So, the power stocks rallied at the Pakistan Stock Exchange (PSX) as another effort to clear the circular debt stock is underway. The idea is to pay the IPPs Rs450 billion in cash and in kind in three tranches throughout the year. This takes one back to the early days of the last PML-N government, when a similar amount was settled with the IPPs with a similar aim of putting an end to the menace.

What should not go unnoticed is the fact that the current settlement plan is quite different from the one adopted by the previous government. There is an element of savings resulting from the negotiations with the IPPs, which proposes to change the capacity payment structure via changes in currency indexation. Good job done on that front, but this must not be confused for a step that will stem the flow of circular debt.

The government’s inability to timely announce tariffs has long been a major cause of accumulation of arrears. The political will remains missing for one reason or the other. Of course, higher power generation cost plays a big role, and efforts towards mitigating that to some extent through renegotiating IPP contracts must be lauded. But that alone will not serve the purpose. Payment to the tune of Rs450 billion is the carrot to lure IPPs and should not be viewed as a step that could in and of itself stem the flow of arrears’ accumulation.

While one can go on saying how capacity payments are the elephant in the room, but there may well be other similar-sized animals too in the room. The unfunded subsidies have been curtailed to an extent, which is a job well done. But the ills of the state-owned distribution companies go on unbated, and status quo in disco affairs would not magically lead to an end to the circular debt menace.

It has been said numerous times before, yet it can never be said enough that the distribution companies are at the heart and center of the power sector woes. Years and years of snail-paced progress at discos means that even if everything else is taken care of, from tariff rationalization reflecting full cost recovery to timely announcement to tariff adjustments, the sector will still be staring at a colossal yearly loss north of Rs200 billion, at the very start.

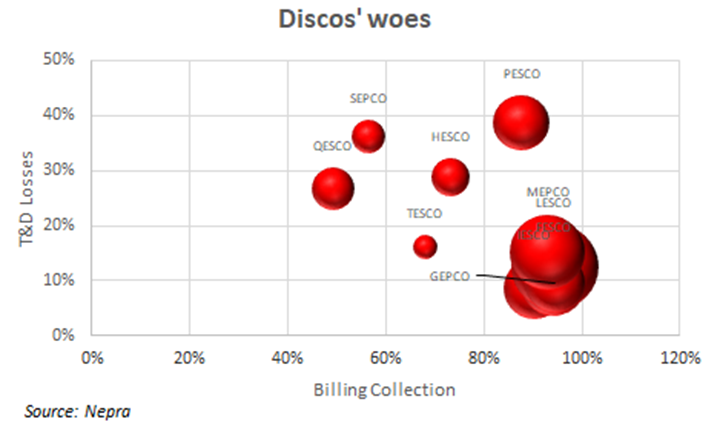

Discos bleed 18.5 percent in transmission and distribution losses yearly. But that is not the biggest worry in terms of tariffs, as the regulator allows 15.5 percent to be covered in consumer tariffs. The real deal is the billing collection rate, which is assumed at 100 percent by Nepra – but the actual recovery comes close to 90 percent. This is where the disparities start, and discos fail to pay CPPA, which in turn find it difficult to pay the IPPs, who withhold the fuel suppliers’ payments.

What needs to be done to resurrect the discos may partly be a technical debate. But most of it rests with the government showing some spine and take the right decisions. Privatization may well be one, but not the only solution. The incentive to underperform should be ended and be replaced with repercussions for underperformance. Without it, payment to IPPs every five years will be labelled different names, without actually addressing the root cause. The consumer may not be directly paying for the government’s inefficiency through electricity bills, but the amount is still being paid from the taxpayers’ money. Standalone, that did not work in the past, and won’t in the future.

Comments

Comments are closed.