In an innovative move, SBP has expanded the scope of the Export Refinance Scheme (ERF). The objective of the move is to both enhance the limits and scope. The existing ERF (Part 1 and Part 2) limits (approximately Rs700 bn) are exhausting, and exporters are demanding enhancement. With this addition of new facility, the ERF exposure may increase by another 10-15 percent. That shall increase the subsidized financing to boost exports.

The facility can only be availed by those exporters who are eligible for existing ERF. This means spinning and weaving sectors will not benefit. The idea is to promote the value-added exports. The other advantage is that exporters can enter contract of 180 days with buyers if they avail this scheme. Otherwise, exporters are bound to bring back the proceeds within 120 days.

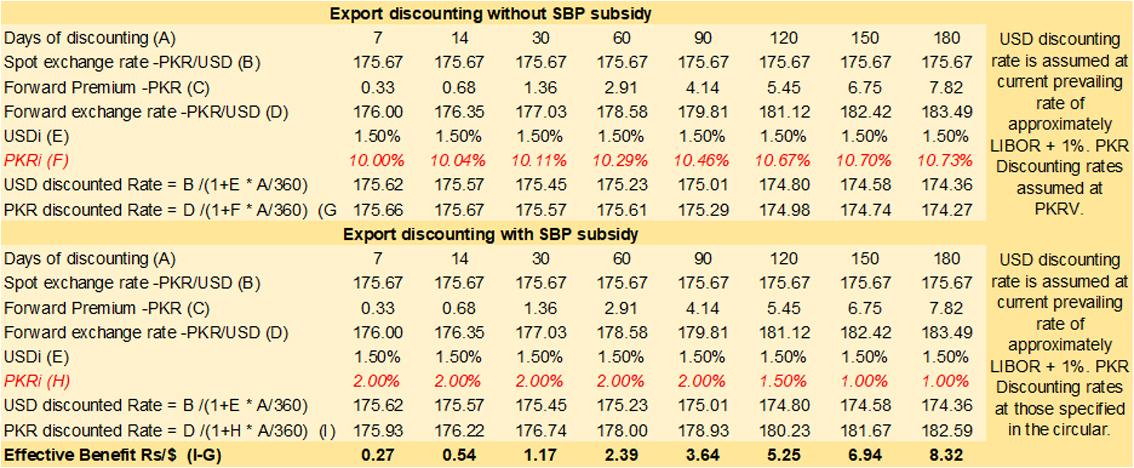

The scheme is effectively giving exporters an implied depreciation advantage of Rs8.32/USD (see calculations) - for only those who wish to avail this scheme. This may help exporters to cover the rising costs, and that is why they are demanding currency depreciation.

In the new scheme, exporters can obtain financing from banks by discounting their export bills/receivables (both post-shipment & pre-shipment). Exporters already use the discounting facility from banks, but there is no subsidy element in it presently. In this facility, they can discount at subsidized rates. Exporters can only avail this if they sell the foreign exchange associated with export bill/receivables and get rupees at the time of discounting.

The subsidy element is mouthwatering. Exporters usually discount their receivables (post shipment) or exports contracts (pre-shipment usually). The process is that export value is discounted in dollar value at applicable discount rate. A USD loan is created. Then another leg in the equation is to convert the USD into PKR at today’s spot rate for exporter to get liquidity. Then, the USD financing is knocked off when exports receipts are received. In this case, at the current spot rate of PKR/USD of 175.67, exporter receives conversion at PKR/USD at 174.27. The difference from the spot rate is the discounting cost.

With this facility, exporter may receive Rs182.59 against each dollar of future exports today for 180 days of financing. The gap is of Rs8.32/USD between discounting from bank versus using this facility. The rate advantage is of 9-10 percent per annum on current forward premium, USD, and PKR costs. The difference is due to the cost of one percent of ERF versus 10.73 PKRv (see detailed calculations in the table).

The scheme offered by the SBP is more lucrative for carrying financing of 6M. SBP has designed it in a way to incentivize exporters to sell their future exports in forward today. Higher is the tenor (maximum 6M) of discounting, better is the return for exporters. For example, the end user rate is two percent for 90 days discounting, 1.5 percent for 90-120 days and one percent or 120-180 days.

These rates are valid for three months (till 17th May 2022) and thereafter the rate shall increase by one percent to three percent (up to 90 days), 2.5 percent (up to 120 days) and two percent (up to 180 days). The early bird discounts are offered to attract more exporters in early days. Then the higher discount for longer time discounting is for exporters to sell further proceeds in future today.

SBP incentive is to gain for dollar liquidity in the interbank market and exporters are getting subsidized cover against forward with implied depreciation advantage without paying forward premium. Sooner the exporters realize and gain from the benefit, better it is for them. As the slogan says ‘Sab bech day’

Comments

Comments are closed.