Janana De Malucho Textile Mills Limited (PSX: JDMT) was established in 1960 as a public limited company. It commenced commercial production three years later in 1963. The company manufactures and sells yarn at its textile unit in Kohat, Peshawar.

Shareholding pattern

More than 50 percent of the shares are held with the associated companies; of this, Bannu Woollen Mills Limited holds most of the shares. About 28 percent are distributed amongst the local general public, 10 percent is under the banks, DFIs, NBFIs category. Share of the directors, CEO, their spouses and minor children is negligible at less than 1 percent. The remaining 5 percent is distributed with the rest of the categories.

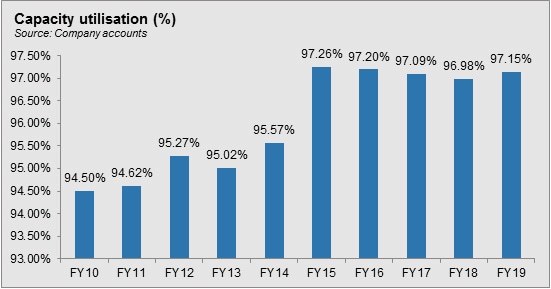

Historical operational performance

Over time, although topline has seen growth, profit margins have contracted due to a high percentage of cost consuming revenue. From roughly taking up 85 percent of the revenue, over the years, cost of production has risen to consume more than 90 percent.

In FY15, the company saw its highest decline in sales revenue by nearly 15 percent. This was attributed to the dumping of cheap Indian yarn in the market, which not only hurt sales prospects of locally manufactured yarn, but also drove down prices. While India had imposed a cumulative 30 percent duty on imported yarn entering the Indian market, Pakistan, on the other hand had allowed almost duty-free import into the country. With fixed costs remaining intact, gross margins halved year on year whereas net margin nearly disappeared in comparison- to a less than 1 percent.

Sales revenue fell further in FY16, although by a marginal almost 2 percent. There was a decline in both absolute terms as well as volumes. This was again attributed to the availability of cheap imported yarn from India. However, by the second quarter of FY16 a 10 percent regulatory duty was imposed which reduced the import. This helped to raise prices, although the effect of it could not entirely erase the impact as given by a lower revenue. With other factors remaining unchanged, net margin reduced further.

The company saw a very marginal gain in revenue in FY17 at less than 1 percent. This was partly attributed to the zero-rated sales tax regime. Cost of production, on the other hand, increased to a noteworthy 95 percent of revenue- the highest seen thus far. This was due to an increase in minimum wages to Rs 14,000 in addition to an increase in average raw material consumption rate. Several textile companies had shut down their operations in the last few years due to their inability to absorb the high cost of doing business. The company’s report for the year suggests that cost of production of gas and electricity is 30 percent higher than its regional peers, namely India, Bangladesh and Vietnam. Thus, the year concluded with a net loss of Rs 8 million.

In FY18, the textile mill recovered, as it grew its topline by a little over 10 percent. Although the company itself is not present in the international market; as part of the textile industry, it does feel the repercussions. The currency depreciation made exports favourable, which otherwise were uncompetitive. This translated into higher demand for the company’s yarn. However, this higher revenue could not be reflected into better profits; instead, losses escalated to Rs 62 million. This was a result of lower sales rate due to the presence of imported Indian yarn. In addition, raw material prices also saw an incline. Despite a rise in local cotton production, it still failed to meet demand, resulting in the need to import. This also had an impact on finance costs as “the company was forced to fully utilize its running finance limits in order to fulfill its daily working capital/production requirements”.

The company gained profitability as revenue witnessed a double-digit growth of 21 percent in FY19. This can be attributed to the currency devaluation and the resultant demand generation from clients downstream. The higher revenue also improved the capability to absorb costs, thus reducing cost of production as a percentage of revenue. Apart from an increase in finance costs which was a result of a higher policy rate, most other factors remained similar, thereby raising profit margins for the first time since FY14.

Quarterly results and future outlook

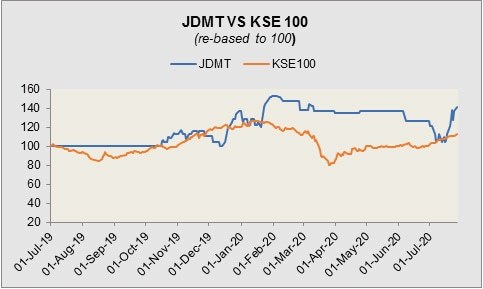

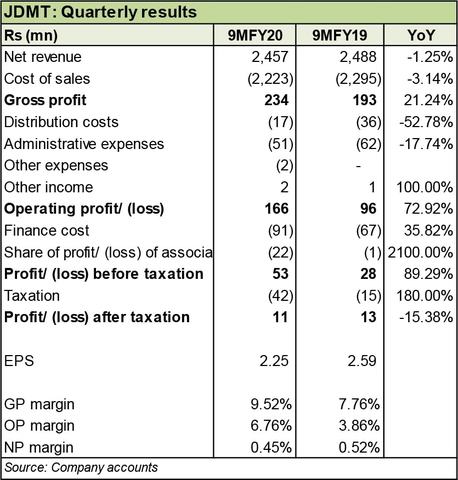

During 9MFY20, the company saw its topline contracting by a marginal 1 percent, whereas most of the revenue-more than 40 percent was generated in the third quarter of FY20. The decline is mainly attributed to the elimination of the textile sector from the zero-rating regime. As a result, there has been a massive increase in sales tax payment. In the absence of timely refunds from the government, the company, along with many others face a liquidity crisis; so while there was an improvement in operating margins, net margin nearly remained flat due to loss from associated companies.

In the wake of the pandemic, and despite government’s measures to support industries, the company foresees dim prospects of recovery in the near future for the textile industry, especially the spinning segment which has witnessed a consistent decline in the last few years.

Comments

Comments are closed for this article.