Highnoon Laboratories Limited (PSX: HINOON) was established in 1984 under the Companies Act, 2017. The company manufactures, imports, sells and markets pharmaceutical and allied consumer products.

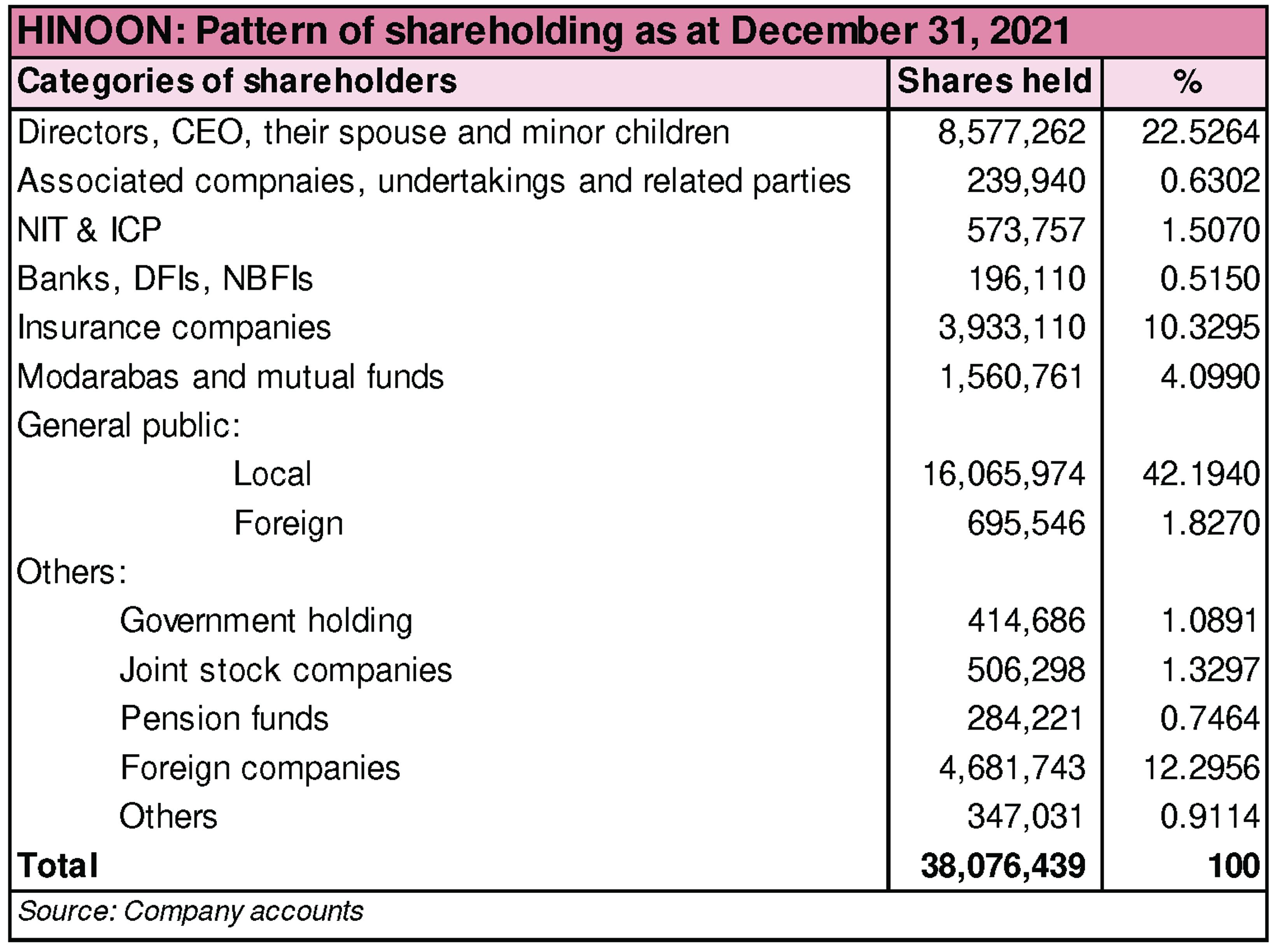

Shareholding pattern

As at December 31, 2021, over 22 percent shares are owned by the directors, CEO, their spouses and minor children. Within this category, Mr. Tausif Ahmad Khan, the chairman of the company, and Mrs. Zainub Abbas own majority of the shares. The local general public owns over 42 percent shares followed by 12 percent held in foreign companies. Another 10 percent is held in insurance companies, while the remaining close to 13 percent shares are with the rest of the shareholder categories.

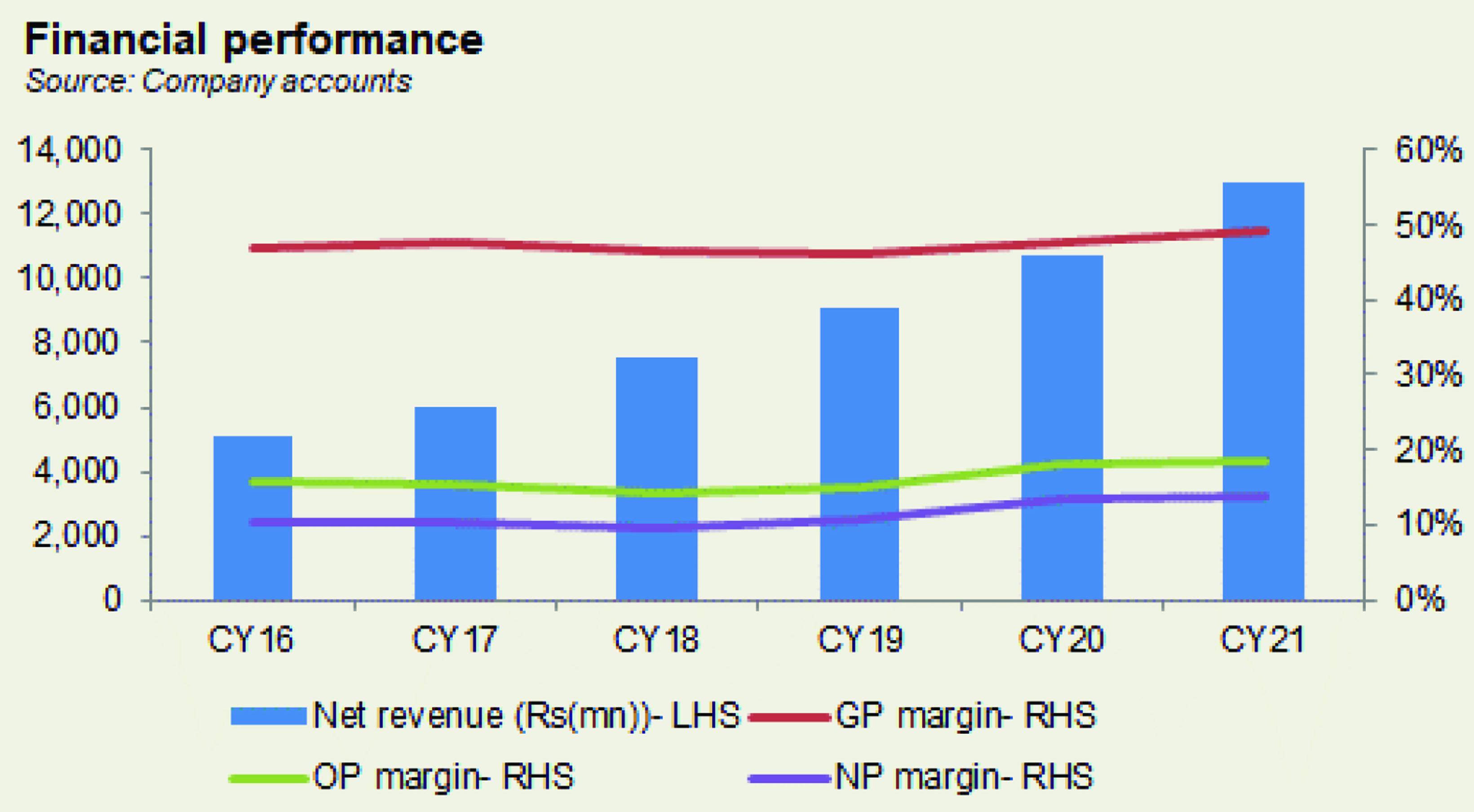

Historical operational performance

The company has mostly seen a double-digit growing topline, with the exception of CY12, when it contracted by over 16 percent, while profit margins in the last six years particularly, have been stable.

Revenue growth in CY18 was at its highest of 25.7 percent, with topline reaching Rs 7.5 billion in value terms. There was a slight decline in export sales due to intermittent border closure in Afghanistan and change of distribution set up. Local sales, on the other hand, increased by almost 30 percent. Segment-wise, alimentary tract and metabolism segment grew by 20 percent, respiratory business grew by 27 percent, followed by cardiovascular segment that posted a growth of 21 percent. With cost of production increasing only marginally, gross margin remained close to 47 percent. However, net margin reduced to 9.7 percent, compared to 10.5 percent in CY17, due to an increase in distribution expense that was attributed to expenditure on product launches and expansion of sales personnel.

Growth momentum continued in CY19 as revenue witnessed an incline of close to 21 percent causing topline to cross Rs 9 billion. This was again a result of increase in local sales that posted a growth of 24 percent, while export sales remained more or less the same year on year. Overall, volume growth for the company stood at 10 percent, compared to 2.4 percent of the industry. All the segments of the company witnessed an incline. The cardiovascular division particularly grew by 39 percent. Cost of production again grew marginally to reach 54 percent, reducing gross margin to 46 percent. However, net margin grew to 10.7 percent as operating expenses decreased, combined with an increase in other income as a share in revenue. The latter was due to return on deposit.

Revenue continued to expand in CY20 as it posted a growth of over 18 percent reaching Rs 10.7 billion in value terms. Local sales were the major contributor to the total revenue as it made 94 percent of revenue. Although export sales also inclined, by almost 41 percent of revenue, it made a small portion of the total revenue pie. Segment-wise, cardio metabolic segment earned Rs 3.2 billion followed by Combivair, a respiratory product that was the first brand of Highnoon Laboratories to cross Rs 1 billion. This was also reflected in the higher gross margin that was recorded at nearly 48 percent, the highest seen thus far. This also trickled to the bottomline that stood at an all-time high of Rs 1.4 billion with a net margin of over 13 percent.

Topline grew by 21.5 percent in CY21 to reach at an all-time high of Rs 13 billion. Export sales grew by 12.6 percent, while local sales registered an incline of nearly 24 percent. During Covid-19, the pharmaceutical sector generally performed better than other sectors in terms of topline. Additionally, as OPDs in hospitals resumed, the companies saw even better sales. As a result, the higher revenue also translated into higher profitability as gross margin reached another high of over 49 percent. But the increase in net margin was marginal at 13.9 percent, from last year’s 13.3 percent. This was due to distribution expenses reverting to consume over 26 percent of revenue, unlike last year when it had reduced to below 25 percent.

Quarterly results

Revenue in the first quarter of CY22 was higher by 20.5 percent year on year. This was attributed to a substantial improvement in volumes, productivity and supply chain practices. But there was a marginal improvement in cost of production that was down to nearly 50 percent, compared to 51 percent in the same period last year. This can be attributed to the currency devaluation and inflation. Thus, gross margin was slightly better at 50 percent. Supported by a higher other income, this also reflected in the net margin that was also marginally better at 14.2 percent versus 13 percent in 1QCY21. While the topline continues to grow as health awareness increases, in addition to resumption of general business activities as lockdowns eased, some of the challenges for the economy as a whole that also affect the company are currency devaluation that increases the cost of raw materials the sector is largely dependent on, inflation and political uncertainty.

Comments

Comments are closed for this article.