Here’s what we know: there is a housing subsidy of Rs30 billion that we have known for a while. This is a one-time cash subsidy that will be given to 100,000 houses initially constructed, in the form of padding the down-payment of the mortgage. In addition, there is a mark-up subsidy—mortgage will be offered at 5 percent (for 5 marla houses) and 7 percent (for 10 marla houses) to households. The government will subsidize the difference between the market rate and 5-7 percent concessionary rate offered under the scheme for a period of five years.

On the supply side, a one-window operation for approvals has been put in place which will reduce delays and speed up delivery time of the projects. Investors have the added incentive to put it any kind of money into development and no questions will be asked as to the source of funds. There is also a 90 percent tax waiver for those who want to invest in the NPHP scheme while for the entire industry, the tax regime has been changed to a fixed tax system (read more: “Naya Pakistan Housing: Supply-side snags”, May 29, 2020).

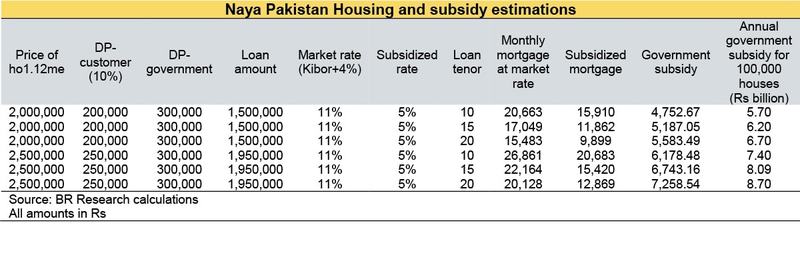

Quick calculations suggest that the additional burden of the mark-up subsidy (for 100,000 houses only) will fall between Rs6-9 billion every year depending on the tenor of the loan. This could be budgeted but if the government intends to meet the 5 million housing mark, and not just 2 percent of what was promised, funds will have to be moved around. Some financial support could be sought from the World Bank which has shown considerable interest in promoting housing finance in Pakistan.

Certainly, some earlier questions about the subsidy have been answered but many more remain. There still seems to be a major black hole of information. The government is relying on provinces to identify demand but that exercise has not been done. For one, housing stock and housing shortage is still a mystery. There are estimates which are based on lazy metrics. Even if those estimations are used (10-12 million houses across Pakistan are needed is one such estimate), the distribution of housing needed along socioeconomic diversity is unknown. How can a subsidy be awarded without understanding the dynamics of housing demand and supply and subsequently carving out a criterion for the subsidy based on these?

Building on that alone, any claims to boost affordability should at least be backed with the knowledge of what affordability means for a Pakistani household. The government can dole out subsidies all it wants and they might still not be affordable. Calling it low-cost housing is also a problem. The lowest income households in Pakistan spend 43 percent of their incomes on food and 21 percent on housing, electricity, gas and other fuels, at a monthly income of about Rs20,000. How much can these households put aside for a mortgage payment? Perhaps home ownership is not a solution for everyone and other housing solutions need to be curated (such as rental).

Secondly, given how expensive (and scarce) land is, why is the government aiming to build 5 and 10 marla houses when it should be going mix-income high rise development where land can be better utilized and cost per home can be further lowered. In fact, if the first 100,000 houses is a pilot project, vertical development would be set a pretty good precedence. Other regulatory challenges such as implementation of foreclosure laws, creating land banks etc. are critically important as well.

To be sure, the subsidy together with other supply side incentives is most likely to intensify activity in the construction and housing sector which could potentially become the biggest growth driver over the next year as services and other industries bow out on the heels of covid-19. However, whether the subsidy will be fair and best utilized and how well-distributed housing supply will be due to the incentives, are important questions that the government needs to ask, and perhaps may not, in all the haste to meet its ambitious targets. One thing is certain, however noble the cause, the NPHP needs product design.

Comments

Comments are closed for this article.