The year of two bottoms is behind us: the first seen in August 2019, and the second in April 2020. Both bottoms helped investors make a lot of money. Will FY21 also provide investors similar opportunities? That the market is chewing over its options and direction is perhaps why June 2020 saw KSE-100 ending largely flat with average daily trade volumes easing to 114 million as against 135 million in May 2020 and 161 million in the month before.

In part, June’s flattish performance was dictated by budget related worries, and fears triggered by the rising lines on Pakistan’s Covid-19 chart – both of daily cases and daily deaths. The budget went by without much ado, whereas Covid-19 charts are now doing better than earlier feared, especially when one keeps into account the horrifying studies put out by Imperial College London, and the likes.

The worms it seems have either not hatched or have decided to come out of the can later from the blindside, especially while investors are busy cherry-picking stocks. (See BR Research’s “KSE-100: waiting for the worms?” June 1, 2020)

Two key developments seem to have killed at least some worm eggs, if not most of them. The consistent lowering of the interest rates, which makes equities valuations a little more attractive than before and makes the alternative rather boring on account of falling earnings yield on government bonds.

Second is the government’s decision to place limits on institutional participation in National Savings Scheme (NSS), which should attract savings of corporates and other institutions towards defensive or high dividend yielding stocks.

Given Pakistan’s thin market of few investment options and small float, these two factors should help the index take off. Of course, much depends on the extent of the damage to earnings caused by Covid-19, and risks of further hits to farming and agro-based income courtesy locusts round two feared this month.

To some degree, the impact of Covid-19 on economy and corporate earnings should start becoming visible once private sector credit data, balance of trade data, and the Large-Scale Manufacturing numbers start coming in.

But the position might remain foggy until corporate results for the quarters ended June and September 2020 are announced – foggy enough to prevent bulls from going all in. If results ending June 2020 will shed light on Corona’s impact on sales and margins during the peak lockdown period, results ending September 2020 will shed light on how companies did in the smart lockdown period, which could possibly be the norm for a foreseeable future.

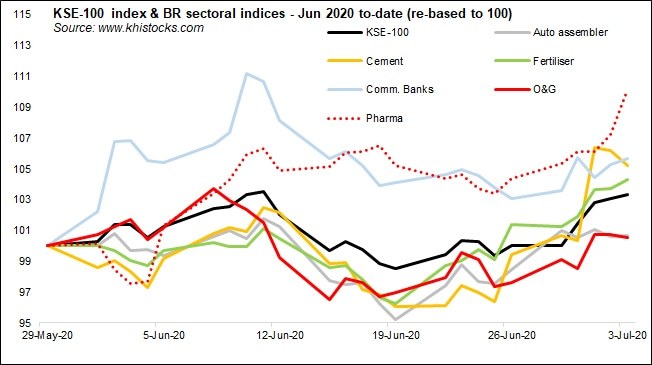

In light of these realities, expect smart investors to keep one eye on low priced fundamentally strong stocks for long term play and another eye on the can of worms, including the macro side where GDP slowdown (at home and abroad in exporting destinations), lofty tax collection targets, and inflation requiring keener than usual observation – nay surveillance. On the subject of cherry-picking, expect sector rotation where fertiliser and banks have begun to invite interest.

The outlook of economic recovery is still fragile, and the risks cannot be easily dismissed, which implies that investors should best see more than just green shoots and bullish analysts’ forecasts of earnings growth. They would do well to demand from brokers scenario-based forecasts for earnings, dividends, and target prices, with specific focus on their estimates of earnings for quarter ending June and Sep 2020.

These are no ordinary times when annual EPS forecast with tweaking around the earning season would suffice. Times like these require frequent and more detailed research communication by the sell side players, to which end the SECP and PSX would do well to encourage listed companies to speak to the market by holding analyst briefings at least every quarter and provide earning guidance.

Comments

Comments are closed.