Pakistan largely meeting IMF’S quantitative and indicative structural targets

- Revival of IMF programme will strengthen rupee and bring much-needed stability in external account

IMF’s financial assistance is intended to fix underlying structural disorders & economic vulnerabilities for the borrowing country, seeking short to medium-term bailout packages.

The IMF lending involves certain policy-level decisions and critical conditionalities. This structural disorder becomes even more complex and challenging for a borrowing country like Pakistan, if it is either deep-rooted or unaddressed by successive governments over a period of long time.

The IMF programme provides a broad framework, which is to be implemented with or without modifications, after IMF’s Executive Board assessment and the necessary periodic approvals. IMF’s lending is primarily conditional which has two structural benchmarks including; a) quantitative Performance criteria and b) indicative targets.

Pakistan has been going through this critical phase. Pakistan and IMF’s authorities had Technical & Policy levels talks in Islamabad and Washington in October 2021. The conclusive assessment and findings of IMF’s Executive Board is eagerly awaited by the officials, market participants and potential investors. The Finance Ministry has shared its optimism on successful completion of the IMF 6th Review.

We will dissect the IMF’s two structural benchmarks in detail and find out whether Pakistan is meeting Quantitative Performance Criteria targets and Indicative Targets.

Quantitative Performance Criteria targets:

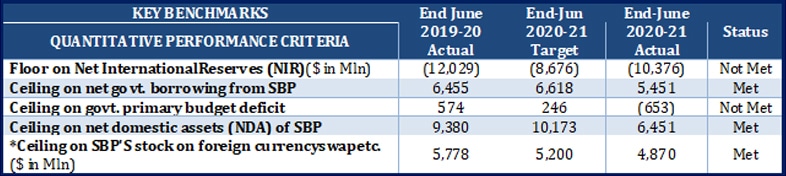

The Quantitative Performance Criteria targets includes; a) floor on the net international reserves b) ceiling on net government budgetary borrowing from SBP, c) ceiling on net domestic assets d) ceiling on stock of SBP’s foreign currency swap/forward position and e) ceiling on government primary budget deficit. The detailed assessment is hereafter;

Quantitative Performance Criteria Targets Vs Performance

Aggregate net positions in forwards and futures in foreign currencies of the SBP vis-à-vis the domestic currency (including the forward leg of currency swaps).

Net International reserves are the difference between usable gross international reserve assets & reserve-related liabilities including foreign exchange liabilities and Swaps.

Out of five, Pakistan meets IMF’s three key structural Quantitative Performance Criteria targets in quarter ended-June 2021.

Pakistan’s NIR stood at negative $10.37 billion as of June 2021 as compared to the IMF’s targets of negative $8.67 billion. Consequently, due to the higher reserve related liabilities, Pakistan is not meeting NIR targets for the ended-June 2021.

Despite the fact that Pakistan’s SBP reserves are at $17.47 billion as of 15th Oct 2021 & has import cover of over 3 months. On June 30th, 2021, SBP reported reserves were at $17.29 billion. This NIR was at higher levels of negative $12.02 billion as of June 2019-20 last year.

According to the IMF, Net international reserve is the difference between usable NIR assets and reserve-related liabilities. These NIRs are readily gives cushion to the borrowing country against external shocks. This can be utilised for meeting external payments or financing requirements for balancing the external account of the country.

However, with respect to ceiling on net government borrowing from SBP, Finance Ministry’s has shown its resilience not to borrow from the SBP.

Borrowing from SBP is highly inflationary and mounts pressure on the domestic commodity prices. Pakistan is comfortably meeting IMF’s quantitative target of ceiling Rs6.61 trillion. The net government borrowing from SBP stood was reported at Rs5.41 trillion as of June 30th 2021. In addition to this, Pakistan also meets ceiling on NDA of SBP which stood at Rs6.45 trillion as of 30th June, 2021 as against the IMF target of Rs10.17 trillion.

Pakistan’s Primary Budget deficit stood at negative Rs653 billion in FY21 as compared to negative figure of Rs757 billion in FY20.

On account of massive interest payments, growth in current expenditures and massive spending due to Covid-19 related expenditures, Pakistan’s Primary deficit has increased. Despite this, Pakistan’s tax revenues growth was in double digits which surpassed IMF annual targets. This stood at Rs4,764 billion in 2020-21 compared to Rs3,997 billion in FY2019-20. Given double digit growth in tax revenues and fiscal consolidation efforts, Finance Ministry can convince IMF authorities over Primary deficit numbers.

Pakistan is also comfortably meeting stock of the net Foreign Currency Swap/Forward position set by the IMF. The stock of net foreign currency swap/forward position stood at $4.87 billion as of June 2021 as compared to the IMF target of $5.20 billion in end June 2020-21. Therefore, Pakistan largely meets IMF’s key structural Quantitative Performance Criteria targets in quarter ended-June 2021.

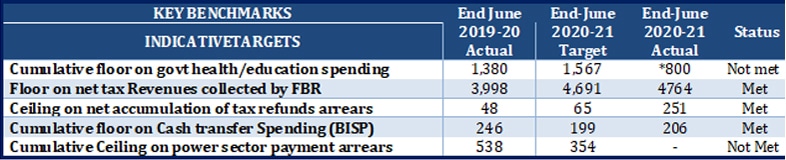

The Indicative Targets Vs Performance

Net Tax Revenue collected by FBR for Sep 2020-21 stood at Rs1,395 billion

Net Accumulation of Tax Refunds arrears for Sep 2020-21 stood at Rs59 billion

Overall, the entire Rs206.76 billion Ehsaas allocations for FY 2020-21 have been consumed for various social protection and poverty alleviation initiatives under Ehsaas. The estimated social sector spending is around Rs1,200 billion.

Date of cumulative ceiling on power sector payment arrears not available

Out of five, Pakistan meets three Indicative Targets in quarter ended June 2021. These indicative targets include; a) cumulative floor on social sector spending, b) FBR’s tax revenue targets, c) ceiling on net accumulation of the tax refunds, d) cumulative ceiling on power sector payment arrears.

Overall, under Ehsaas social spending program (which includes BISP), Pakistan has spent around Rs206.76 billion in FY2020-21. This includes the varying social protection & poverty alleviation initiatives as well. However, it is estimated Pakistan’s social sector spending including health and education stood at Rs800 billion. IMF’s target for social sector spending stood at Rs1.56 trillion. However, on account of massive covid-19 related expenditures, most of the countries have elevated levels of debt to meet fiscal needs. This has compromised their social sector spending and increased fiscal slippages.

On account of technical and distribution losses in energy sector, structural issues in updating tariffs and provision of unbudgeted subsidies have added further arrears in the power sector. Hence, on account of such fiscal constraints& elevated circular debt levels, country is likely to miss the IMF’s target on ceiling on power sector arrears as the actual numbers are not available.

On tax revenue side, Pakistan’s tax revenues grew by 19% or Rs767 billion to Rs4,764 billion in 2020-21 as compared to Rs3,997 billion in FY2019-20. IMF’s target was Rs4,691 billion in quarter ended-June 2021.

The FBR surpassed this target by Rs73 billion. In addition to this, tax refunds releases were also higher than indicative target of Rs65 billion. The actual tax refunds stood at Rs251 billion as of June 2021. This has not only addressed liquidity issues of the exporters but also boosted exports.

Pakistan is even meeting September 2021 indicative targets on tax refunds and FBR tax revenues. This is healthy sign that would give waivers on other indicative targets given ongoing economic momentum of Pakistan’s economy, if case is pursued well. Therefore, Pakistan largely meets IMF’s Indicative Targets in quarter ended June 2021.

Given the above assessment on the IMF's Quantitative &Indicative targets and overall outlook of Pakistan's Economic Performance, Pakistan‘s IMF-EFF program is expected to be revived.

Pakistan has no choice than to accept IMF’s tough conditionalities on withdrawal of exemptions and hike in power tariffs to keep this IMF program intact.

Pakistan's gross external financing needs for the next 12 months stood at $25 billion from April 2021-March 2022. Out of which $17 billion includes the amortizations to multilateral & bilateral official and commercial creditors. In order to plug the gap, Pakistan has secured financing commitments from various bilateral & multilateral partners as well.

Revival of IMF programme will strengthen rupee vs USD devaluation & bring much-needed stability in external account of the country. Therefore, it is expected that Pakistan is likely to hit annual GDP growth target of 4.8% in 2021-22 despite inflationary and policy rate hike trend which will remain a challenging task.

The article does not necessarily reflect the opinion of Business Recorder or its owners

The writer is a data-driven economist

Comments

Comments are closed.