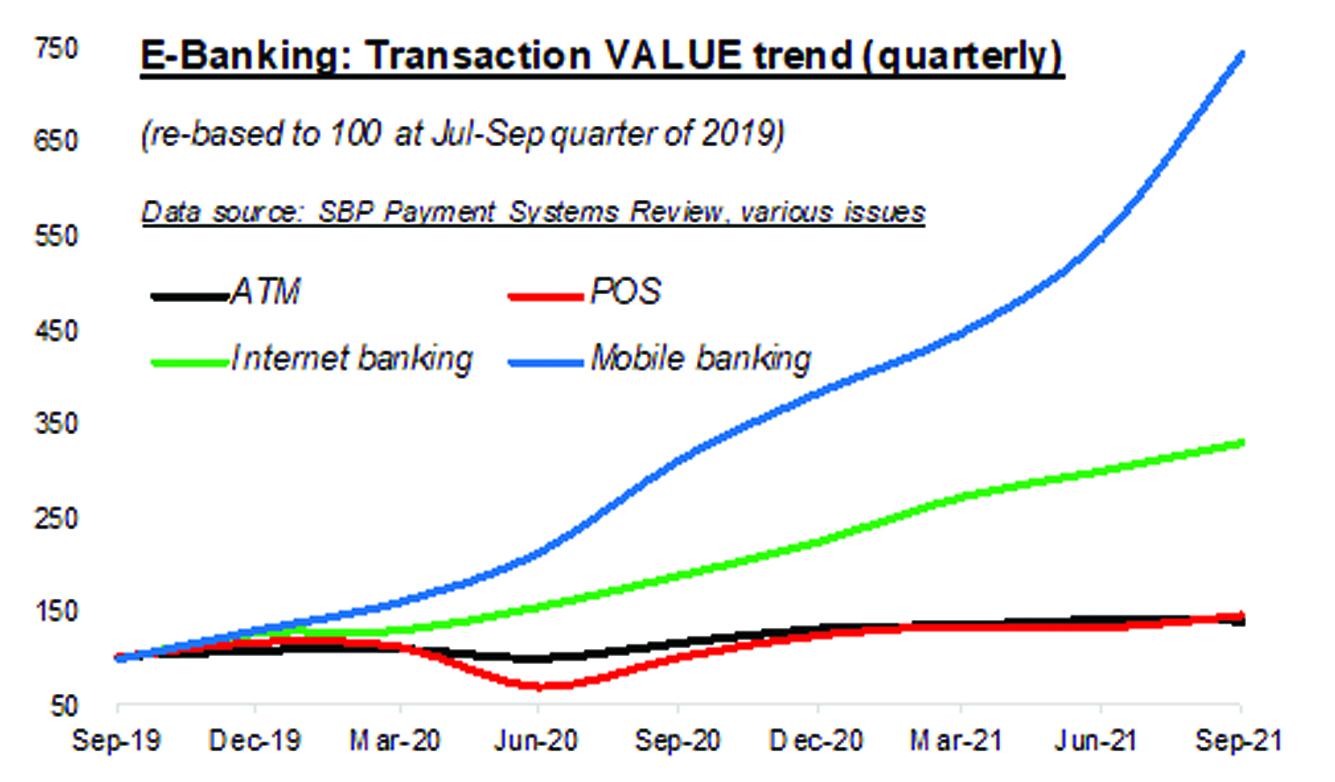

In terms of yearly growth, it is the Mobile banking transactions that especially stand out in the Jul-Sep 2021 quarterly review. Banking customers used this channel to make 79 million transactions in that quarter worth a value of Rs2.16 trillion – this signifies a yearly growth of 117 percent in volume and 138 percent in value. There were 11.3 million Mobile banking users as of September end 2021, higher by 26 percent year-on-year. The number of banks offering this service was 27, unchanged over the year.

In a first, Mobile banking transaction value surpassed even heavyweight ATM channel in 1QFY22 – that says something about its popularity! Average transaction size for Mobile banking was Rs27,322 in the quarter under review, up by 9 percent year-on-year. Not far behind in terms of annual growth race is the Internet banking channel, which banking users deployed to make 30 million transactions totaling Rs1.89 trillion in 1QFY22, with yearly growth of 57 percent and 74 percent, respectively.

There were 6.9 million Internet banking users as of September end 2021, up 60 percent year-on-year. There were 28 banks offering Internet banking service as of September 2021, same as in the year-ago period. Average transaction size for Internet banking – Rs 63,990 (11% YoY growth) – continues to remain highest among the four ADCs. Internet banking transactions in the said quarter were 2.5 times the volume and 3.3 times the value compared with the level seen two years ago in 1QFY20. Impressive, but not as much as Mobile banking, which grew 5 times in value and 7.5 times in volume in the same period!

Its transaction numbers may not be up there with its other ADC peers yet, but the POS channel generated a whole lot of receipts during 1QFY22. This is because there were 79,134 POS machines by September 2021 end, a phenomenal growth of 50 percent compared to September 2020 end. Some 28 million transactions worth Rs135 billion were made by banking customers using their plastic cards in the quarter, resulting in yearly growth of 67 percent and 46 percent, respectively.

The POS quarterly transaction levels reached 1.5 times in Jul-Sep 2021 compared to Jul-Sep 2019. Growth is expected to accelerate as tax incentives on POS transactions, increasing documentation of retail trade and consumer preferences may compel more vendors and service providers to install these devices. The average transaction value at POS machines was Rs4,801 in 1QFY22, down 13 percent year-on-year. This may suggest that POS use is broadening to less expensive purchases and services.

It may not be as flashy, but the good-old ATM continues to return significant growth in transaction numbers. During 1QFY22, banking users conducted 164 million ATM transactions with a sum of Rs2.15 trillion, generating yearly growth of 21 percent each in terms of volume and value. Quarterly transactions in 1QFY22 were 1.3 times the volume and 1.4 times the value compared to 1QFY21. ATM transactions averaged Rs13,188 in the quarter under review, down by a marginal 35 basis points year-on-year.

There were 16,546 ATMs as of September 2021 end, up 5 percent year-on-year. ATMs, which are a convenient source of cash withdrawal, hold special salience for first-time banking users. To boost growth in this channel, which is a key entry-point for other ADCs as well, banking service providers will need to increasingly fan out towards un-banked population segments so that accessibility is improved. Overall, these four ADCs have done well as the economy is fully open. Let’s see how they fare in the rest of FY22.

Comments

Comments are closed.