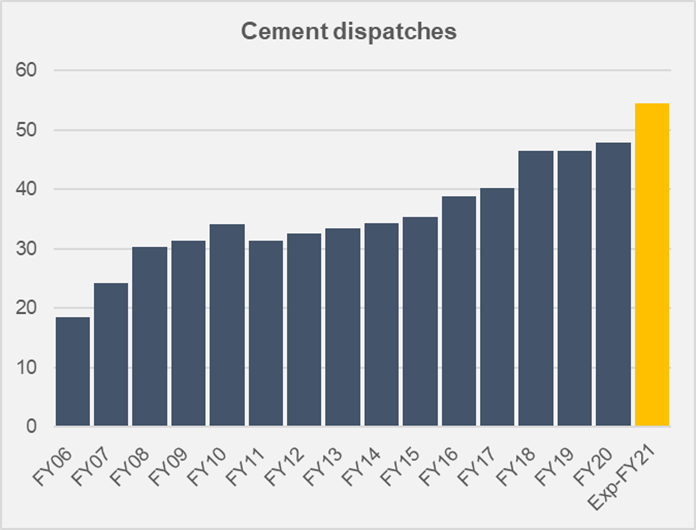

Whether the country has left covid-19 behind is debateable but the cement industry has certainly put it far in the backburner. A simple projection based on current growth patterns for 8 out of 12 months, indicates the industry could be selling near to 54 million tons of cement and clinker by the end of this fiscal year; a new peak and unquestionably one of the biggest annual jumps in history.

Cement firms have already started to make up for the losses of previous quarters by demonstrably becoming profitable on the back of not just strong demand but also better pricing in the markets, shrunk costs and a calm control on overheads (read more: “Cement: Concrete Revival”, Mar 5, 2021).

The industry had gone through a huge expansion phase only recently which raised debt levels and was costing some companies an arm and a leg in finance costs. With policy rate down to 7 percent, the burden of that expense item also reduced.

Should demand remain persistent over the next months, the trends that led to the improvement in the financials—combined gross margins stand at 23 percent in 1HFY21 versus 8 percent in the period last year while net margins stand at 11 percent during the period against a negative 1 percent in 1HFY20—will further bolster net incomes.

Zone-wise dynamics are also crucial to note. While growth between the north and south has been uniform—firms in the south have relied more on exports than ever before and specially compared to firms in the north for whom the domestic demand recovery has cast a silver lining in times where cross border markets such as India all but closed doors to incoming cement. South’s growing export share however may not be too good for margins as cement and particularly clinker sell at a discount in markets overseas compared to the prices firms fetch at home ground.

North players on the other hand have been witnessing a marked increased in domestic markets as demand has been coming aplenty from private and public run projects. This is reflecting in the north player’s impressive growth in revenue per ton sold—going between 8-16 percent for the handful of companies.

For south players, the same measure has remained muted and even negative in the cases of small firms like Power Cement. The company spent 19 percent of its revenue toward mark-up payments at a time when interest rates are low and borrowing costs are declining. New expansion had just come in for the company that caused sales to catapult but brought profits hurtling down.

Firms in the north have not much to worry about and can focus on new expansion plans (some are being financed under SBP’s TERF). With better coal inventory management, they can absorb costs more efficiently. Meanwhile, their margins would also remain robust as demand grows and price retention further improves.

Firms in the south, few and small by comparison will not be churning gold though (except for Lucky, of course). It would take housing and construction projects (whether under Naya Pakistan Housing or within the ambit of the construction package) to really get off ground in Sindh, and particularly in Karachi to substantially improve their profitability as they can divert resources inwards to supply to markets close to home that is unarguably better for both gross margins and overheads.

Comments

Comments are closed for this article.