Systems Limited (PSX: SYS) was founded in 1977 as a private limited company and was converted into a public listed company in 2005. SYS was listed on PSX in 2015.

The principal activity of the company is the development and trading of software and business process outsourcing services. In short, SYS assists its clients in their digital transformation journey. Besides having a strong footprint in the local market, the company has a firm presence in the US, UK, EU and Middle East.

Pattern of Shareholding

As of December 31, 2024, SYS has a total of 292.986 million shares outstanding which are held by 8253 shareholders. The company’s directors are its largest shareholders with a stake of 32.08 percent in the company. This is followed by foreign companies holding 18.89 percent shares of SYS. Ex-employees account for 14.01 percent of the outstanding shares of the company.

General Public has a shareholding of 10.48 percent while Mutual funds own 7.88 percent shares. Other companies also account for 7.88 percent shares of SYS while insurance companies hold 4.98 percent shares. Around 2.25 percent of the company’s shares are held by executives and the remaining 1.55 percent by banks, DFIs and NBFIs.

Financial Performance (2019-24)

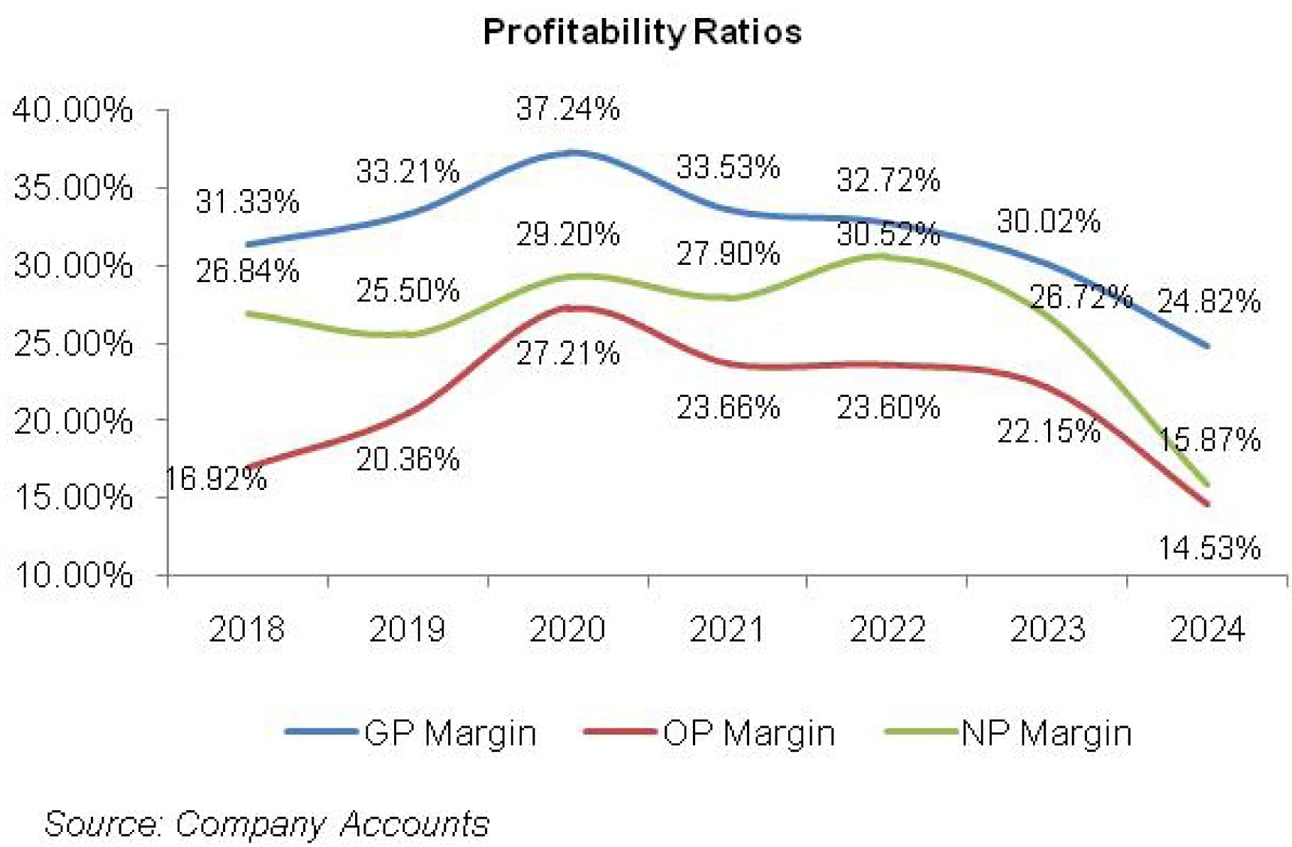

The topline and bottomline of SYS have grown staggeringly over the period under consideration with the exception of 2024 where its bottomline posted a slide. The company’s margins portray a fluctuating pattern over the period under consideration. In 2019, gross and operating margins of SYS posted considerable growth while net margin ticked down. This was followed by an incredible rebound in margins in 2020 and then a slump in 2021.

In 2022, gross and operating margins fell while net margin registered phenomenal growth. In the following years, SYS’s margins recorded a drastic decline and hit their lowest level in 2024. The detailed performance review of the period under consideration is given below.

In 2019, SYS’s topline grew by 42.21percent year-on-year to clock in at Rs.5348.57 million. This was on the back of a selection of a better client portfolio which comprised of large companies. This ensured sustained and recurring business to SYS.

While the cost of sales also moved up mainly on account of increased salaries and wages, purchase of software, travelling and conveyance and technical consultancy, gross profit posted a tremendous 50.73 percent year-on-year growth with GP margin clocking in at 33.21 percent in 2019 versus GP margin of 31.33 percent recorded in 2018.

Distribution expense multiplied by 114 percent year-on-year in 2019, however, the fact that it stood at less than 2 percent of the sales in all the years under consideration, makes this hefty growth figure rather insignificant. Administra-tive expense grew by 18.84 percent year-on-year as the company expanded its workforce from 2289 employees in 2018 to 3174 employees in 2019 which inflated the payroll expense. Other expense inched by 17.45 percent year-on-year mainly on the back of a massive rise in allowance of ECL ontrade debts.

The company also booked provisions against doubtful refundable while contract assets and bad debts written off also significantly grew during 2019. Operating profit posted a year-on-year growth of 71.20 percent in 2019 with OP margin climbing up from 16.92 percent in 2018 to 20.36 percent in 2019.

Other income couldn’t provide any support to the bottomline in 2019 as it plunged by 21.72 percent on the back of lesser exchange gain. Finance cost grew by 107.94 percent in 2019; however, with the debt-to-equity ratio of 28.8 percent in 2019, finance cost didn’t produce much of a negative impact on the bottomline.

SYS’s net profit grew by 35.13 percent year-on-year to clock in at Rs.1364.13 million in 2019 while NP margin slightly lowered to 25.5 percent in 2019 from 26.8 percent in 2018. EPS grew from Rs.8.16 in 2018 to Rs.10.95 in 2019.

Due to the outspread of COVID-19 in 2020, the businesses across the world were facing issues related to mobility. SYS made the most of these turbulent times by offering innovative offerings and solutions to its clients.

As a consequence, its topline grew by 40.48 percent year-on-year to clock in at Rs. 7513.77 million. This was mainly on the back of revenue generated from software implementation services which forms the major chunk of its revenue mix.

Outsourcing services which forms the next big chunk of SYS’s revenue mix also boasted a staggering growth while software trading posted a marginal year-on-year growth of 4.6 percent in 2020. It is to be noted that the company’s revenue is mainly driven by export sales with North American and European markets outshining the other geographical markets.

Hence, local currency depreciationalso had a major role to play in SYS’s topline growth. Gross profit considerably grew by 57.51 percent year-on-year in 2020 with GP margin climbing up to its optimum level of 37.24 percent. Operating expense grew in line with inflation and also because of induction of new employees which took the head count to 3361 employees in 2020.

Other expense slid by 3 percent year-on-year as the company didn’t write off any advances, contract assets and bad debts in 2020 and also didn’t book any provision against doubtful refundable in 2020. Operating profit posted a handsome year-on-year growth of 87.72 percent in 2020 with OP margin reaching its highest level of 27.21 percent.

Other income posted 20.43 percent decline in 2020 on the back of lower exchange gain and lesser gains on the disposal of property and equipment. Finance cost surged by 27.45 percent year-on-year in 2020. While discount rate dropped in 2020, the rise in finance cost was on account of increased borrowings during the year which took its debt-to-equity ratio to 35.6 percent in 2020. SYS’s bottomline posted a robust year-on-year growth of 60.83 percent in 2020 to clock in at Rs.2193.92 million with NP margin of 29.20 percent. EPS also rose to Rs.17.31 in 2020.

In 2021, the magnitude of topline growth further increased to 58.42 percent year-on-year which took SYS’s revenue to Rs. 11,903.58 million. This was driven by demand generated in all the geographies and business segments. 67.79 percent year-on-year mount in cost of sales in 2021 was due to higher salaries and allowances. Software purchases, depreciation, technical consultancy also played a significant role in driving up the cost.

While gross profit grew by 42.64 percent year-on-year in 2021, GP margin weakened to 33.53 percent. Selling and administrative expenses posted huge growth of 59 percent and 96.33 percent respectively in 2021. The main drivers of higher operating expenseswere elevated salaries expense, fee & subscriptions, donations and depreciation. Employee count also escalated to 5068 employees in 2021.

Other expense shrank by 87.44 percent year-on-year in 2021 on account of reversals booked against ECLon trade debts during the year. While operating profit grew by 37.75 percent in 2021, substantial growth in operating expenses pushed OP margin down to 23.66 percent. Other income came to the rescue with an unparalleled 127.53 percent year-on-year growth in 2021 mainly on account of striking exchange gain as company’s export sales grew considerably.

Despite downtick in discount rate, finance cost expanded by 68.87 percent year-on-year in 2021 on the back of elevated borrowings. Debt-to-equity ratio further increased to 45.5 percent in 2021. The bottomline enlarged by 51.36 percent year-on-year in 2021 to clock in at Rs.3320.69 million with NP margin of 27.90 percent which although was lesser than that of 2020, however, is bigger than the OP margin due to significant support provided by other income. EPS ticked down to Rs.11.98 in 2021 due to increase in the outstanding share volume of the company during the year.

Among all the years under consideration, 2022 outperformed with year-on-year topline growth of 73.43 percent. SYS’s net sales clocked in at Rs.20,644.76 million. This came on the back of IT services and increased demand across all the geographies and verticals.

Gross profit improved by 69.25 percent in 2022, yet GP margin lowered to 32.72 percent because of the impact of inflation as well as increase in company’s operations which required purchase of software and induction of additional resources during the year. Operating expense also increased by 49 percent in 2022. The main drivers were increased salaries expense, technical consultancy, purchase of software, repair and maintenance as well as high advertising budget.

The employee headcount clocked in at 5143 in 2022. SYS incurred a loss on derivative financial instruments which drove up other expense by 427.96 percent in 2022. The company registered 72.98 percent higher operating profit in 2022, however, OP margin slightly inched down to clock in at 32.72 percent.

Pak Rupee depreciation provided growth impetus to other income which magnified by 218.70 percent year-on-year in 2022. High borrowing cost coupled with increased borrowing resulted in an increase of 166.38 percent in SYS’s finance cost in 2022.Due to increase in SYS’s equity due to higher paid-up share capital, capital reserve and revenue reserve, debt-to-equity ratio plummeted to 14 percent in 2022. Bottomline rose by 89.71 percent year-on-year to climb at Rs.6299.84 million in 2022 with NP margin of 30.52 percent and EPS of Rs.22.29.

SYS continued to impress in 2023 with 55.19 percent year-on-year growth in topline. This resulted in net revenue of Rs.32,038 million in 2023. This was driven by IT services and continuous improvement in demand across the geographies and verticals.

The company continued to receive business from its existing customers and also enhanced its revenues by cross selling and ups-selling to new customers and customers acquired through acquisition. Export contributed 83 percent in the total revenue of the company; hence depreciation of Pak Rupee also played its due role in buttressing the topline. Middle East made the major export destination of SYS followed by North America. Record high inflation resulted in rise in salaries and wages as well as other components of cost. Gross profit although grew by 44 percent year-on-year in 2023, however, GP margin shrank to 30.36 percent.

Distribution and administrative expenses multiplied by 44.96 percent and 37.15 percent respectively. The main growth drivers were increased payroll expense and elevated advertising budget. The company has been expanding its workforce to manage higher demand. As of December 2023, SYS’s workforce stood at 6589 employees, up 28 percent year-on-year. During the year, the company recorded impairment loss on investment in associate and trade receivables to the tune of Rs.68.95 million and Rs.33.47 million respectively.

Other expense dropped by a massive 90.41 percent in 2023 on account of high-base effect as the company incurred massive loss on derivative financial instruments in the previous year. All these factors translated into 45.66 percent higher operating profit in 2023, however, OP margin slid to 22.15 percent. Other income mounted by 33.80 percent in 2023 on account of Pak Rupee depreciation which resulted in exchange gain.

Elevated borrowings and discount rate culminated into 195.8 percent higher finance cost incurred by SYS in 2023. Net profit registered year-on-year rise of 35.86 percent in 2023 to clock in at Rs.8559.16 million with EPS of Rs.29.22 and NP margin of 26.72 percent.

In 2024, SYS’s topline grew by 20.25 percent to clock in at Rs.38,526.98 million. This mainly came on the back of a robust growth recorded in export sales particularly revenue generated from IT services. The company has continuously been expanding its footprint across North America, UAE, Qatar, Europe, KSA and the APAC region. In 2024, the company’s gross profit slid by 1.70 percent mainly on the back of higher salaries, allowances and amenities incurred during the year coupled with the purchase of hardware and software.

Appreciation in the value of local currency squeezed the company’s revenue in Rupee terms which didn’t allow it absorb the soaring cost. This resulted in the lowest ever GP margin of 24.82 percent recorded in 2024.

Selling & distribution expense surged by 90.80 percent in 2024 on the back of elevated salaries of sales force, travelling & conveyance charges, vehicle running & maintenance charges as well as advertising & sales promotion expense incurred during the year. 20.42 percent escalation in administrative expense recorded by SYS in 2024 was the consequence of higher payroll expense. This was due to workforce expansion to 6701 employees to meet the demand of the growing clientele worldwide.

During the year, the company recorded a massive impairment loss of Rs.605.20 million on its financial assets. This resulted in 21.11 percent drop in operating profit in 2024 with OP margin falling down to 14.53 percent. Other income also slumped by 60.74 percent in 2024 as the company incurred exchange loss during the year. Finance cost tumbled by 64.59 percent in 2024 due to rate cuts during the latter part of the year and also because of repayment of a significant portion of liabilities during the year.

The company maintained a debt-to-equity ratio of 7 percent in 2023 and 2024. Net profit dwindled by 28.55 percent to clock in at Rs.6115.297 million in 2024. This translated into EPS of Rs.20.80 and NP margin of 15.87 percent in 2024.

Recent Performance (1QCY25)

During the first quarter of the ongoing calendar year, SYS’s topline posted year-on-year growth of 19 percent to clock in at Rs.10,898.70 million. Technology and retail proved to be the most profitable segments for the company; however, BFS and Telco registered the highest growth in terms of revenue. Cost of sales mounted by 19.28 percent in 1QCY25 mainly on the back of wage inflation.

Gross profit posted year-on-year growth of 18.16 percent in 1QCY25 with GP margin almost staying intact at 25 percent. Administrative expense and distribution expense escalated by 27.32 percent and 46.93 percent respectively during the period mainly on account of elevated payroll expense, advertising & promotion expense as well as travelling expense incurred in 1QCY25. SYS was able to record 13.35 percent higher operating profit in 1QCY25; however, OP margin slightly inched down from 16.92 percent in 1QCY24 to 16.12 percent in 1QCY25.

The company recorded other income of Rs.401.62 million in 1QCY25 versus other expense of Rs.114.99 million recorded during the same period last year. This was the result of exchange gain as well as interest income recognized from loan to subsidiaries. Finance cost shrank by 59 percent in 1QCY25 due to lower discount rate. Net profit picked up by 62.45 percent to clock in at Rs.2006.536 million in 1QCY25. This translated into EPS of Rs.6.80 in 1QCY25 versus EPS of Rs.4.21 recorded in 1QCY24. NP margin strengthened from 13.49 percent in 1QCY24 to 18.41 percent in 1QCY25.

Future Outlook

As SYS continues to expand in new geographical markets, its export sales will continue to rise which will not only produce a positive impact on the topline but will also keep the other income buoyant. To boost its local sales, SYS is turning its focus from public sector and SMEs to private sector large-scale enterprises particularly in telecom and financial sector.

The local segment of the company is expected to achieve breakeven by 2QCY25.Other sectors where SYS plan to expand include technology, retail and consumer goods segments. SYS is also expanding into consultancy and solution selling services. The company is also leveraging its strategic alliances and is eyeing new partnerships in order to drive new leads, generate and acquire clientele and expand its service offerings.

Comments

Comments are closed for this article.