The outbreak of a pandemic, the ensuing lockdowns and slowdown in business activity led to the largest restructuring and rescheduling of loans ever in the country’s banking history. As per latest estimates by State Bank of Pakistan (SBP), more than Rs844 billion of existing loans have either been restructured, or rescheduled. For the uninitiated, this simply means that businesses and individuals who were supposed to make their principal, or interest payments were allowed a grace period of up to one year to make their payments. Such a grace period enabled businesses, and individuals to preserve their liquidity during a health, and economic crisis.

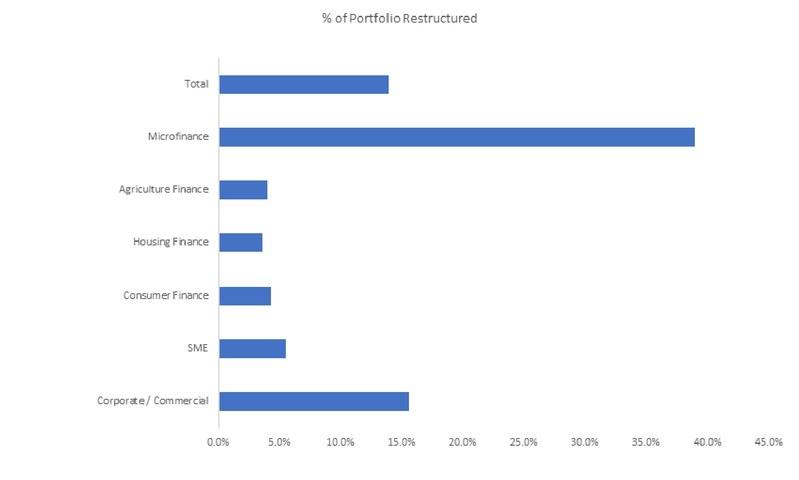

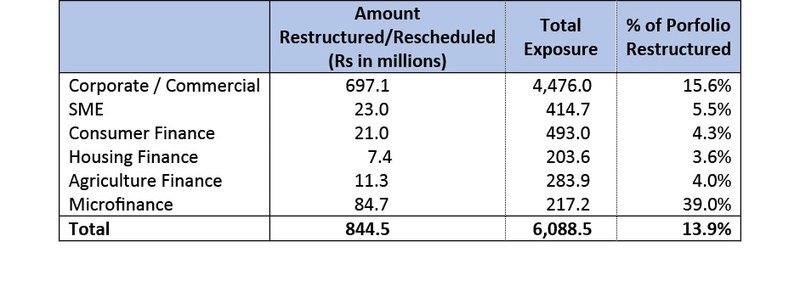

Total private sector lending is at Rs6.08 trillion, which has largely remained flat over the last twelve months. Restructuring or rescheduling of Rs844 billion, implies that 13.9 percent of exposure to private sector found it difficult to make repayments, and hence got restructuring, or rescheduling approved. The grace period is supposed to end from April 2021 onwards, and it is at that critical juncture that the ability of financial institutions to absorb any potential losses will come into play. At a time when 13.9 percent of private sector lending has been restructured, econcomic growth prospects remain muted, and real incomes continue to erode – credit risk remains considerably elevated.

Microfinance is the hardest hit segment, with 39 percent of loans extended by microfinance banks being either restructured, or rescheduled. As the interest rate on microfinance debt remains significantly high, mostly in excess of 35 percent, borrowers may have a tough time paying back what they owe. This does not include amounts restructured by microfinance Institutions which are regulated by the SECP. Similarly, almost 15.6 percent of corporate and commercial loans have also been restructured, or rescheduled, as mid-to-large enterprises find it difficult to make necessary repayments.

Credit risk remains elevated. Even if a fifth of the loans go bad, they may severely affect capitalization of the banking sector, particularly for the mid-to-low tier banks. In such uncertainty, a risk-off mode is largely justified for the banks, given the lack of clarity regarding sources, and magnitude of potential growth. A potential hike in policy rate is only going to make things worse. The central bank says the proportion of non-performing loans is at a comfortably low, two percent. But stress testing of exposures, impairment assessments and a buffered-up capital base could help prepare the banks for leaner times.

Comments

Comments are closed for this article.