Nishat Power Limited (NPL) posted its 9MFY18 result, which surprised the market once again on account of no cash dividend being announced by the power generation company. Recall that the company had also foregone dividend payment in the past two quarters.

A potential reason for skipping dividend throughout this year might be the strain on the company’s liquidity situation due to pending receivables by NTDC on account of rising circular debt. According to a research note by Arif Habib Limited, overdue receivables of NPL had reached Rs8.9 billion as of Dec-17, which is an almost 45 percent increase on a year-on-year basis.

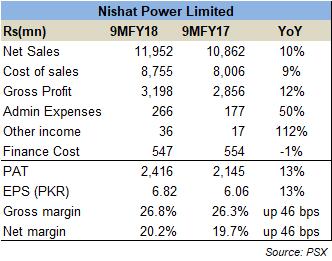

NPL witnessed a 10 percent increase in revenue, which could be attributed to higher dispatches on account of higher generation. Recovering oil prices during the period also have a role to play in the increase in the top-line.

Gross profit clocked in an increase of 12 percent as compared to the same period last year, where both gross and net margins increased by 46bps. The rupee devaluation might have a role to play in keeping margins intact.

There was negligible change in the finance cost as the majority is longer term debt, while reliance on short-term borrowings has seen an increase in mark-up but still constitutes a relatively smaller proportion of overall debt. The cumulative effect on the bottom-line translated into an increase of 13 percent in PAT and EPS on a year-on- year basis.

Going forward, the further devaluation of the rupee as well as clearance of circular debt seems to be two positive factors for Nishat Power Limited. According to sources, another Rs100 billion will be cleared in the coming days while some payments have already been made to IPPs.

Comments

Comments are closed.