While a lot of focus has been on the quantum of electricity base tariff revision (and rightly so), an equally important detail seems to have failed to gather much traction. The issue in question is a very substantial change in the consumption patterns of domestic electricity consumers, as referenced in the base tariff revision motion for 2021.

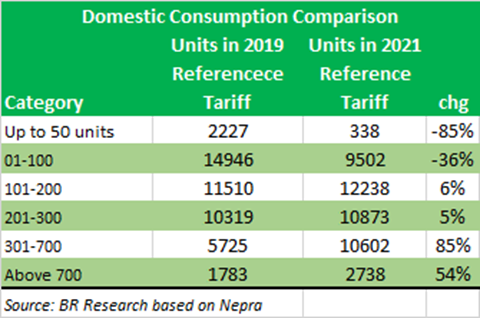

The lowest consumption slab, commonly referred to as baseline category consuming up to 50 units has undergone the largest change, with an 85 percent dip from previous base tariff revision in 2019. The baseline slab had been absolved of most upward price revisions in the last ten years, including monthly and quarterly tariff adjustments. The category has now been also subject to 98 percent tariff increase. One wonders if virtually all baseline power consumption will cease to exist in just two years’ time.

Similarly, the second slab falling in the 1-100 units has also been put under a substantial downward revision, with 36 percent dip projected in actual consumption, and the share going down from the highest amongst all slabs to being only higher than the highest consumption slab.

The graduation from low consumption to higher consumption is an abrupt one and raises questions if the demand patterns have actually changed this much in such a short span of time, especially when power prices have been on the rise and real wages have not. Nonetheless, the lowest two consumption slabs, which accounted for one-third of all domestic consumption, are now slated to account for no more than one-fifth.

The biggest jump is seen in the 301-700 units slab, with a 10 percentage point increase in consumption share. The mentioned slab is projected to be responsible for more than one-quarter of the base revenues. One could argue that the total domestic consumption which has been projected to stay lower year-on-year, may actually rebound after a three-year period of lull. And that play its part in augmenting the revenues further.

But the consumption mix remains a big question mark, and failure to achieve how it is projected, could lead to serious shortfalls in revenue, none of which is budgeted for. More importantly, the revised consumption shares also call for another serious look at electricity inflation as computed by the PBS. Recall that the PBS had altered its methodology on weighted consumption just recently.

The new reality significantly changes the consumption patterns of the given quintiles that the PBS uses – and would lead to meaningful changes in electricity inflation index. The likelihood of that happening though, remains very low, given reluctance to change especially after the relatively recent rebasing exercise. From what it appears, electricity tariffs stand the risk of being underreported in the CPI, for times to come.

Comments

Comments are closed.