A common refrain concerning domestic cropping pattern is that it is highly skewed towards low value staple grains and cash crops, with little focus on high value crops such as oilseeds, vegetables and fruits. As a result, low value traditional crops are often produced in surplus, leading to poor farming incomes even though these consume more than 80 percent of water available for irrigation.

A common refrain concerning domestic cropping pattern is that it is highly skewed towards low value staple grains and cash crops, with little focus on high value crops such as oilseeds, vegetables and fruits. As a result, low value traditional crops are often produced in surplus, leading to poor farming incomes even though these consume more than 80 percent of water available for irrigation.

While some major crops contribute to export value chain – crops such as cotton and rice are responsible for over half of country’s foreign exchange earnings – dependence on these high delta crops amounts to virtual export of water. This line of argument goes on to insist that a shift of cropping patterns to high value crops can not only substitute for low value grains and cash crop-based exports, but also address the crisis of water availability.

The above argument, while well-meaning – is flawed on several accounts. While ‘ill-informed’ crop preferences of ‘poorly educated’ growers may offer an easy explanation for Pakistan’s rural poverty, it misses major ground realities.

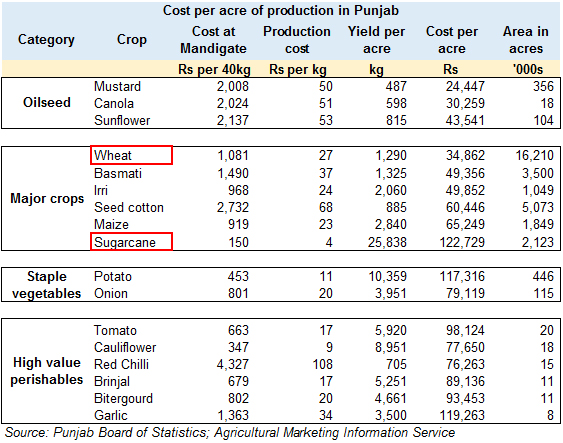

Farmer preference for major crops results from interplay of several – sometimes opposing – variables, chief among them being farm economics. While major crops may not always offer the most profitable choices, for most of Pakistan’s small-scale growers these fall in the low risk, non-perishable, staple, high-demand sweet spot.

Farmer preference for major crops results from interplay of several – sometimes opposing – variables, chief among them being farm economics. While major crops may not always offer the most profitable choices, for most of Pakistan’s small-scale growers these fall in the low risk, non-perishable, staple, high-demand sweet spot.

Take the example of paddy and maize that have enjoyed substantial popularity with growers in recent years. Of course, growing demand for the two crops by food processing value chain – rice for export and poultry by feed mills – has been pivotal in increasing farmer interest. But lower cost of production compared to substitutes has played an equally important role. In addition, low perishability of food grains makes the two crops less risky, protecting against loss of value over long intervals of storage.

On the other hand, crops such as wheat and sugarcane that lack traction in exporting markets due to lack of competitiveness are nevertheless produced in excess of domestic demand. Surprisingly, while wheat requires very low investment, sugarcane is one of the most expensive crops to produce in terms of absolute investment required per acre. Yet excess production of both crops is partly explained by provision of guaranteed returns in the form of minimum support prices, pushing the risk-and-return pendulum in their favour compared to substitutes.

But one factor that probably plays the most overwhelming role in lower traction for high value vegetables among farmers is their higher perishability viz cost per acre. Because most farmers in the country are small-scale, amount of investment required to produce a specific crop becomes the overriding factor in farmer preference.

Because Pakistan does not boast a very liquid formal market for farming credit – whereas informal credit is available at very exorbitant rates – high value crops that require high investment (in absolute value) become a risky proposition, further exacerbated by their higher risk of perishability before reaching ghalla mandis.

The risk of perishability due to vulnerability to pests and extreme weather such as floods and rains also explains the loss of growers’ interest in seed cotton in recent years. For a long time, cotton enjoyed the ultimate cash crop status - along with lower absolute value of investment demanded – its sensitivity to harsh weather has forced farmers to shift to safer choices, often exacerbating production of crops such as sugarcane that are already produced in excess.

One exception that distinctly stands out against the ‘absolute per acre investment rule’ are oilseeds, whose average cost per acre is even lower than wheat. More interestingly, oilseed crops are also not as sensitive to severe weather as vegetables or cotton.

Is low oilseed production a mystery then? Not really, if one looks at the total quantum produced. Because oilseed crops feed into the crushing industry, low average domestic yields have kept the value addition momentum on the down low. Low yields mean that the crushing industry finds it cheaper to import substitutes such as soybean seeds, in turn inhibiting grower interest who can instead earn higher guaranteed returns by making marginally greater investment in crops such as wheat – a vicious cycle.

Average per acre investment required by various crops obviously calls for more comprehensive analysis by policymakers. However, even scratching at available data’s surface indicates that there are no binary solutions to the blighted intersection between Pakistan’s dependence on major crops, water inequity, and rural poverty.

High level of subsistence farming means grower choices may often be a reflection of compulsions resulting from food requirements of farm-dependent family, fodder needs of livestock, guaranteed returns on lower risk staples, absence of storage facilities for perishables, but most importantly, inadequate access to capital that restricts investment in higher value crops.

Comments

Comments are closed.