Gharibwal Cement Limited (PSX: GWCL) was set up in 1960, as a public limited company. Two years later it was listed on the stock exchange and by 1965 it started commercial production with production capacity of 1200 tons per day.

The company produces and sells cement, with an annual production capacity of 2,010,000 tons clinker as of FY20.

Shareholding pattern The following information was extracted from the company’s website as at January 13, 2021. Close to 89 percent of the total shares in Gharibwal Cement are owned by its directors, CEO, their spouses, and minor children. Within this category, Mr. Muhammad Tousif Peracha, the CEO of the company is a major shareholder. About 6 percent shares are with the general public and a little over 2 percent are held in foreign companies. The remaining 3 percent shares are distributed with the rest of the shareholder categories.

Historical operational performance

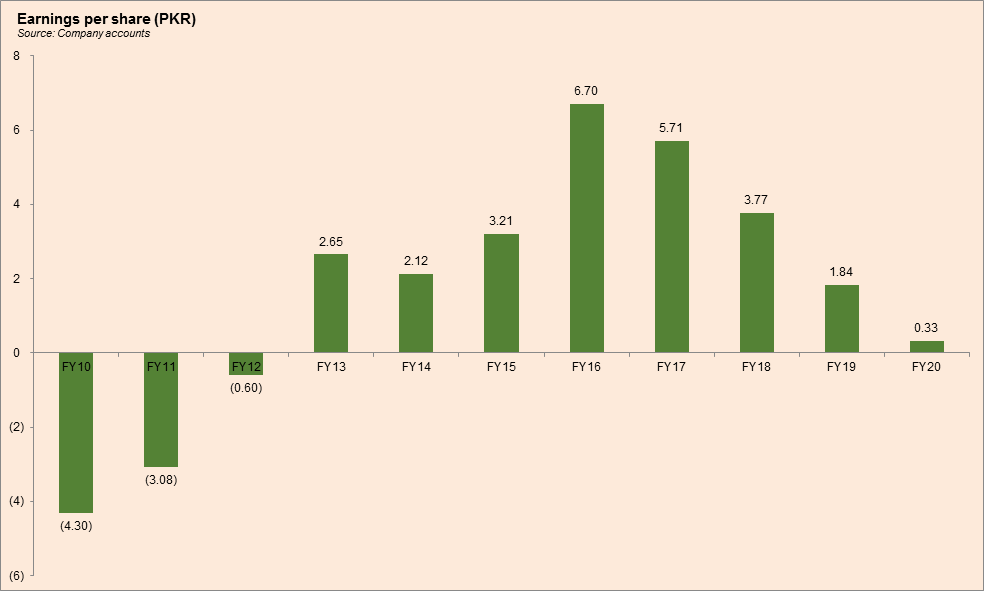

Gharibwal Cement has mostly seen a rising topline over the decade, except for more recently in FY19 and FY20, whereas net margin was highest between FY15 to FY18 and has been declining since.

In FY17, the company saw one of its lowest sales revenue growth rates at 6.7 percent. The overall cement industry registered a growth of 3.7 percent year on year. For the company, cement dispatches increased by 4.6 percent to 1.6 million tons. For the previous six years, cement sales volumes had followed an upward trajectory. However, a reduction in selling prices due to tax impositions and duties subdued the net sales revenue. Moreover, cost of production also increased to nearly 66 percent of revenue; this was due to a rising fuel and power expense that made up almost 64 percent of total cost of production. Thus, net margin reduced to 20 percent, down from preceding year’s 25.5 percent.

Sales revenue growth rate, although positive, further decreased to 4 percent during FY18. Cement dispatches registered an 18 percent increase during the year, reaching 1,89 million tons, while there were no clinker dispatches. Most of the sales volume was dominated in the local market as local sales revenue grew by 10 percent despite an 8 percent reduction in selling price. In the absence of clinker sales as well as a reduction in export sales, latter by nearly 40 percent, the total sales revenue for the company could only grow by 4 percent. On the costs side, cost of production increased to almost 75 percent of revenue, due to currency devaluation from Rs 105/USD as of June 30, 2017 to Rs 121.60 on June 30, 2018. This made coal imports more expensive. With the rise in distribution and finance expense - latter due to higher interest rates - led net margin to fall to almost 13 percent.

Gharibwal Cement saw a 4.5 percent contraction in its sales revenue during FY19, whereas cement dispatches reduced by 11.4 percent at 1.676 million tons. There was a decline in both export sales as well domestic sales. Export sales were impacted due to Pakistan-Indian border tensions as India was one of the destinations for cement exports from Pakistan. However, despite the 11.4 percent drop in sales volumes, the decrease in sales revenue was not as pronounced due to an increase in selling price in the domestic market. However, cost of production and finance expense continued to climb for the third time in a row, squeezing profit margins; net margin for the year was recorded at 6.6 percent.

Reduction in sales revenue was more pronounced in FY20 as it fell by 22 percent. There was a 1 percent decline in cement dispatches (1.66 million tons) combined with a 21 percent decline in selling price that led overall revenue to fall by 22 percent. Most of the decline in volumes was due to the lockdown imposed in the last quarter of FY20 due to the Covid-19 pandemic. Cost of production increased to its highest seen since FY11, at 99 percent of revenue. This was attributed to increase in “the rate of royalty on raw materials with effect from July 2019 that increased the respective expense by 161 percent year on year”. Thus, net margin fell to 1.5 percent.

Quarterly results and future outlook

There was an almost 27 percent rise in topline year on year during 1QFY21, while sales volume registered a 13 percent increase from same time last year; there was also an improvement in selling price. Cost of production was also lower year on year at 78 percent of revenue. Profitability was also enhanced due to a reduction in finance cost as it reduced due to a fall in interest rates during the year.

The company foresees rising cement demand in the domestic market. By the end of FY20, a new clinker storage silo of 150,000 tons capacity was completed; this would aid in meeting the rising demand in future.

Comments

Comments are closed.